The FED simply lowers the rates – will mortgages will ever fall to 3%again?

For the first time in nine months, the Federal Reserve lowered its benchmark interest with a quarter -time percentage, which resulted in the rate of the central bank to a reach of 4% to 4.25%.

It is a long -awaited and highly disputed movement, as president Donald Trump has repeatedly a summoned chairman Jerome Powell To reduce the loan costs for besieged home builders and buyers, many of whom desire the days only a few years ago when the bench market rates were almost zero.

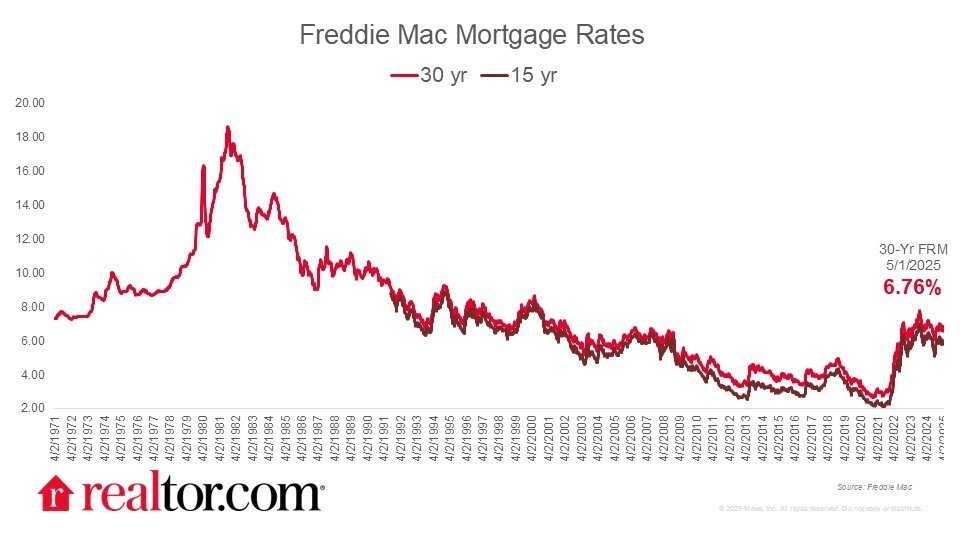

The mortgage interest rate fell below 3% for the first time in 2020 and eventually reached a low of 2.65% in January 2021.

But although the decisions of the Fed will certainly make some relief to homeowners, home buyers and sellers, do not count on an interest of 3% that takes place quickly.

“The unprecedented circumstances that have activated these historically low rates will probably not be repeated,” says Hannah Jonessenior economic research analyst at REALTOR.COM®. “It is unlikely that the rates will fall to 3%in the near future.”

Nevertheless, millions of home buyers hope that the mortgage interest rate could return to the lows during the Pandemic era of COVID-19. The reality, according to economists and mortgage professionals, is that waiting for those rates to return can cost more than it saves.

An anomaly of the Pandemic era: how the speeds fell so low

“The 3% rates from a few years ago were a deviation, not normal market conditions,” says Carlos ScarperoA mortgage broker at Edge Home Finance. “Unprecedented and not a normal market.”

So how did we get there?

In March 2020, when the Coronavirus Pandemie was stopped and raised the economy, the Federal Reserve reduced interest rates to almost zero. It was the most dramatic step of the central bank since the 2008 financial crisis, and it had an immediate wrinkle effect on the mortgage interest rate.

At the time, the mortgage interest rate was already low due to the continuing effects of the 2008 collapse. But after the emergency intervention of the FED, the rates fell even further. By the summer of 2020 they had fallen below 3%. Subsequently, in January 2021, the average fixed mortgage interest rate of 30 years reached a record low of 2.65%.

Could 3% rates ever return?

