6 Best ACH Payment Processing for Small Businesses

My top picks for ACH payment processors for small businesses include Stripe for its overall versatility, Square as a small business-friendly all-in-one solution, and Helcim for its strong value-for-money. Together, they lead my list of six cost-effective, feature-rich ACH payment platforms that stand out in today’s market.

As a popular alternative to credit cards for its significantly lower fees, Automated Clearing House (ACH) payments continue to grow. Total ACH Network volume from Q1 2025 to Q1 2026 rose by 4.8% to 8.9 billion payments, valued at $24.1 trillion, up by 9.3%.

The best ACH payment processing for small businesses are:

Best ACH payment processing compared

How I chose the best ACH payment processors for small businesses

To evaluate the best ACH payment processors, I fact-checked each provider to ensure that pricing and features were accurate. I then scored each one on 24 data points, prioritizing ACH fees and features, value for money, and ease of use. See my full methodology below.

I have over five years of experience testing and reviewing payment processing technology, merchant services, and POS systems. My goal is to help small businesses streamline financial workflows and boost efficiency.

Payments Staff Writer at Fit Small Business

Automated Clearing House (ACH) payments are electronic bank-to-bank transfers that pass through the ACH network, regulated by the National Automated Clearing House Association (Nacha).

This nonprofit body oversees the ACH Network in the United States, setting the rules and standards that make electronic payments secure, reliable, and widely adopted for payroll, bill pay, and business transactions.

Small businesses favor ACH payments as an alternative to credit card transactions for the following reasons:

- Lower fees than credit cards (often <1% with caps vs 2.9% + 30 cents for cards)

- Predictable costs for large invoices and recurring payments

- Trusted and widely adopted for payroll, invoicing, and B2B transactions

- Reduced reliance on card networks, which can mean fewer chargebacks and more direct settlement

So, if you’re in the market for an ACH payment processing solution, here are the key points you need to know:

- You have three ACH payment platform types to choose from: One is the independent ACH platform, ideal if you prefer simple transactions. The other is an independent provider with integration capability that can connect to accounting, invoicing, or ERP software. Or, you can choose a platform that’s built into a credit card payment processor.

- You can opt for a platform that can also make ACH payouts: An ACH debit functionality is what you need to accept payments for things like subscriptions or memberships. But if you also require the ability to settle your accounts payable via bank transfers, then your choice should include an ACH credit feature.

- ACH payments are possible both for in-person and online transactions: Depending on the platform, you can accept payments through a mobile app at the point of sale, via ecommerce checkout with digital wallets, or by invoice and recurring billing.

- An echeck is a type of ACH payment: The echeck payment data includes the customer’s bank account and routing number, which then goes through the ACH network.

- Same-day processing is possible with ACH payments: This option allows funds to clear within a single business day (or a few hours) instead of the usual two to five days. However, it requires that both your customer and your bank support this feature. There are also sending limits and higher fees involved.

Other ACH payment key features include:

- Account validation: Verifies bank details like routing and account numbers before processing payments

- Cross-border capabilities: International payment processing options with some providers for cross-border transfers

- Support for surcharging: Businesses can provide customers with the option to pay via ACH in lieu of credit cards with surcharge fees

- Typical funding speed: Generally two to five business days, with faster options available from certain processors

Same Day ACH allows payments to clear within a single business day instead of the usual two to five days. Transactions submitted before Nacha’s cutoff windows are processed and settled the same day, provided both the sending and receiving banks support Same Day ACH.

According to Nacha, Same Day ACH volume grew from 326 million payments in Q1 2025 to 403 million in Q1 2026 — a 23.6% year-over-year increase. For small businesses, this means improved cash flow and reduced waiting times. The trade-off is that Same Day ACH often carries higher costs and may be subject to daily dollar limits.

