Understanding Business Credit Reports (2026): How to Read Them

A business credit report is a snapshot of a company’s financial health. It shows details about the company’s debt and how it handled debt payments in the past. It’s broken into various sections, each showing different information for company liens, outstanding loans, derogatory payment information, and recent credit applications.

Lenders and investors often review this report when deciding whether to approve financing and what rates or terms to offer. Potential vendors and business partners may also use it to gauge a company’s financial stability before working together. That’s why it’s worth understanding what appears on your business credit report and how to interpret the information it contains.

Business credit reports can be obtained from different credit bureaus, although Dun & Bradstreet (D&B) is most commonly used by lenders. D&B also provides other products and services that allow business owners to monitor their business credit profile.

How to read a business credit report

The exact layout of a business credit report can vary depending on the credit bureau or provider, but most reports include many of the same core sections. Below is a general overview based on a sample report from Experian, one of the major business credit reporting agencies that provides access to business credit reports and scores.

- Business profile is a general overview of your company, such as its contact information, years in business, and business type.

- Business credit score and risk rating is a numerical score reflecting a particular type of risk associated with a company.

- Credit summary is a high-level overview of a company’s credit accounts, such as total balances, payment amounts, liens, delinquent accounts, and more.

- Account payment history typically provides details of each individual account, including creditor names, balances, payment terms, account types, and payment history.

- Credit inquiries contain details of recent applications for credit, such as the creditor name and the date they pulled a business credit report.

- Significant derogatory information details late payments, judgments, tax liens, bankruptcies, and foreclosures.

- UCC filings may contain details on if the business has pledged any items as collateral.

