What Is Certified Payroll & How to Comply in 2026

Key takeaways

- Certified payroll compliance depends more on accurate worker classification, wage calculations, and recordkeeping than the form itself.

- Whether federal or state prevailing wage laws apply is determined primarily by how the project is funded, not just where it’s located.

- Failing to comply can lead to serious consequences, including withheld payments, contract termination, debarment, and legal penalties.

Certified payroll is a weekly payroll report required under the Davis-Bacon and Related Acts (DBRA), a federal law that governs wages on federally funded construction projects. Contractors and subcontractors working on projects valued at over $2,000 must submit these reports to the US Department of Labor (DOL) to demonstrate that workers are being paid the required prevailing wage.

The report, submitted using Form WH-347, details employee wages, benefits, hours worked, and job classifications. Each submission also includes a statement of compliance, certifying that the information is accurate and that all workers have been paid in accordance with DBRA requirements.

If you’re new to government-funded projects, certified payroll can feel more complex than standard payroll. In my experience, most compliance issues come down to a few key areas: misclassifying workers, miscalculating fringe benefits, or overlooking state-specific rules. Getting these wrong can lead to delayed payments, contract issues, or even penalties.

It’s also important to note that some states, such as California and New York, have their own prevailing wage and certified payroll requirements, which may differ from federal rules. Always check applicable state laws before processing payroll.

DBA vs. DBRA: What’s the difference?

- Davis-Bacon Act (DBA): Applies to federally funded construction contracts over $2,000. It sets the requirement to pay prevailing wages and submit certified payroll.

- Davis-Bacon and Related Acts (DBRA): Expands DBA requirements to federally assisted projects (such as those funded through grants, loans, or other programs).

In practice, most contractors refer to both together as “Davis-Bacon,” but DBRA is what brings many non-direct federal projects under the same prevailing wage rules.

If you’re managing certified payroll across multiple employees or projects, manual reporting can quickly become time-consuming. Many payroll providers offer certified payroll features to help automate reporting and reduce compliance risk. For example, ADP RUN’s Point North Certified Payroll Reporting supports both union and nonunion contractors and can accommodate state-specific requirements.

How to fill out form WH-347

Filling out Form WH-347 can feel overwhelming at first, especially if you’re new to certified payroll. But this process is simply about accurately documenting employee pay, hours, and classifications in line with the law. Once you understand what each section is asking for, it becomes a repeatable weekly task.

You can make this process more manageable with preparation. Before you begin, make sure you’re maintaining accurate and up-to-date records of each employee’s pay rate, hours worked, deductions, fringe benefits, and job classifications. I’ve seen most reporting errors happen not because the form is complicated, but because the underlying data is incomplete or inconsistent.

Two areas tend to cause the most confusion: fringe benefits and worker classifications. This is especially true when employees perform multiple types of work in a single week. In these cases, you’ll need to report each classification separately with corresponding hours and pay rates, which is easy to miss if you’re not tracking work at a detailed level.

Certified payroll requirements most commonly apply to construction-related industries, including:

- Plumbing

- Electrical

- Painting

- Highway projects

- Public works initiatives

If you decide that doing your certified payroll manually is the best option, we’re here to help. Below, you’ll find screenshots and line-by-line guidance to help you fill out Form WH-347.

