Delayed jobs data provides surprises as housing market gains momentum

After weeks of delayed data, we finally have an update on the job market – and it’s not exactly what most people expected.

Data delayed by the federal government shutdown is starting to trickle in. We found that September’s workforce was more robust than many expected, with 119,000 new jobs in the month – largely in the health, food and social assistance sectors. Still, some sectors saw employment declines, including transportation and warehousing and the federal government.

Although government data on unemployment insurance claims Although unemployment has remained remarkably stable, private data shows that layoffs will increase by 2025. Against this backdrop of hiring and layoffs, the unemployment rate rose to 4.4% in September.

Nevertheless, profits continued to rise, up 3.8% from a year ago. This means that employees again saw a real increase in purchasing power last year.

Newly released information underlined what Chairman Jerome Powell hinted at the Fed meeting in October: There may not be support for a Fed rate cut in December. According to the minutes of that meeting, “many participants” expected the policy rate to remain unchanged for the rest of the year. Mixed signals from the labor market are likely to reinforce this wait-and-see perspective.

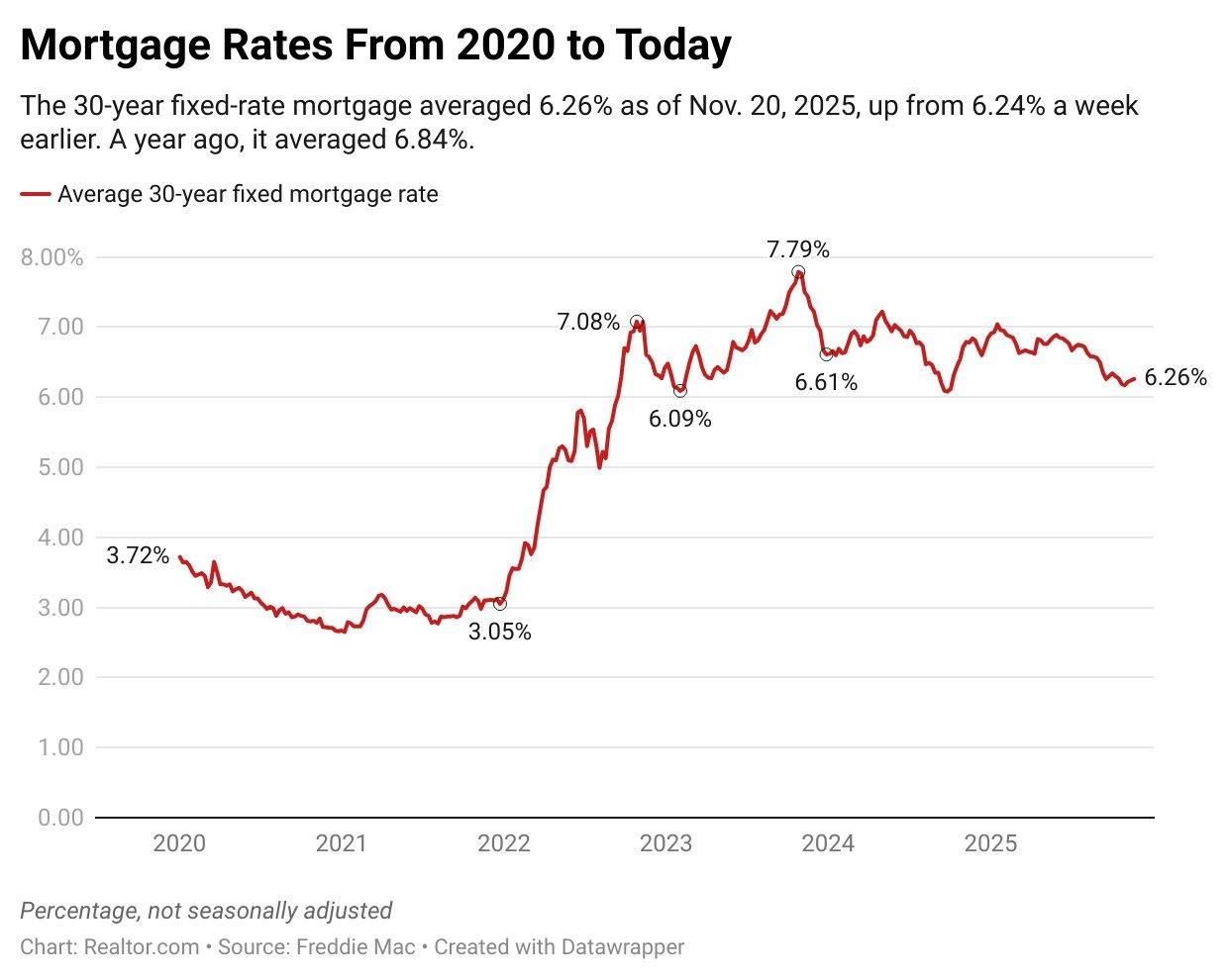

Mortgage rates reflected this trend, rising only a modest 2 basis points this week, landing right in the middle of the narrow range of about 6 and a quarter percent they have occupied since mid-September.

This stability in mortgage rates was welcome news for buyers and sellers and ultimately resulted in an increase in existing home sales in October, which rose to the highest level in eight months despite the impact of the government shutdown.

In addition to the fourth consecutive month of annual sales increases and continued home price growth, the data shows that the share of first-time buyers in the housing market has risen to 32%, up from 27% a year ago. Simply put, buyers responded to improved home and mortgage interest rates this fall.

Looking at the weekly trends in housing data, inventory continued to grow and the growth rate continued to slow. On balance, active listings were still 13% below 2017-2019 standards Realtor.com® October’s Housing Trends report, so there’s still more room for recovery. New listing activity rose for a second week and asking price trends remain weak as homes sit longer than they did this time last year.

Finally, the Realtor.com Rental report showed that asking rents continued to decline, extending the streak to 27 months in October. Even after the declines, rents are still almost 17% higher than in 2019.

This is a much smaller jump than the 26% increase in overall consumer prices and almost 50% increase in the price per square meter of homes for sale, but affordability is still a big driver when looking for tenants.

The report shows that cheaper markets like Detroit, Philadelphia and Sacramento have seen the most pronounced growth in the share of renters who came from elsewhere over the past six years. This suggests that renters are willing to move to find lower costs.