Learn more:

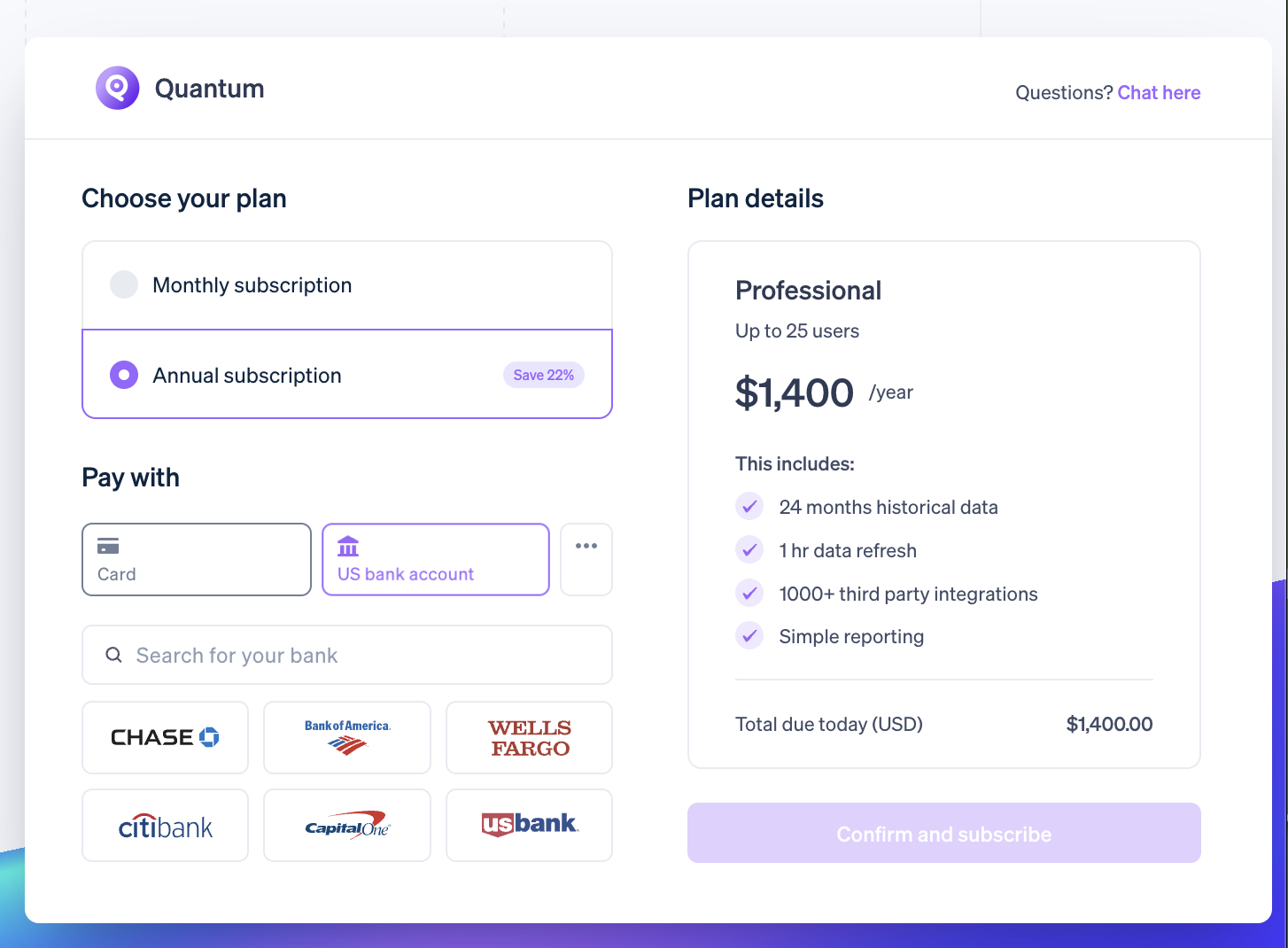

Stripe: Best overall ACH payment processor

![]()

![]()

Pros

- Highly customizable platform

- ACH reconciliation

- Accepts ACH Credit

Cons

- Requires some technical expertise and resources

- Has add-on rates for invoicing and recurring billing

- Limited to US merchants and customers

Overview

Who should use it:

Stripe is the best choice for businesses that need a highly customizable ACH solution with advanced reconciliation tools and flexible workflows.

Why I like Stripe:

Stripe is a leading international payments platform widely recognized for its developer-friendly APIs, extensive integrations, and support for both ACH debit and ACH credit transfers. It’s most well-known for offering powerful reconciliation tools that automatically match incoming ACH payments to invoices, saving time and reducing manual errors.