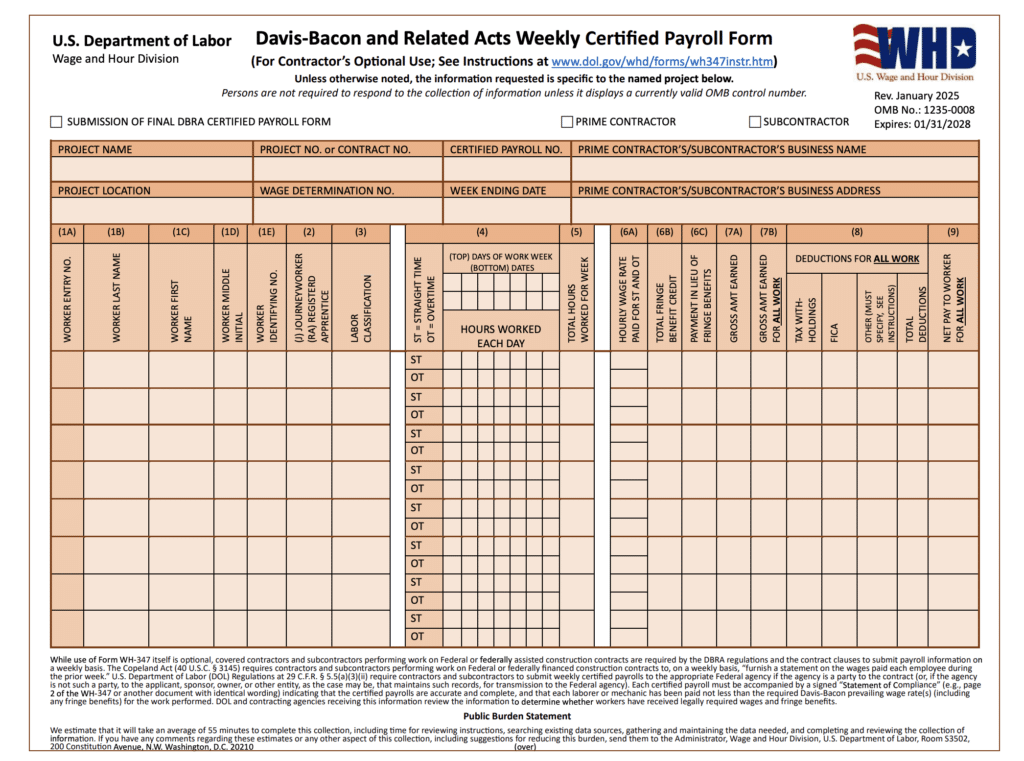

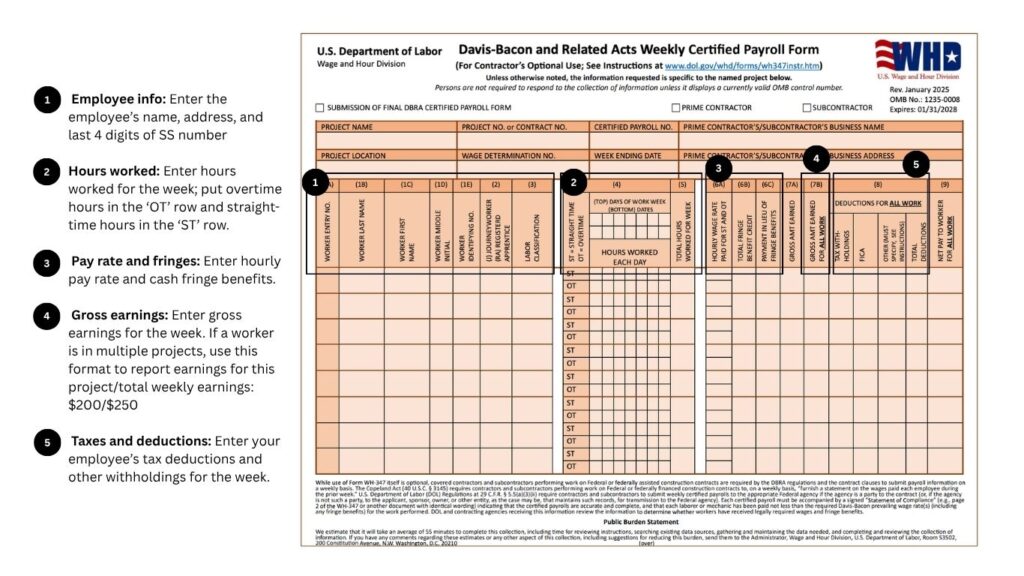

Certified Payroll Report: Page 1

This table provides a quick overview of the basic information you’ll need to add to the top of the form. Then, we’ll get into the employee specifics and work details you’ll enter in the rest of the form.