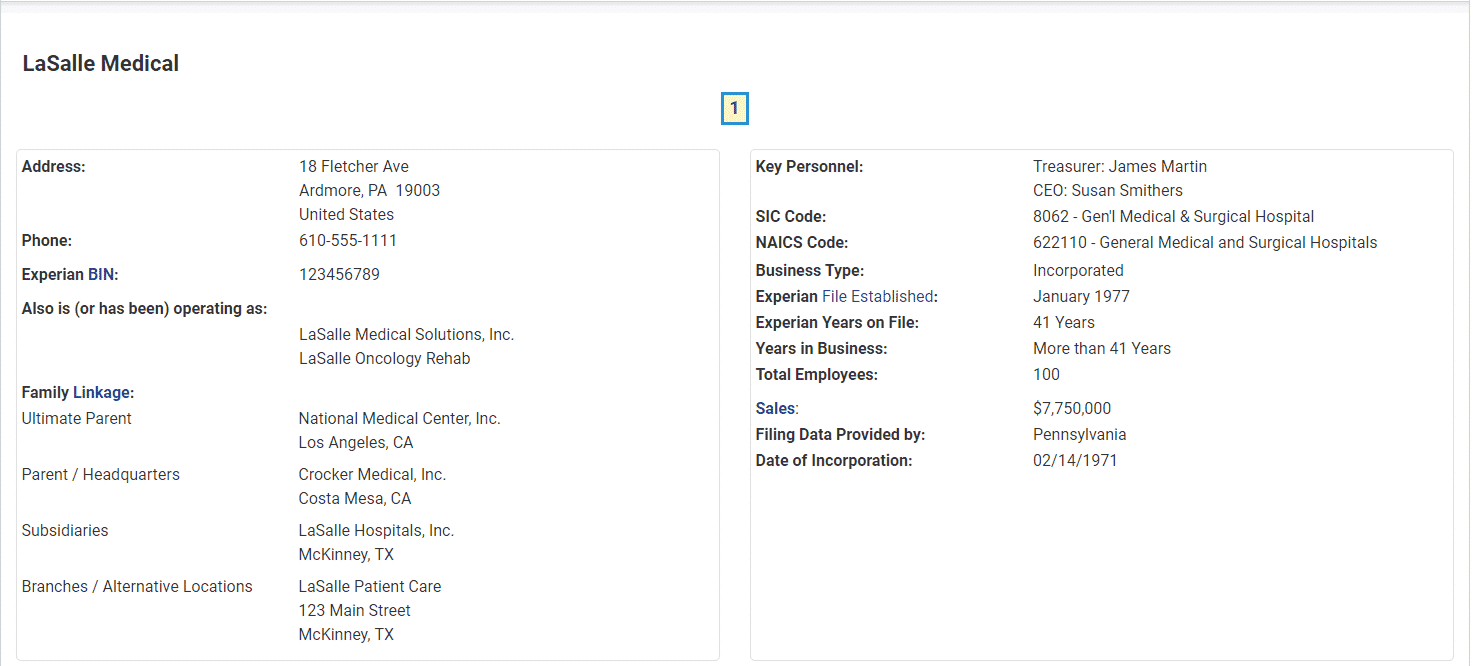

Business profile

One of the first sections you’ll likely see on your business credit report is a general profile of your company.

A business profile section taken from a sample credit report by Experian for a fictitious business. (Source: Experian)

This section provides basic identifying details about your business, including its name, address, and contact information. While much of this information is straightforward, you may also see a few technical terms used by credit bureaus and government classification systems, such as:

- BIN (Business Identification Number) is a unique number that the credit bureau uses to identify your company. It operates similarly to an Employer Identification Number (EIN) or Social Security Number (SSN).

- SIC (Standard Industrial Classification) Code corresponds to a US government system for identifying the industry in which your business operates. You can visit the US SEC’s SIC Code List to locate the SIC code for your industry.

- NAICS (North American Industry Classification System) Code is used to classify which industry your company operates in. Although similar to SIC codes, NAICS codes can provide a greater level of detail. You can visit the NAICS’s code by industry page to find your code.

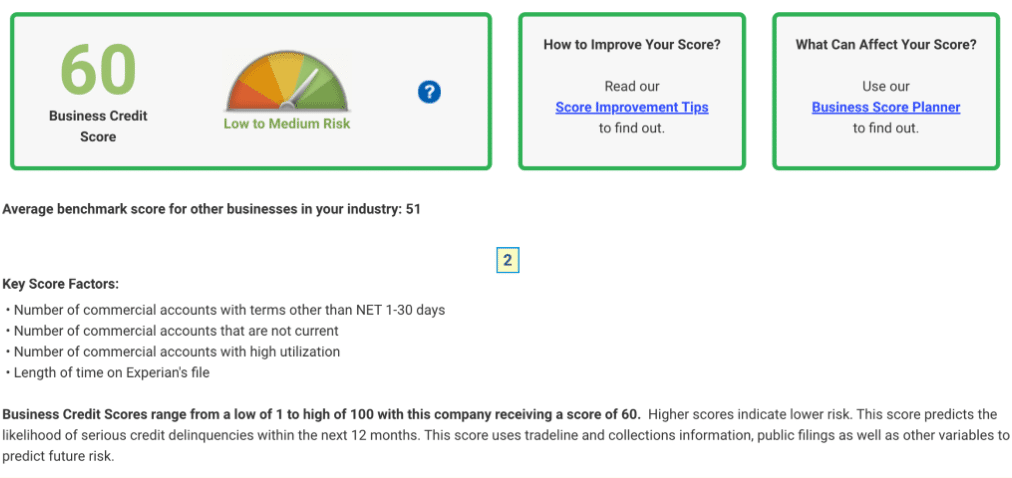

Business credit score & risk rating

Depending on where you get your business credit report, you may also get a credit score. The image below is one example of a score you might get if you obtained a credit report through Experian.

An example of how Experian might display credit scores on its credit reports. (Source: Experian)

Credit scores are intended to reflect a business’s overall level of risk, but different scoring models evaluate different risk factors. For example, some models estimate the likelihood of delinquency or default within a specific timeframe, while others are designed to assess the probability of bankruptcy.