What I like most about Stripe is how well it lives up to its “Best Overall” claim: its customization and reconciliation features are unmatched. Whether you’re sending recurring invoices or managing large-scale ACH reconciliation, Stripe provides highly flexible workflows and automatic invoice matching thanks to ACH credit support and auto-reconciliation tools that tie payments to invoices seamlessly.

That being said, Stripe isn’t without its trade-offs. Implementation often requires technical resources, invoicing and recurring billing come with additional costs, and ACH services are currently limited to US merchants and customers. For businesses looking for a simpler setup with built-in tools at no extra charge, Helcim is a practical alternative.

- Monthly Subscription: $0

- ACH Payment Processing

- Add-on monthly fee: $0

- ACH Debit Processing fee: 0.8%, maximum of $5 per transaction

- ACH Credit Processing fee: $1.00 per payment

- ACH reject/failure fee: $4

- ACH dispute/refund fee: $15

- Two-day settlement: 1.2%

- Instant bank account validation: $1.50 per transaction

- Other Fees

- In-person: 2.7% + 5 cents

- Online: 2.9% + 30 cents

- Keyed-in: 3.4% + 30 cents (card payment details are manually entered in the Stripe dashboard)

- Invoicing: From 0.4%–0.5% per transaction (on top of transaction fees)

- Recurring billing: 0.5%–0.8% per transaction (on top of transaction fees)

- Accepts ACH payments via invoicing, payment links, and checkout pages

- Allows saving of the customer’s ACH bank details for recurring payments

- Has bank account verification to reduce fraud and stay compliant with NACHA validation rules

- ACH Direct Debit may be added as a payment option to any of Stripe’s integrations

- Offers options to instantly verify the customer’s bank details (requires coding skills)

- Creates US virtual bank accounts for each of your customers for easy automatic reconciliation of ACH credit payments

- Automatic reconciliation also allows customers not to provide any bank details and to pay in multiple transactions

- Allows ACH refunds directly from the Stripe Dashboard

Its wide range of payment solutions has earned Stripe a place in several of our guides:

Create highly customized ACH checkouts with Stripe. [Image Source: Stripe]

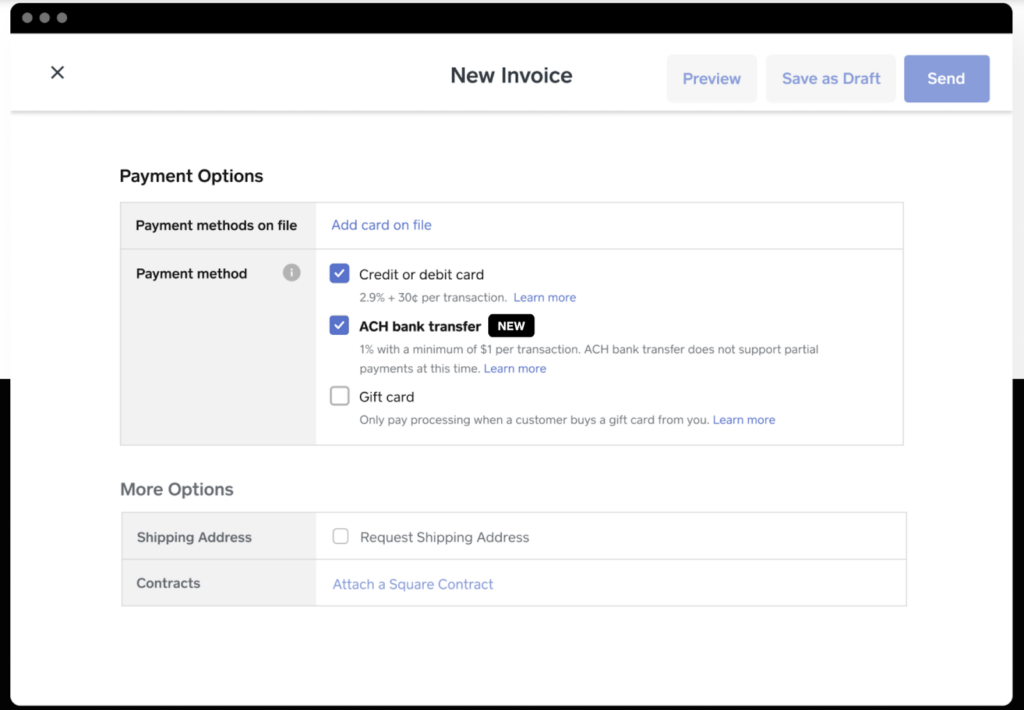

Square: Best for small and new businesses

![]()

![]()

Pros

- Affordable pricing

- No ACH reject/chargeback fee

- Easy to use

Cons

- Accepts ACH payments only through invoices

- Limited cross-border capabilities

- No cap on processing fee

Overview

Who should use it:

Square is the best choice for small or newly established businesses that want an easy-to-use ACH option built within an all-in-one POS system.