The most recent reduction in the FED is already largely priced in the mortgage interest rate, so that they have been brought to a lowest point of 11 months of 6.35% for the FED decision. Whether they will fall further depends on the future actions of the FED, but many economists do not expect them to fall below 6%.

That is unwanted news for house hunters in the hope of returning to the days of the 3% mortgage.

The era of Ultralow Hypotheek interest rate has fueled a housing tree that was no longer seen since before the 2008 crisis. Cheap loan costs gave millions of buyers access to houses that would otherwise have been out of reach.

Although everything is possible in theory, the experts with whom we spoke are saying that a return to 3% mortgage interest is very unlikely without another major economic shock.

“The rates as low as we saw during the Pandemie are very unlikely,” says Michael Merrittsenior vice president Bok Financial. “A dramatic economic event in a scale would be needed if the pandemic or financial crisis to push the rates so low again.”

Kevin LeiboWitzPresident and CEO of Grayton MortgageIf it agrees: “There will be a very low probability – in the short term to zero. We will have to wait until the next big crisis, which I really don’t want.”

An important reason? The Federal Reserve remains committed to combating inflation, which has been a persistent thorn on the part of the central bank. The August -Consumer price index rose by 2.9% year after year, an increase of 0.4% compared to the previous month.

Fighting inflation as sticky as that means that the interest rates are kept well above zero-the same zero-bound area that helped to stimulate mortgage interest in 2020 and 2021. And without another Black Swan event, the FED has little incentive to lower the rates to the levels needed to return to return to register Lages.

And even if those rates returned, they would have come to a steep prize: widespread economic pain.

Why hope can be 3% counterproductive

It is easy to see why many potential buyers are on the sidelines. More than 80% of the mortgages nowadays have an interest rates of sub-6% and 3% rates are hardly in the rearview mirror. But experts warn that playing the waiting game can be a precious mistake.

Staying from the market in the hope of a tariefization that never comes, can lead to missed opportunities: rising house prices, rent increases and inflation can surpass any future savings on interest. And as rates Doing Falling again, buyers can get a completely different challenge for a completely different challenge: rising competition.

“If the rates ever fell to 3%, we would see a housing leg rider,” says Scarpero. “This would increase the prices even further.”

That scenario could leave many of the cautious buyers today, all over again priced from the market.

Reframing expectations

The problem with real once-a-lifetime opportunities is that they, well, happen once in your life-and it should not be the benchmark for your future. If you wait until a rate of 3% returns before you buy a house, it might be time to shift your expectations.

“The reframe is that the current rate is the reality speed,” says Scarpero. “And we just have to get used to it.”

That means making peace with higher loan costs and plans accordingly. You can end with a smaller house or a longer -term work traffic than you had originally suggested. But buying a house is still one of the most powerful ways to build long -term wealth.

“House buyers must adjust their expectations to only buy what they can afford based on current rates,” says Leibowitz. “Waiting for 3% is a bad plan.”

In the current market there is no room for Wishful Thinking. Flexibility and financial realism are the keys to get ahead.

The bigger picture: it’s not just the rate

Yes, your mortgage interest rate is important to influence your monthly payment and long-term costs. But it’s just one part of the comparison.

“The mortgage interest rate is only one factor that influences the affordability of homes,” says Merritt. “Rising insurance costs and real estate tax are [also] contribute to affordability issues. “

And then there is the inventory crisis, which is perhaps an even greater barrier than the interest rates themselves.

“There have just not been enough new houses built since the financial crisis,” says LeiboWitz. “The range of houses is not where it should be.”

Scarpero agrees: “The pricelessness problem has been there for a while, and most is due to a lack of inventory and home builders who do not keep up with the demand.”

A mortgage interest of 3% was not normal. It was a gift of extraordinary economic conditions. Waiting for it to return can mean that the real opportunities are now missing.

Instead of pursuing yesterday’s rates, you concentrate on what the current market can offer you: a stable place to live, the chance to build equity and a house that reflects your life – not just your loan.