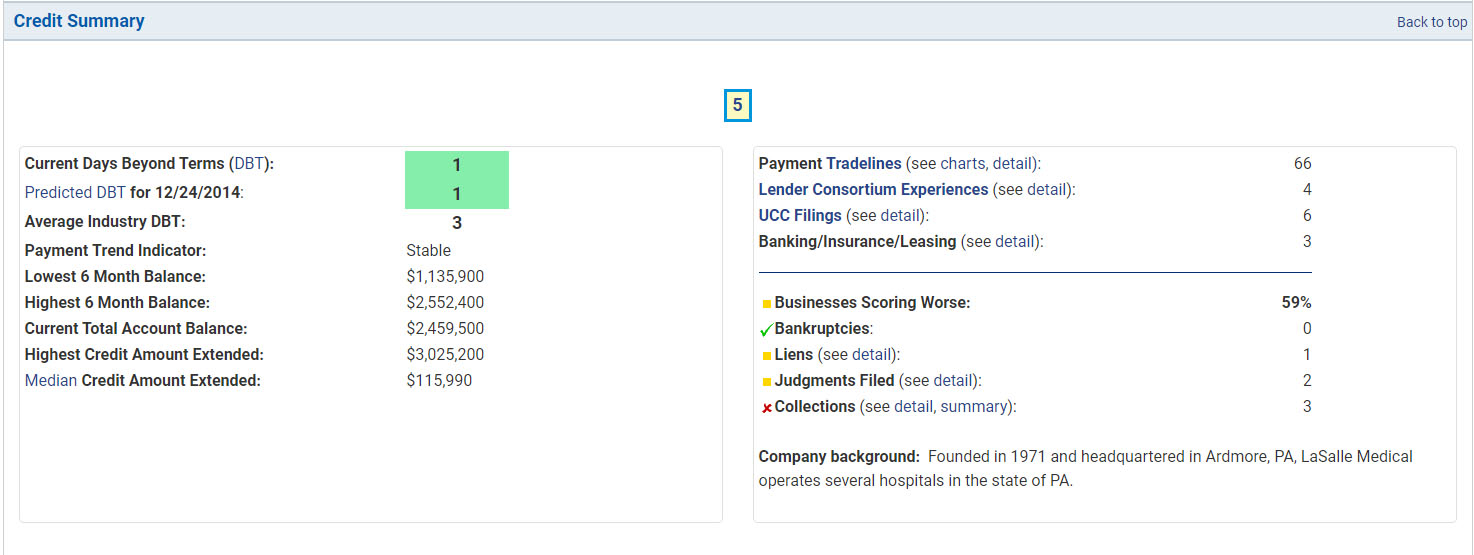

Credit summary

This section of your business credit report is a quick overview of various aspects of your credit. It will provide a summary of your loan payment history and reflect how you utilize your credit accounts. It will typically also include information on UCC liens for any assets pledged as collateral.

Credit reports often include a summary of your credit history, such as this one on a sample Experian credit report.

(Source: Experian)

Common items covered in this section include:

- Days Beyond Terms (DBT): This indicates how many days past the due date your firm pays. Your DBT figure may be reflected as your current, average, or historical worst.

- Account Balances: How much credit you’re using will be summarized here, including the balance of your accounts and the amount of available credit you can use. This section may also include data on your highest balances in a given period.

- Number of Tradelines: The total number of credit accounts will be displayed here. Accounts can include credit cards, loans, lines of credit, and leases.

- UCC Filings: If collateral has been pledged in exchange for financing, it may appear in this section.

- Derogatory Information: Negative payment history will be displayed here and can include late payments, collections, and bankruptcies.