Why I like Square:

Square is an all-in-one POS and payments platform designed for accessibility and ease of use. It’s most well-known for providing small businesses with a feature-rich free plan that includes POS, invoicing, and payment acceptance in one package.

Its ACH functionality works well for invoice-based transactions, which are common for service providers, contractors, and freelancers. But what I like most about Square is that it does not charge a failed transaction fee. Many providers charge $5 to $15 per failed ACH payment, but Square absorbs that cost, which is a big advantage for newer or smaller businesses that can’t afford unpredictable penalties.

While Square is very small business-friendly, its ACH feature set has limits. ACH is available only for invoice payments, cross-border capabilities are restricted, and there’s no cap on ACH processing fees, which means costs can rise on larger transactions. For businesses with higher-value invoices or international clients, Helcim or Stripe may be a better fit.

- Monthly Subscription: $0

- ACH Payment Processing

- Add-on monthly fee: $0

- ACH processing fee: 1%, minimum of $1 per transaction

- ACH reject/failure fee: $0

- ACH chargeback fee: $0

- Other Fees

- Card-present: 2.6% + 15 cents

- Ecommerce and invoice: 2.9% + 30 cents

- Card-not-present: 3.5% + 15 cents

- Invoicing: 3.3% + 30 cents

- No monthly fee and flat ACH processing rate

- Allows ACH payments through invoicing only

- Does not charge fees for failed/rejected ACH transactions

- Send and track invoices and automatic payment reminders to customers

- Approval and settlement times take around 2-3 days

Square is also a top pick in our other guides:

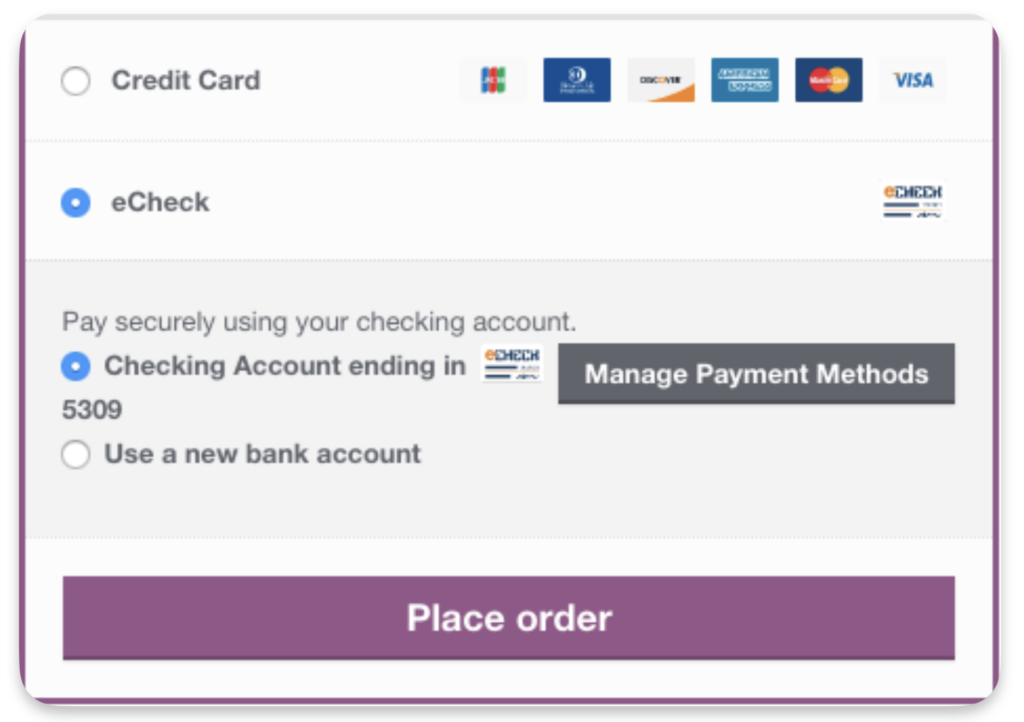

Add an ACH payment option on your Square invoice. [Image Source: Square]

