What it means for housing

A new era for the Federal Reserve begins on Friday Kevin Warsch takes over leadership of the central bank amid historic political tensions and controversies surrounding the country’s monetary policy.

Warsh, a former Fed governor who served at the central bank during the Great Recession, takes over Jerome Powellwhose second term as chairman is ending. Warsh will serve a four-year term as chairman and a 14-year term on the Fed’s Board of Governors.

Although chairman Donald Trump Self-appointed chairman in 2017, the president has spent the past year directing his ire at Powell for keeping interest rates higher than Trump would like.

In response to a criminal investigation launched by Trump’s Justice Department, Powell is taking the unusual step of remaining on the Fed’s Board of Governors indefinitely after completing his term as chairman. That alone will make Warsh’s tenure remarkable, as he votes on interest rate policy alongside a former chairman.

Meanwhile, Warsh could be caught between a president pushing for lower interest rates and a voting panel on the Federal Open Market Committee that appears increasingly skeptical of rate cuts.

At last month’s FOMC meeting, three “hawks” who favor higher interest rates disagreed with the final vote. They said they were in favor of keeping rates stable but did not support the statement issued with the decision, which they said should not include language suggesting the next move on rates will be a cut.

Cleveland Fed Chairman Bet HammakMinneapolis Fed Chairman Neel Kashkariand the president of the Dallas Fed Lori Logan believe instead that a rate hike could just as likely be the Fed’s next move. Their dissent may have been intended to send a strong message to Warsh as he prepared to take power.

Although he is now chairman of the Federal Reserve, Warsh will have just one vote on the 12-member FOMC and will need to get the majority on his side to make changes to interest rate policy.

“Can Warsh even practically convince this FOMC to make cuts right now? Very unlikely. They have made their positions known and put predictions on paper,” says Realtor.com® senior economist Jake Krimmel. “But strategically, should he try? Probably not. The incoming data currently favors an increase before a decrease.”

The Fed uses higher interest rates to curb inflation and lower interest rates to stimulate the labor market, in line with the central bank’s dual mandate: price stability and maximum employment.

In the past week alone, major federal reports have shown that the labor market remains surprisingly robust, while inflation is rising back to a three-year high — a combination that seems to portend higher interest rates from the Fed.

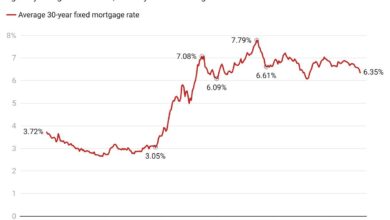

Mortgage rates have already responded, rising rapidly in March as an oil price shock from the war in Iran raised concerns about inflation.

Warsh must show independence

Above all, Warsh will now face the crucial task of convincing markets that he is an independent Fed chairman who acts based on economic data and sound judgment, rather than political pressure or the whims of the president.

By law and tradition, the Fed is structured to be independent of political whims and influences. History shows that keeping interest rates artificially low for political purposes can lead to runaway inflation and capital flight. That would wreak havoc on the economy and ultimately increase borrowing costs.

Instead, the Fed should set interest rates based on its mandate. Yet policymakers often have honest disagreements about what interest rate would be ideal for the economy.

During his confirmation hearing in the Senate last month, Warsh insisted that Trump had not given him a specific mandate on interest rate policy.

“I take my responsibility as the independent leader of the Federal Reserve very seriously,” Warsh said. “The president has never asked me in any of our discussions to pre-determine, commit, lock in an interest rate decision, and I would never agree to that.”

Still, economist Krimmel says that on the issue of Warsh’s independence, “the consensus among Fed observers is skeptical for now.

“What confuses many is that Warsh was an inflation hawk when he was governor from 2006 to 2011, then turned into a dove when he ran for chairman,” Krimmel said.

The inconsistency itself is not the problem, says Krimmel, because shifting information can and should lead to changing insights. But Warsh’s record raises concerns that his views on monetary policy could be influenced by who occupies the White House.

“A chairman who is not data-dependent cannot be independent,” says Krimmel. “Over time, Warsh will have ample opportunity to prove his independence, but that will only be truly tested when he is faced with an economic crisis or forced to make a politically unpopular call.”

Warsh’s unusual plan to lower mortgage rates

Essentially, Warsh seems to believe that the Fed can create room to cut rates without fueling inflation if it simultaneously reduces the size of the central bank’s balance sheet.

It is an untested theory, and works on the principle that two opposing forces will cancel each other out: a looser monetary policy on interest rates, and a tighter policy on the balance sheet.

Warsh has always been critical of the Fed’s large balance sheet, which ballooned during the Great Recession as the central bank sucked securities from the open market, a process known as quantitative easing.

After trimming some of these assets, the Fed began buying again in earnest during the COVID-19 pandemic, including purchasing trillions of mortgage-backed securities, which scientists believed had pushed mortgage rates to ultra-low levels below 3%.

More recently, Fannie Mae and Freddie Mac, at Trump’s direction, have carried out a similar scheme, increasing their mortgage holdings in an effort to squeeze term out of the market and keep interest rates low.

But Warsh appears to be in favor of unwinding that trade at the Fed and selling the central bank’s hoard of mortgage bonds, worth about $2 trillion.

“The Fed’s bloated balance sheet, designed to support the largest companies in a bygone crisis era, could be significantly downsized,” Warsh wrote in a recent publication. Wall Street Journal op-ed. “That generosity can be used in the form of lower interest rates to support households and small and medium-sized businesses.”

If the Fed were to sell its mortgage bonds, it would put upward pressure on mortgage rates, but Warsh argues that this effect can be countered by lowering the Fed’s short-term interest rate. It’s a plan that’s never been attempted before.

Krimmel says there is “also an important catch-22” in Warsh’s plan to trade a smaller balance sheet for lower interest rates.

“If markets think the Fed is making a policy mistake, such as cutting inflation while inflation is running high, that mistake will be priced into the long end of the curve,” he says. “Practically speaking, long-term rates would rise and mortgage rates would rise even if the Fed lowers its policy rate.”