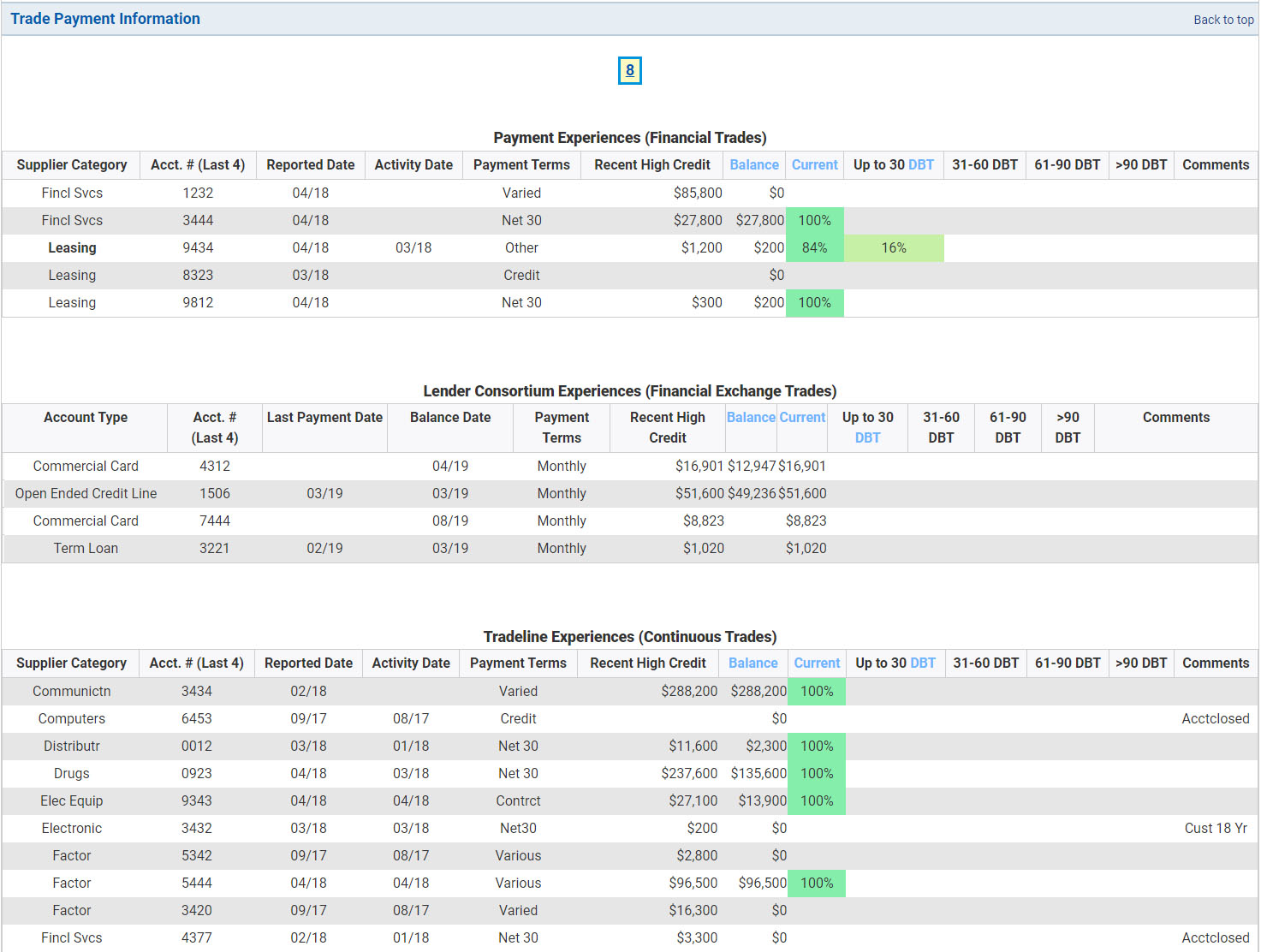

Account payment history

This section of your business credit report provides a detailed look at each individual account as reported by your creditors. It outlines key information such as payment activity, outstanding balances, credit terms, and amounts due, offering insight into how consistently your business meets its financial obligations. The more accounts that show you pay on a timely basis, the easier it will be to build business credit.