Helcim: Best for cheapest processing fees

![]()

![]()

Pros

- ACH embedded in wide range of transaction types

- Comes with a traditional merchant account

- Qualifies merchants for surcharging features when approved for ACH processing

Cons

- Lacks fast funding option

- Limited cross-border payment support

Overview

Who should use it:

Helcim is the best choice for small and mid-sized businesses that want the lowest ACH processing costs without monthly fees.

Why I like Helcim:

Helcim is a Canada-based payment processor popular in the industry for its cost-optimization features, particularly for its built-in automated processing discounts. It comes with a traditional merchant account, making it a more stable option for businesses with a steady transaction volume.

As an ACH payment processor, Helcim supports ACH transactions across a wide range of transaction types, including invoicing, recurring billing, ecommerce, and virtual terminals. But what sets it apart is its ability to provide merchants with surcharging features by using ACH payments as an alternative to cards.

Note, however, that Helcim does not support fast settlement options for ACH payments. Transfers take about three to four business days to withdraw and four to six business days after batch processing to reach your bank. If this is a dealbreaker, consider Stripe instead.

- Monthly Subscription: $0

- ACH Payment Processing

- Add-on monthly fee: $0

- ACH processing fee =<$25,000: 0.5% + 25 cents, $6 cap per transaction

- ACH processing fee >$25,000: +0.05%

- ACH reject/failure fee: $5

- Other Fees

- Card-present: Interchange + (0.3% + 8 cents to 0.10% + 5 cents)

- Keyed and Online: Interchange + (0.50% + 25 cents to 0.20% + 10 cents)

- 24/7 customer support

- Accepts ACH payments through invoicing, recurring payments, subscriptions, QR codes, email and SMS payment requests, and virtual terminal

- Includes a traditional merchant account

- Offers free credit card payment processing service

- Tracks ACH payments together with all forms of transactions, including POS, online, mobile, and virtual terminal payments within the same platform

- Strong security and fraud protection tools

You will also find Helcim among our different guides:

Helcim offers surcharging tools for merchants accepting ACH payments. [Image Source: Helcim]

GoCardless: Best standalone ACH platform

Pros

- Transparent, affordable pricing

- Accepts international ACH payments

- Easy to set up and use

Cons

- Only processes ACH payments

- Processing rates increase to access premium feature

- Faster funding only for higher plans

Overview

Who should use it:

GoCardless is the best choice for businesses that want a dedicated ACH solution with international payment processing capabilities.

Why I like GoCardless:

GoCardless is a standalone ACH platform built specifically for bank-to-bank payments. It’s most well-known for its transparent, affordable pricing and easy setup, as well as its ability to process both domestic and international ACH payments.

Beyond its standalone platform, GoCardless also offers pre-built integrations with popular tools for accounting, membership management, and subscription billing, including Xero, QuickBooks, Zuora, Recurly, TeamUp, and Chargebee. That said, I like how GoCardless offers a wide range of native solutions on its own.

Note that GoCardless only processes ACH payments, so businesses needing card or other payment methods will need a second provider. Access to faster funding is reserved for higher-tier plans, and processing rates increase if you want premium features.

- Monthly Subscription: $0

- ACH Payment Processing:

- Standard: 0.5% + 5 cents, maximum of $5 per transaction

- Advanced: 0.75% + 5 cents, maximum of $6.25 per transaction

- Pro: 0.9% + 5 cents, maximum of $7 per transaction

- International transactions: Same transaction rate but fixed fee varies based on country where customer is located

- ACH reject/failure fee: $5

- ACH chargeback fee: $5

- Accepts international payments

- Collects ACH payments via online form, email, or payment link

- Integrates with various accounting and billing systems for automatic reconciliation

- Sends automatic customer notifications for every transaction

- Offers discounts for high-volume businesses (contact the GoCardless sales team)

- Has paid plans that come with added customizations, such as branded payment pages and your business name on bank statements