Enter the following information about your employees and their work details:

Worker entry number and worker information (Columns 1A–1E)

Enter each worker as a separate line item. Provide the worker’s last name, first name, and middle initial. Include a unique identifying number, such as the last four digits of the worker’s Social Security number or an employee ID, to maintain privacy while ensuring accurate tracking.

Worker status and classification (Columns 2–3)

Indicate whether the worker is a journeyworker (J) or a registered apprentice (RA), then list the labor classification that reflects the actual work performed. This classification must align with the wage determination in the contract. If a worker performs multiple types of work, you must record each classification separately with the corresponding hours worked.

Hours worked (Column 4)

Record the hours worked each day of the week using the grid provided. Enter straight time (ST) and overtime (OT) hours in their respective rows. For contracts subject to the Contract Work Hours and Safety Standards Act (CWHSSA), hours worked over 40 in a week must be recorded as overtime.

Total hours worked (Column 5)

Add all straight-time and overtime hours for the week and enter the total.

Hourly wage rate (Column 6A)

Enter the hourly wage rate paid for both straight time and overtime work. Ensure the rate meets or exceeds the applicable Davis-Bacon prevailing wage for the worker’s classification.

To prevent confusion, separate the straight-time hourly rate and cash paid in lieu of fringe benefits like this: “$10.15/.60.” This would reflect a $10.15 base hourly rate plus 60 cents for fringe benefits. This comes in handy when computing overtime.

When an employee works overtime, show the overtime hourly rate paid, plus any cash in lieu of fringe benefits paid in the overtime box; if there was no overtime, you may skip this box. If the work falls under the CWHSSA, you must pay the employee overtime at a rate of 1.5 times the regular rate if the prime contract exceeds $100,000.

Fringe benefit credit (Column 6B)

Enter the hourly credit for fringe benefits provided through bona fide benefit plans (such as health insurance or retirement contributions). These must comply with Davis-Bacon requirements.

Cash paid in lieu of fringe benefits (Column 6C)

If fringe benefits are not provided through a plan, enter the cash equivalent paid directly to the worker.

Gross amount earned (Columns 7A–7B)

Record the worker’s gross earnings for the week. This includes total earnings for the project as well as total earnings across all work performed, if applicable.

If the worker earned part of their money from projects other than the project you’re reporting on this payroll form, enter the following in column 7:

- Amount earned on the federal or federally assisted project

- Gross earnings during the week on all projects

For example, if you entered $200.00/$420.00, it would reflect that a worker earned $200.00 on a federally funded construction project during a week that they earned a total of $420.00 on all work.

Deductions (Column 8)

List all deductions made, including tax withholdings, FICA, and any other authorized deductions. All deductions must comply with applicable regulations.

If one of your workers works on other jobs in addition to this project, show actual deductions from their weekly gross wages and indicate that deductions are based on gross wages.

Net pay (Column 9)

Enter the worker’s net pay after all deductions have been applied.