Your business credit report will also show details of individual tradelines. (Source: Experian)

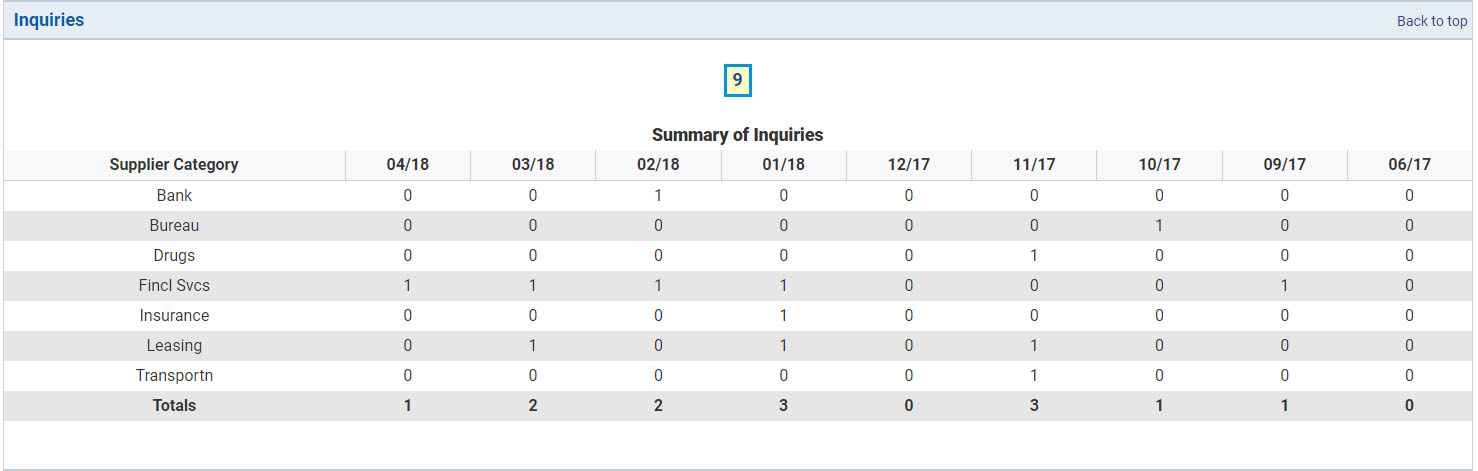

Credit inquiries

This section shows when your business credit report has been accessed in connection with a credit application or financing review. In many cases, lenders check your report as part of their decision-making process, and those requests are recorded as credit inquiries. Experian, for example, displays inquiries from the previous nine months and categorizes them by the types of businesses that reviewed your credit. Depending on the provider, your report may show inquiries going back further than nine months.

Creditors and other companies that have checked your credit will appear in the credit inquiries section of your credit report. (Source: Experian)

In general, a high number of recent credit inquiries may be viewed as a sign of elevated risk. Lenders may interpret frequent inquiries as an indication that a business is seeking additional financing due to cash flow strain or limited access to credit. By contrast, fewer inquiries may suggest a more stable credit profile, although they are only one factor considered in an overall lending decision.