- Provides migration assistance for those moving from another provider

Powered by Wise to support international payments from 30+ countries [Image Source: GoCardless]

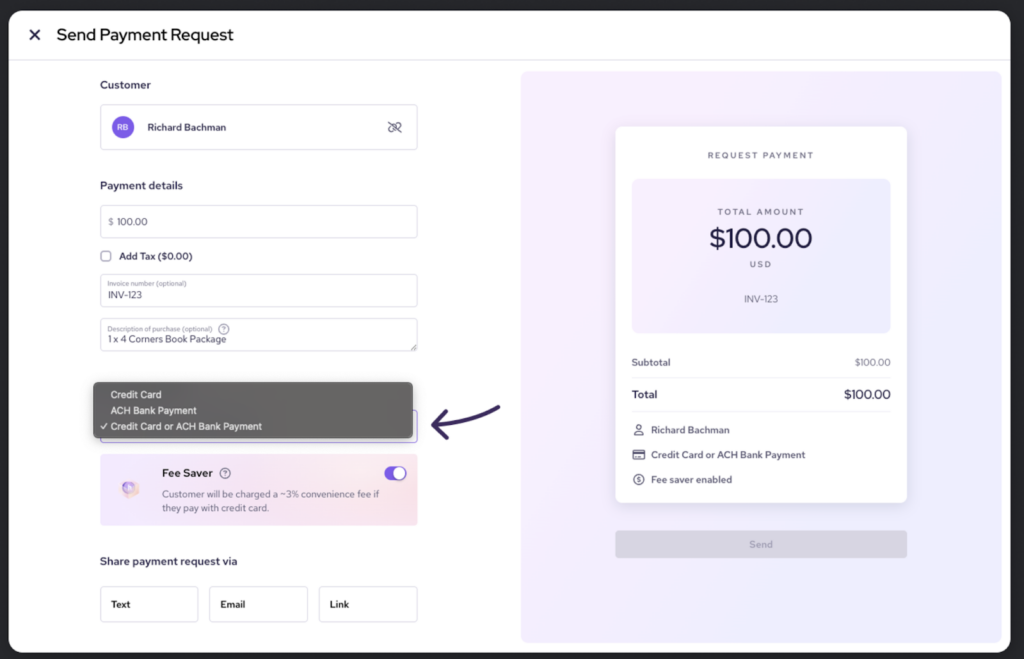

PayPal: Best for add-on ecommerce checkout

Pros

- Flexible checkout that works alongside other payment processors

- Widely used digital payment platform

- Supports both ACH debit, echecks, and Venmo

Cons

- Flat-rate fees can be expensive for small business with growing sales volume

- Popular target of fraud

- Poor customer support quality

Overview

Who should use it:

PayPal is the best choice for businesses that want to add a flexible, widely recognized checkout option alongside their existing payment processor.

Why I like PayPal:

PayPal is one of the most widely used digital payment platforms in the world, best known for its recognizable checkout button and its ability to integrate seamlessly with ecommerce platforms. For many small businesses, enabling PayPal alongside an existing processor helps reduce cart abandonment by offering customers a trusted, familiar payment choice.

What I like most about PayPal is that it’s the only provider on this list that supports multiple ACH payment types. In addition to ACH debit, PayPal also processes echecks and integrates Venmo, giving small businesses more flexibility to accept bank-based payments from different customer preferences. This makes PayPal uniquely versatile for merchants who want more than just standard ACH debit functionality.

While PayPal is versatile, it does come with drawbacks. Its flat-rate fees can become expensive as sales volume grows, and customer support is often criticized for being slow or inconsistent. As one of the most popular digital payment brands, PayPal is also a frequent target for fraud attempts. These limitations make it better as a complementary checkout option rather than a business’s sole ACH or payment processor.

