Should you continue renting or become a homeowner?

The dream has long been associated with homeownership, leading many people to view renting as a temporary step rather than a long-term housing plan. This mentality often pressures people to rush into one of the largest financial commitments of their lives before they are truly prepared.

However, many financial experts are now encouraging people to evaluate renting and homeownership based on personal financial readiness and goals. Continuing to rent can provide greater financial flexibility, depending on one’s income, savings goals and lifestyle needs buy a house can provide stability, potential for equity building, and the opportunity to establish long-term roots. If you are thinking about switching to a new home in Evanston, ILor across the country for one house in Fresno, CAthis Redfin article discusses why renting can be strategic, when homeownership may be the right next step, and how to evaluate which option best supports your financial and lifestyle goals.

Evaluate your financial readiness

A thorough financial evaluation forms the basis for determining your housing path. Rather than assuming one option is always better, it’s helpful to compare the two based on your income, savings, debt, and long-term goals.

Renting can provide time to strengthen credit, grow savings, and prepare for the full cost of homeownership beyond just a mortgage. On the other hand, buying may make sense if you have a stable income, a solid emergency fund, manageable debt, and enough savings for initial and ongoing costs.

Clint Stucky, Marketing Director at Industrial Federal Credit Unionnotes that renting “can provide time to strengthen credit, grow savings, and prepare for the full cost of homeownership beyond just a mortgage.” If buying a home gives you little financial flexibility, that may be a sign to continue renting until you are better prepared.

>>Read: What does “Financial Done” Really mean?

Down payment and debt burden

Your down payment, monthly housing costs, and debt-to-income ratio all play a role in determining whether purchasing is realistic. While some lenders may approve loans with a higher amount debt-to-income ratiosThat doesn’t always mean taking on that amount of debt is the best choice.

Justin Boggs, from Optima Capital, LLCrecommends keeping home debt between 25 and 35% of your income to maintain your long-term investment goals. A useful way to assess your overall readiness is to look at consistency, including steady income, manageable debt, and the ability to comfortably handle upfront costs and ongoing maintenance.

For renters, this same evaluation can help determine whether continuing to rent supports other priorities, such as paying off debt, building an emergency fund, investing, or saving for a future down payment.

>>Discover: How much house can you afford?

When renting can make sense

Renting can be a strategic choice when flexibility, liquidity or short-term mobility are priorities. If you are moving in the coming years or want to avoid unexpected maintenance costs, renting can offer more freedom and predictability.

Renting can be especially useful if you change careers, move, downsizingor unsure about your long-term plans. It can also allow you to live in a desirable neighborhood without taking on the full financial responsibility of the property.

Mackenzie Richards op SKwealth emphasizes that renting can provide flexibility at any age. For clients looking to downsize, selling their home first and moving to a rental property can allow them to purchase a new property without making the sale of their old home a contingency. Renting first can also be helpful after a recent move, giving you time to familiarize yourself with the area before purchasing.

When buying can make sense

Buying can be a good choice if you are financially prepared and plan to live in your home long enough to offset the costs start-up costs when buying a houseand want more control over your living space. Homeownership can provide long-term stability, the opportunity to build equity, and potential appreciation over time.

For many buyers, a fixed-rate mortgage can also offer more predictable principal and interest payments compared to rent, which can increase over time. Ownership can also offer you the opportunity to renovate, personalize your spaceand establish deeper roots in a community.

Buying can make sense if you have a stable income, a strong emergency fund, a manageable debt load, and a clear understanding of the full cost of ownership, including property taxes. homeowners insurancemaintenance, repairs and possible HOA fees.

Misconceptions about building wealth

A common misconception is that renting is always ‘throwing money away’. Another is that buying is always the better financial move. In reality, both options can support wealth building, depending on your circumstances.

AJ Ayers, co-founder of Brooklyn Fisays, “It’s a common belief that homeownership is always the better financial move, but that’s only true if you’re truly prepared for it.” The most difficult obstacle to renting is the stigma attached to it, but “in most major cities, renting can be a smarter financial move, with flexibility as a serious bonus.”

Sean Ingraham, senior vice president at First Residential Serviceclaims it’s time to abandon the old advice that everyone should be a homeowner. He suggests that for many, especially in expensive markets, “renting a house and investing the difference can produce more wealth than taking out a huge mortgage.” Ayers adds that in some situations, home values can average about 3% per year, while a diversified investment portfolio has historically returned closer to 8%.

At the same time, homeownership can be an important wealth-building tool for prepared buyers. Mortgage payments can increase equity, and homeowners can benefit from the appreciation over time. Depending on your situation, ownership can also provide tax benefits and long-term housing cost stability.

Compare the costs of renting and buying

The long-term costs of renting versus buying vary by market, interest rates, home prices, rental prices and how long you plan to live in the home. In some places, renting month-to-month can be cheaper. In other countries, purchasing may become more cost-effective over time.

Owning a home involves more than just the mortgage payment. Buyers must also consider property taxes, insurance, maintenance, repairs, closing costs, HOA fees and possible unexpected expenses. However, ownership can also provide equality, stability and the opportunity for appreciation.

Renting usually comes with fewer surprise costs and less responsibility for maintenance. Tenants pay for flexibility, liquidity and predictable cash flow, although they may face rent increases or restrictions on the extent to which they can personalize their space.

Using a rent vs buy calculator can help you compare the full financial picture, including upfront costs, monthly payments, investment options and how long you expect to stay.

How to choose between renting and homeownership

Ultimately the decision will be between renting or home ownership should be based on financial readiness, lifestyle goals, and stability. For some people, continuing to rent may be a smarter, financially responsible choice if your current lifestyle, long-term plans or savings goals better suit the flexibility and predictable costs of leasing. Shelley Carlson, EVP Marketing and Relationship Management at 1st University Credit Unionstates that “renting doesn’t fall behind. It’s often the smarter choice if you’re still building your financial foundation.” For others, homeownership can provide greater stability, long-term equity building, and the opportunity to create a home that meets their needs over time. By carefully evaluating both options, you can ensure that your choice supports your long-term financial health.

>>Read: Renting versus buying a house

Frequently asked questions

Is renting really a waste of money?

No. Renting is an exchange of money for a predictable place to live, flexibility and freedom from major maintenance costs. The biggest misconception is that renting is throwing money away, when in reality you are paying for flexibility, liquidity and predictable cash flow.

How do you calculate financial readiness?

To assess readiness, conduct a rent-versus-buy analysis, comparing the long-term cost of renting versus the opportunity cost of tying down a 20% down payment on a home.

What is a good housing debt-to-income ratio (DTI)?

Justin Boggs recommends keeping your home debt between 25 and 35% of your income to safeguard your long-term investment goals, even if some lenders offer loans that exceed this threshold.

Should market conditions influence my decision to buy?

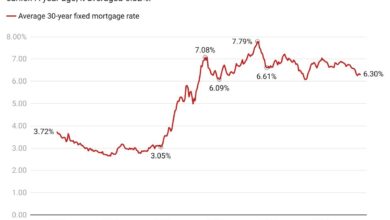

Market conditions should be part of your decision, but should not be the only factor. Mortgage interesthome prices, inventory and local rental trends can all impact affordability. However, the decision to purchase should still be driven primarily by personal factors, such as income stability, savings, debt, family needs and how long you plan to live in the home. It can be difficult to wait for interest rates to fall, as falling interest rates can also put upward pressure on home prices.

>>Read: Is Now a Good Time to Buy a House?