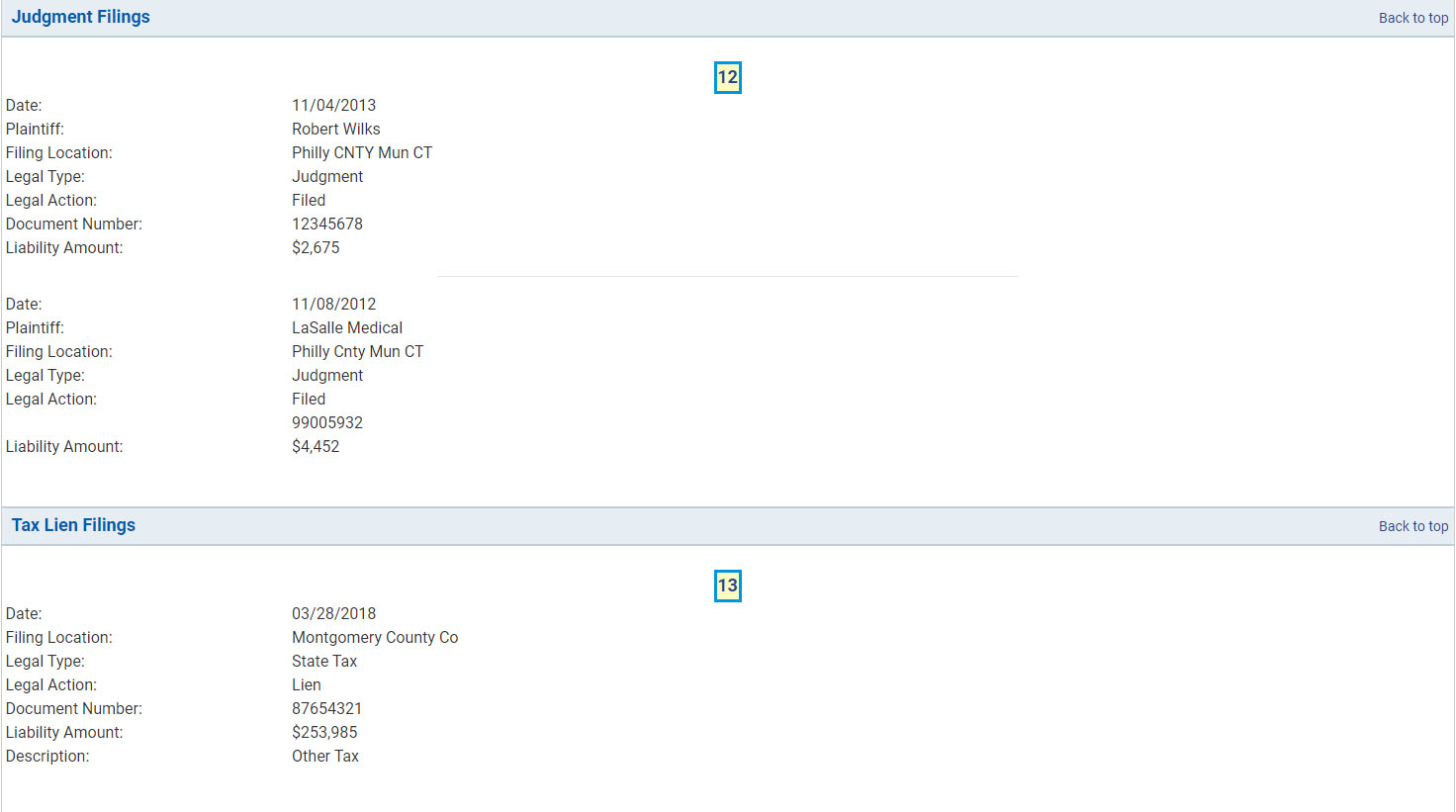

Significant derogatory information

This section highlights serious negative items that may affect your company’s credit profile. In addition to late payments, it often includes matters such as tax liens, collections, judgments, and bankruptcy filings, although some credit bureaus may present these records in separate categories.