Certified Payroll Report: Page 2

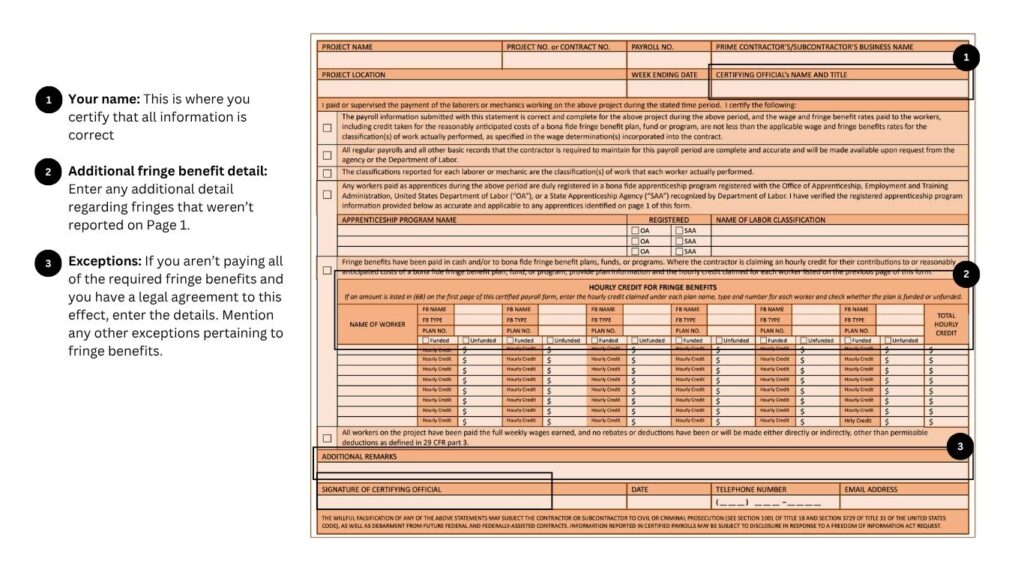

Statement of compliance

This section certifies that the payroll information submitted for the project is complete and accurate. The certifying official must confirm that all workers have been paid at least the applicable Davis-Bacon prevailing wage rates, including any required fringe benefits.

A notarized signature is not required, but signing this statement carries legal responsibility. False certification may result in civil or criminal penalties, including fines, imprisonment, and potential debarment from future federal contracts.

Project and certifying official information (Top section)

Enter the project name, contract or project number, payroll number, and business name. Include the project location, the week ending date, and the name and title of the certifying official.

This information must match the details reported on Page 1 to ensure consistency across the certified payroll submission.

Certification statements (Checkbox section)

The certifying official must review and affirm several required statements, including:

- The payroll information is complete and accurate for the reporting period.

- All workers have been paid no less than the applicable prevailing wage and fringe benefit rates for the classifications of work performed.

- Payroll records are complete and available for inspection upon request.

- Worker classifications reflect the actual work performed.

Each applicable box must be checked to confirm compliance with Davis-Bacon and Related Acts (DBRA) requirements.

Apprenticeship information

If any workers are classified as apprentices, you must confirm they are registered in a bona fide apprenticeship program approved by the U.S. Department of Labor (OA) or a recognized State Apprenticeship Agency (SAA).

Provide the apprenticeship program name and the corresponding labor classification for each apprentice listed on Page 1.

Fringe benefit statement and hourly credit details

Indicate whether fringe benefits are paid through bona fide plans, funds, or programs, or provided as cash payments.

If you claim a fringe benefit credit (as reported in Column 6B on Page 1), you must provide detailed information for each worker, including:

- Benefit plan name

- Type of benefit

- Plan number

- Whether the plan is funded or unfunded

- Hourly credit amount

If fringe benefits are not fully provided through plans, any remaining required amounts must be paid to workers in cash and reflected appropriately in payroll reporting.

Final certification and signature

The certifying official must sign and date the form and provide contact information, including a phone number and email address. By signing, you confirm that:

- All workers have been paid their full weekly wages.

- No unauthorized deductions or rebates have been made.

- All information submitted is truthful and compliant with federal regulations.

How to determine prevailing wage

The purpose of certified payroll is to ensure workers on federally funded projects are paid fairly. When you sign the Statement of Compliance, you’re certifying that every laborer and mechanic has been paid at least the applicable prevailing wage and fringe benefits for their classification, as required under the DBRA.

To determine the correct rates, use the Department of Labor’s Wage Determinations online search tool, which is accessible through SAM.gov. Locate the wage determination tied to your contract, then identify the appropriate classification for each worker.

Each classification includes:

- A base hourly wage

- A fringe benefit rate

You must meet both components. This means either:

- Paying the full fringe benefit amount through bona fide benefit plans, or

- Paying any remaining fringe amount directly to the worker in cash

Accurately matching workers to the correct classification is critical. If a worker performs multiple types of work, you must apply the appropriate wage rate to the hours worked in each classification.