- Monthly fees:

- Basic: $0

- Optional services:

- Recurring billing: $10 per month

- Recurring billing tools: $30 per month

- Invoicing service: $14.99 per month

- ACH Payment Processing:

- ACH processing fee: 0.80% (capped at $5.00 per transaction)

- ACH return/dispute fee: $5 per transaction

- ACH through invoicing: 1% (capped at $10.00 per transaction)

- Other fees:

- Credit and Debit Card Payments: 2.99% + 49 cents

- PayPal Checkout: 3.49% + 49 cents

- Pay with Venmo: 3.49% + 9 cents

- PayPal Pay Later options: 4.99% + 49 cents

- Local payment methods in other countries: 2.89% + 29 cents

- Payment gateway transactions: 10 cents via standard or payment links/button

- Invoicing: From 2.99% + 49 cents to 4.99% + 49 cents

- Micropayments (under $10): 4.99% + 9 cents

- Crossborder transactions: +1.5%

- E-checks: 3.49% + fixed fee* (capped at $300 per transaction)

- Standard online checkout services:

- Semi-hosted checkout (Payments Advanced): $5 per month

- Fully customized checkout (Payments Pro): $30 per month

- Payment gateway (Payflow Pro): $25 per month

- Manual entry:

- Card Payments: 2.89% + 29 to 49 cents

- Virtual terminal: 3.39% + 29 cents + $30 per month

- ACH: 0.80% (capped at $5.00 per transaction)

- Incidental fees:

- Dispute fee (buyer’s PayPal account or a PayPal checkout transaction): $15 (for US merchants)

- Chargeback fee (guest checkout transactions): $20 (for US merchants)

- Custom rates:

- Advanced Credit and Debit Card Payments (Interchange Plus, Plus): Interchange Pass-through Costs + 0.49% + 39 cents

- Wide variety of payment methods

- Supports ACH Direct Debit

- Supports echecks (processed via ACH)

- Bank-to-bank transfer via Venmo payments

- Option for primary or add-on checkout option

- Highly compatible ecommerce checkout integration

- Mobile-friendly checkout experience

- Recognized and trusted global brand

- One-click checkout

Related reading:

Choose from PayPal’s ACH debit, echeck, or Venmo options [Image Source: PayPal]

Authorize.net: Best flexible ACH payment gateway

Pros

- Highly compatible with multiple payment processors

- Supports all types of payment types, including ACH

- 24/7 customer support

Cons

- Charges a monthly fee regardless if you already have a payment processor

- Very low echeck transaction fee but no cap

- Lacks fast funding option

Overview

Who should use it:

Authorize.net is the best choice for businesses that want a flexible ACH gateway that can connect with multiple processors and support a wide range of payment types.

Why I like Authorize.net:

Authorize.net is a long-standing payment gateway owned by Visa, best known for its broad compatibility with existing processors and merchant accounts. It supports all major payment types, including ACH through its echeck feature, and works across different processors, making it a reliable option for businesses with mixed payment needs.

What I like most about Authorize.net is how it delivers compatibility with most payment processors and merchant service providers. Its ACH functionality can be used alongside credit cards and other payment methods, and it integrates with recurring billing tools for subscription-based businesses. This flexibility makes migration to a different payment processor seamless for those who find they’ve outgrown their current provider.

The main trade-offs with Authorize.net are cost-related. For one, it charges a monthly fee, which adds fixed overhead that some small businesses may find unnecessary. In addition, its echeck transaction fees don’t come with a cap, so costs can add up quickly on larger transactions. If cost is your main concern when choosing an ACH payment processor, consider Stripe or Helcim instead.

- Monthly gateway+echeck: $25

- ACH payment processing:

- Echeck per transaction fee: 0.75%

- Other fees:

- Credit card per transaction fee: 10¢ + daily batch fee 10¢

- Chargeback fee: $25 (all-in-one plan)

- Support for echecks (ACH payments) via the echeck.Net solution

- Accept ACH payments via virtual terminal, enabling manual entry of account info

- Enable recurring ACH billing through automated echeck authorization

- Streamlined integration with multiple existing merchant accounts and processors

- Fraud protection tools included (e.g., Advanced Fraud Detection)

- API access and developer SDKs for custom integrations (including mobile)

- Support for multiple payment types: cards, ACH/echeck, virtual terminal, and recurring invoices/subscriptions

Also read: Best Payment Gateways in 2025: Cut Fees & Start Saving

ACH payments processing calculator: Compare fees for the best providers

Use this calculator to compare ACH processing fees for our top providers and see which fits your small business best.

How to choose the best ACH payment processing for small business in 5 steps

Choosing the best ACH payment service is slightly different from choosing a credit card payment processor. Consider the following points before signing up with an ACH payment provider.