Derogatory information often has its own section on your credit report. (Source: Experian)

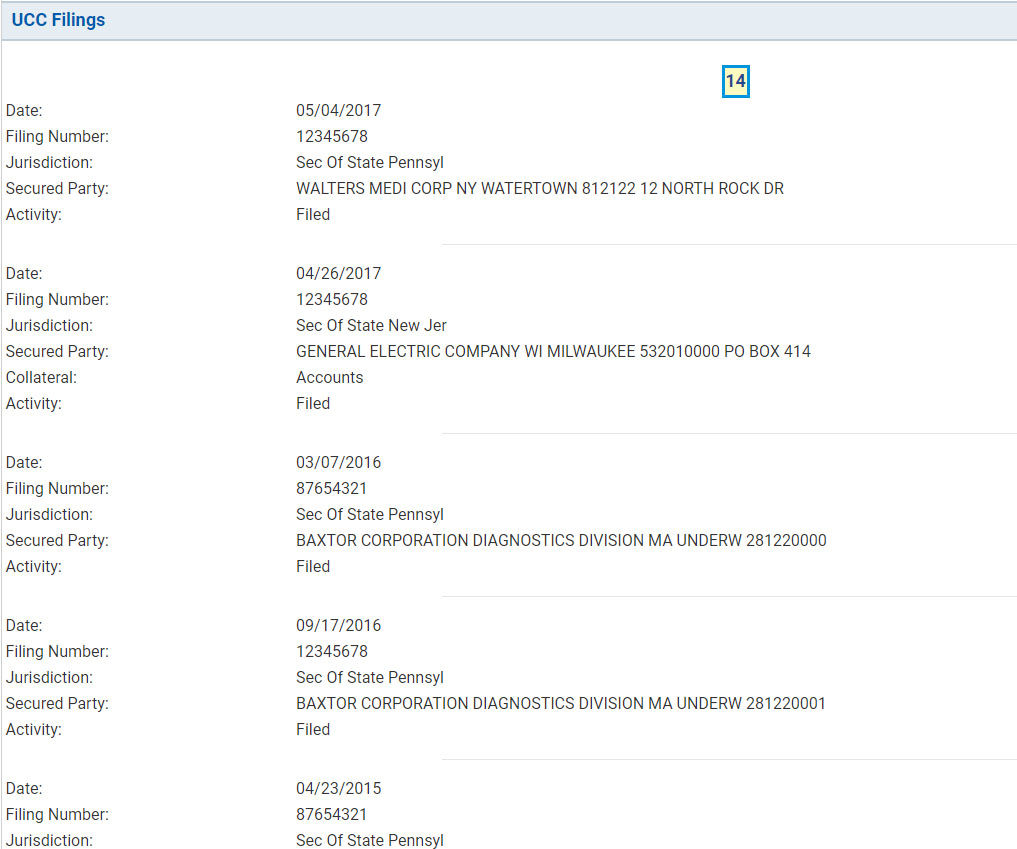

UCC filings

UCC filings reflect whether a business has pledged assets as collateral for financing. These records may include details such as the filing date, the type of collateral involved, and the secured party, giving other lenders visibility into existing claims against the company’s assets.

Any assets pledged as collateral can be listed under the UCC filings section of your credit report. (Source: Experian)

UCC filings are used to lower the risk of lending money by claiming a public interest in the collateral, allowing the party to take legal possession of it in the event of a default. Common types of collateral that can be pledged include:

- Accounts receivables

- Contracts

- Business equipment

- Inventory

- Leases

- Notes receivable

How business credit reports are used

Business credit reports are primarily used for three purposes. They’re used to verify identity, evaluate whether your company will be approved for a loan, and determine the rates and terms you’ll get.

1. Business verification

Business credit reports are often used to confirm key details about a company, including its identity and basic business information. Lenders compare the report against your loan application and supporting documents to check for inconsistencies, verify that they are evaluating the correct business, and help ensure that any approved funds are released to authorized parties.

2. Loan approval

Business credit reports give lenders insight into a company’s financial obligations and repayment history. This information helps them assess whether the business is likely to manage additional debt responsibly, making it an important factor in determining whether financing will be approved.

3. Rates & terms

If financing is approved, the details in your business credit report can influence the rates and terms you’re offered. Strong credit and a consistent payment history may help you qualify for more favorable terms, while higher risk profiles may result in higher costs or more restrictive conditions.