Apprentices and trainees may be paid less than the full prevailing wage rate, but only under strict conditions. Apprentices must be registered in a DOL-approved apprenticeship program, and trainees must participate in an approved training program for a construction occupation. Their pay rates must follow the schedule outlined in those programs. Otherwise, they must be paid the full prevailing wage for their classification.

Calculating fringe benefits

Under the DBRA, contractors are required to provide workers with both a base hourly wage and a fringe benefit amount as defined in the applicable wage determination. Meeting this requirement ensures the total compensation package meets or exceeds the required rate.

Fringe benefits can be provided in two ways:

- Funded plans: These include benefits such as health insurance, retirement plans, or life insurance. Contributions must be made to bona fide third-party plans on behalf of the employee.

- Unfunded plans: These include benefits like paid time off or sick leave that are paid directly by the employer. These must be a legally enforceable commitment and cannot be discretionary.

To calculate fringe benefit contributions, contractors must annualize the rate of contributions for all employee hours worked, not just those worked on Davis-Bacon-covered projects. Fringe benefits must also be paid for all hours worked, including overtime.

For calculating fringe benefits, contractors should refer to the prevailing wage determination issued by the DOL. A contractor’s fringe benefits must meet or exceed the prevailing wage determination issued by the DOL for the particular job classification and location.

Fringe benefits are paid for all hours worked, including overtime. However, the overtime premium applies only to the base hourly wage, not the fringe portion.

To determine the hourly credit, deduct the basic hourly rate paid from the total hourly fringe rate. If the basic hourly rate paid is less than the hourly credit, the contractor must make up the difference by paying the employee the additional amount or by adding benefits.

Federal laws vs state laws on prevailing wage

While the Davis-Bacon Act governs federally funded construction projects, it’s not the only set of rules contractors need to follow. Many states have their own prevailing wage laws, often referred to as “Mini Davis-Bacon” or “Little Davis-Bacon” laws, that apply to state-funded work.

Currently, about 20 states enforce their own prevailing wage requirements, and these can differ from federal rules in important ways. One of the biggest differences is the contract value threshold that triggers compliance.

For example, California applies prevailing wage requirements to projects valued at $1,000 or more, while Missouri sets a much higher threshold at $75,000. This means whether you need to comply can depend heavily on the state and the size of the project.

The key factor is how the project is funded. If the project is federally funded, DBA requirements apply. If it’s funded by a state or local government, you’ll need to follow that state’s prevailing wage law. In cases where both federal and state funding are involved, you may need to comply with both sets of rules, typically following whichever standard is stricter.

If your project is in a state that doesn’t have its own prevailing wage law, then you only need to follow federal DBA requirements for certified payroll.

Penalties for not complying with certified payroll laws

Submitting detailed weekly reports in addition to your regular payroll process can be daunting. However, it’s necessary to avoid the negative consequences that result from not complying with prevailing wage and certified payroll laws.

Here are the penalties for violating Davis-Bacon laws:

- Debarment: Debarment from future contracts for up to three years

- Payments placed on hold: Contract payments may be withheld to pay for unpaid wages and award damages that result from overtime violations

- Termination: Termination of the federal contract

- Prosecution: Falsification of records could lead to civil or criminal prosecution, which could be punishable by fines and imprisonment

If the Wage and Hour Division determines you violated applicable laws, you can challenge the determination before an administrative law judge. You can also appeal decisions made by the administrative law judge to the Administrative Review Board (ARB), and if you’re unhappy with the ARB’s decision, you can appeal to the federal courts.

Bottom line

To comply with the Davis-Bacon Act, it’s crucial to understand your required federal and state prevailing wage and certified payroll requirements. Take your time when calculating total wages and fringe benefits, and ensure to maintain detailed payroll records. If needed, consider outsourcing your payroll to a provider that can handle certified payroll for you.

You can simplify this process by utilizing the services of ADP RUN. This service allows you to take full advantage of a comprehensive suite of tools that automate and streamline your entire payroll process, including certified payroll, so you can stay compliant and keep your government contracts. Get three months free today.

Source link