Consider how you want to accept payments

Most businesses prefer credit cards as the main payment method, with ACH payments as an alternative. Some business types, such as B2Bs, may prefer direct-to-bank transactions. If this is the case, you can work with providers like GoCardless that specialize in ACH payment processing. Otherwise, look for payment processors with the best overall rates for all your payment methods.

Payment processors provide merchants with a merchant account, but you need to know which type of merchant account best matches your business. Read our guide to merchant accounts to learn more.

Evaluate the transaction fees

ACH payment processing fees range anywhere from 0.5% to 1.5% and, naturally, the lowest rate gives you more savings. However, you also need to look into the fee caps. Without it, any ACH payment you accept becomes more expensive after a while.

Compare transaction limits

Higher transaction limits mean you pay less transaction fees, so find out the per-transaction, daily, and monthly ACH processing limits. Most banks working with payment processors would process as much as $5,000 per day, but it may not be the actual limit your payment processor will allow for your account.

Compare incidental fees

Like credit card transactions, ACH payments can impose reject and dispute fees. This can be caused by various reasons, including some that are out of your control, such as a customer’s insufficient funds. Ideally, fees of this kind should range between $2–$5 per instance. Chargeback fees are sometimes higher, but no more than $25.

Consider the processing time

ACH payments take longer to process than credit card transactions. The average wait time is one to three days for processing and approval, plus one to two days for funds to be transferred to your bank. Some payment processors offer Same Day ACH processing, while others offer instant fund transfer to make up for the wait time. In both cases, be sure to find out if you are paying extra for the faster processing service.

Methodology: How I evaluated the best ach payment processing companies

I looked for merchant services that offer affordable ACH payment processing. Then, I narrowed my evaluation to six of the most affordable and reputable platforms and considered their different ACH processing fees and features.

I also compared monthly fees, add-on ACH fees, failed/reject fees, and settlement speed. Next, I looked for specific use cases like high-risk businesses, as well as real-life user reviews and ease of use.

Here are our specific evaluation criteria:

20% of Overall Score

I gave the most points to payment processors that offer low or zero monthly fees, do not require contracts or monthly fees, do not impose account cancellation charges, and have low reject/return fees.

30% of Overall Score

I assessed whether each solution offers invoicing, payment links, recurring payments, virtual terminal, and ACH reconciliation. I also considered if the processor provides Level 2 or Level 3 processing.

30% of Overall Score

Here, I considered a range of functions essential for ACH payment processing, such as customer support, approval/settlement times, customer management features, security and compliance tools, and deposit speed.

20% of Overall Score

This combined my overall evaluation of price and ease of use with scores from real-world users on trusted third-party review sites.

*Percentages of overall score

Frequently asked questions (FAQs)

ACH stands for Automated Clearing House, an electronic network that allows for the transfer of funds between bank accounts in the United States. The ACH network is operated by the independent organization Nacha with defined ACH network rules and regulations.

The key difference between ACH debit and ACH credit transactions for small businesses is who initiates the transaction.

An ACH debit transaction is initiated by the merchant, who authorizes the transfer of funds from the customer’s bank account to the merchant’s bank account (upon getting the customer’s authorization). On the other hand, an ACH credit transaction is initiated by the customer, who authorizes the transfer of funds from their bank account to the merchant’s bank account.

To accept ACH payments from customers, you will need to sign up and set up an ACH payment processing service. Once you have chosen an ACH payment processor, you will need to enable ACH payments for your account and set it up based on your provider’s instructions.

Yes, there is typically a processing fee for ACH payments. The fee may vary depending on the payment processor or bank used to process the ACH transaction. Some processors charge a flat fee per transaction, while others charge a percentage of the transaction amount. Generally, ACH processing fees are much lower than typical card processing fees, so it allows businesses to save on transaction costs.

Bottom line

ACH payments processing provides businesses an efficient, secure, and cost-effective way to get paid. When choosing an ACH payment service, businesses should consider factors such as processing fees, transaction limits, ease of use, approval and payout speeds, and customer support.

Among the best ACH payment processing for small businesses, Stripe stands out as the best overall option due to its zero monthly fees, comprehensive ACH features, ACH reconciliation, competitive pricing, robust security and fraud protection tools, and excellent customer support.

Source link