What to expect from the US housing market in 2026

The answer, according to Kushi, lies in six forces shaping the outlook: affordability, demographic demand, regional divergence, local tension, rising inventory and the continued benefit to new housing.

Affordability and demographics

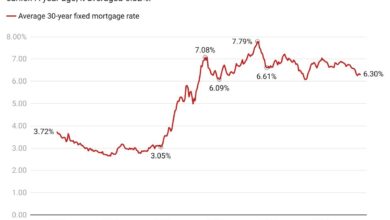

Mortgage rates are expected to remain in the low 6% range next year, according to a report published this week by First American Data & Analytics.

That alone won’t unlock the market, Kushi said, but cooling home price growth combined with income gains should continue to increase affordability.

The report shows that price growth has already slowed to the weakest pace since 2012. If this trend continues, Kushi says markets with growing inventories and modest price reductions will see more buyers emerge again.

By Kushi’s estimate, the U.S. recorded about 4 million fewer existing home transactions between 2022 and 2025 than the five-year average before COVID-19. Yet the demand is far from exhausted.

She added that nearly 52 million Americans are in their 30s, and many are entering a homeownership-driven phase of life. Even without major shifts in mortgage rates, family changes, job moves and downsizing are expected to keep transactions rising steadily through 2026.

Regional differences must remain strong

Inventory trends remain mixed. Kushi said the Midwest and Northeast continue to have tight supply for both new and existing homes, keeping prices relatively firm.

Meanwhile, many southern and western metros have more active inventories than before the pandemic. Markets like Austin and Tampa saw strong price increases during the post-pandemic boom, followed by slower migration and affordability issues.

The construction of new homes in these regions has given buyers more choice and increased the cooling-off period.

Most analysts expect a “two-speed” market in 2026: tight conditions in the Northeast and Midwest, accompanied by softer conditions in parts of the South and West. And rising insurance costs could add further pressure in some coastal areas.

Indicators of financial distress have risen from record lows but remain well below crisis levels.

Kushi said weaknesses are concentrated in areas with limited affordability, higher insurance costs or slower job growth, along with households that have thinner financial buffers.

“The labor market has cooled but not cracked, and homeowners still have a very large equity cushion, so risk remains limited,” Kushi said.

“By 2026, the pressure should be localized. Prices are falling in some Sun Belt and Western metros that rose sharply during the boom, and recent buyers with small down payments are more vulnerable if prices fall. We will keep a close eye on the labor market, but the base case is a gradual normalization, rather than a broad surge.”

Inventory and construction benefit

The supply shortage eased in 2025 as more homeowners accepted higher financing costs and builders completed more homes.

Kushi said life events – but not just interest rate shifts – should encourage more owners to go public in 2026. Lower interest rates would help margins, but the easing of the lock-in effect is expected to be gradual.

Single-family home construction has cooled, but builders are still benefiting from move-in ready homes and incentive flexibility.

Many buyers remain wary of selling a home with a low mortgage rate and entering a more expensive market, keeping their focus on new homes where sellers can buy up or offer help with closing costs, Kushi added.

She said the new construction segment is positioned to maintain its lead because supply is available and builders can quickly adapt to changing demand.

“The housing market will enter 2026 on a more stable footing,” Kushi said. “We expect affordability to improve, mainly because prices cool and wages rise, not because financing suddenly becomes cheap. Demand is driven by milestones rather than spreadsheets.”