Where to get your business credit report & business credit scores

The following are four providers that you can visit to get a copy of your business credit report. Each has additional products and services to help you monitor your credit and track your business credit score.

Keep in mind that since your credit report is simply a snapshot of data last reported from lenders, the information you see may vary among the different providers.

1. Dun & Bradstreet

D&B is one of the most commonly used credit bureaus by lenders. It offers different types of business credit scores and multiple services to help companies monitor their credit. You can read our guide on the D&B credit report to learn more.

- PAYDEX® Score: This score ranges from 0 to 100 and is determined by a company’s past payment performance. Higher scores are correlated to companies that pay bills early or on time. Scores of 80 and above are generally considered to be low risk.

- Delinquency Predictor Score (DPS):Measured on a scale from 1 to 5, with lower scores indicating lower risk, the DPS is meant to show the probability that a business might become delinquent.

- Failure Score: This also operates on a scale from 1 to 5 and is designed to reflect a company’s likelihood of filing bankruptcy or encountering financial difficulties within 12 months.

- Maximum Credit Recommendation: As the name suggests, this gives creditors a guideline on how much credit to extend based on a company’s industry, payment history, and other characteristics.

- D&B Rating: This is an overall rating of a company’s creditworthiness and is determined by information from a company’s balance sheet and overall size.

2. Experian

Experian provides the Intelliscore Plus business credit score. The most recent version, Intelliscore Plus V3, ranges from 300 to 850, with higher scores indicating lower risk. Experian also offers blended scoring models that incorporate both business credit data and the personal credit information of business owners.

Earlier versions of Intelliscore Plus used a scale from 1 to 100, with higher scores representing lower risk. In general, scores above 75 were considered to indicate a lower likelihood of delinquency.

3. Equifax

Equifax has two main types of credit scores lenders can utilize.

- Business credit risk score: This is the likelihood of a business being over 90 days late on financial obligations. The range is from 101 to 992, with 992 being the least likely.

- Business failure score: This is the risk that a business will go bankrupt in the next 12 months. Scores range from 1,000 to 1,610, with 1,610 being the least likely.

4. FICO Small Business Scoring Service (SBSS)

The FICO SBSS score is commonly used by lenders, including for certain Small Business Administration (SBA) loan programs, to evaluate creditworthiness. Scores range from 0 to 300, with higher scores indicating lower risk.

For SBA 7(a) loans, the SBA often uses a minimum SBSS score threshold (historically around 155) for prescreening purposes, although the exact cutoff can vary by lender and loan program.

FICO SBSS scores are not directly available to consumers through FICO. However, some third-party platforms, such as Nav, may provide estimated or modeled versions of your SBSS score rather than the exact score used by lenders.

Frequently asked questions (FAQs)

A personal credit report typically only contains information related to yourself as an individual, whereas a business credit report contains information on debt and other tradelines which your business is liable for. The type of report a lender uses may depend on whether the company’s finances are sufficient to qualify alone or if a personal guarantee is required.

I recommend checking your business credit report no less than once every three to six months. You can also consider enrolling in credit monitoring services, some of which are free and designed to alert you of any material changes to your credit profile.

No. The information you see on your credit reports can differ if creditors decide to report data only to certain credit bureaus. Additionally, different credit bureaus may occasionally experience a delay in reporting or receiving data.

Inaccuracies in your business credit report can make it difficult for your company to get funding. For example, the information in your credit report is used to determine your credit score, one of several factors that can impact your ability to get approved for a loan as well as the rates and terms you can get.

Bottom line

Your business credit report plays an important role in financing decisions, including whether your application is approved and the rates and terms you may receive. Understanding how to read your report and what information it includes can help you better evaluate your credit profile and identify opportunities to strengthen it.

Dun & Bradstreet, Equifax, Experian, and Nav are among the providers that offer access to business credit reports and scores. Many also offer credit monitoring tools that can help you track changes to your report over time.

Source link