What does a reduced rate mean for the mortgage interest for the mortgage interest rate?

In response to increasing warning signals from the labor market, the Federal Reserve is preparing to lower its benchmark interest for the first time in nine months.

Most economists and investors expect Fed Chair Jerome Powell And the rest of the Federal Open Market Committee (FOMC) to reduce the overnight rate of the Central Bank on Wednesday by a quarter point.

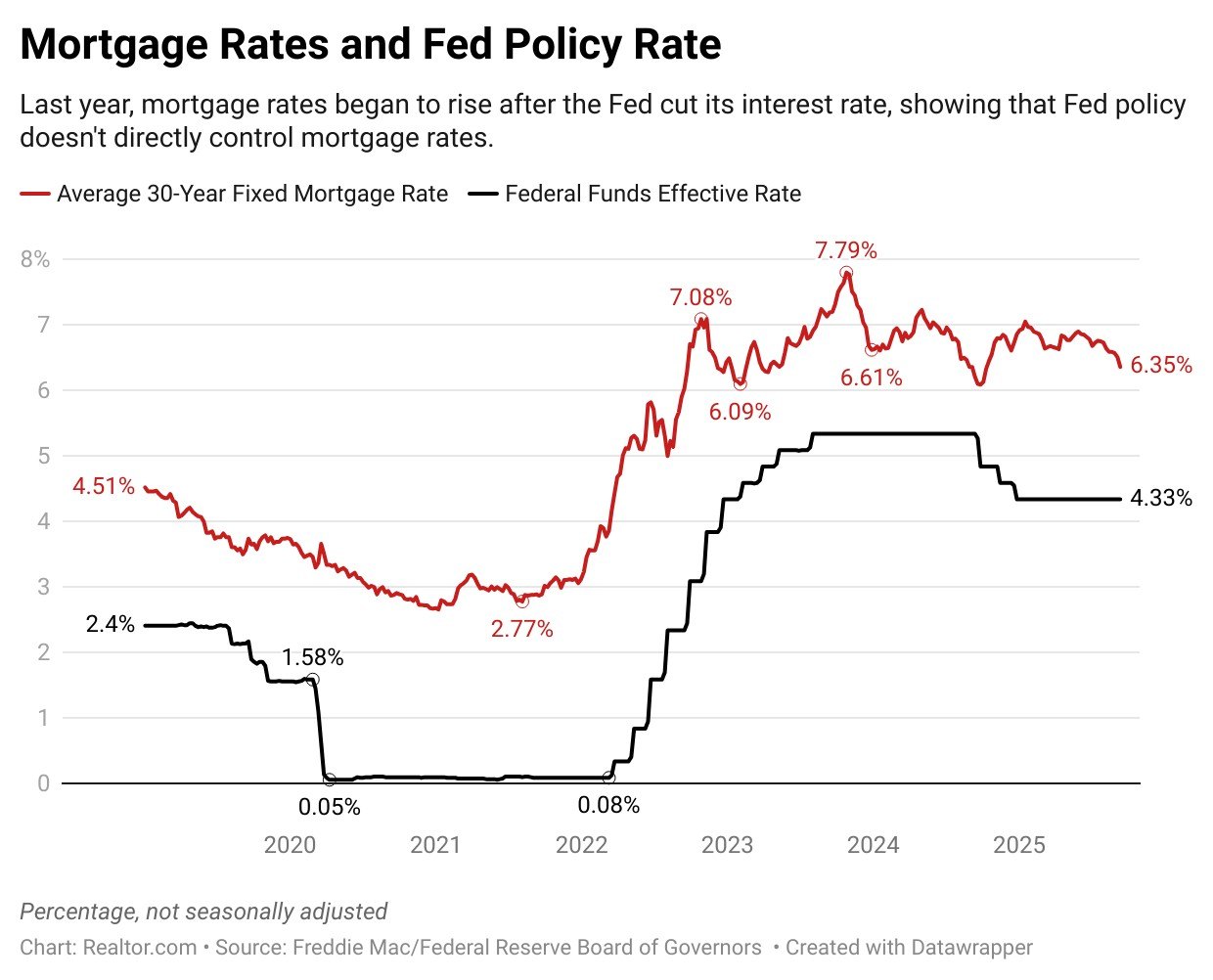

The mortgage interest rate has already fallen pending the move, with the average fixed rate of 30 years last week reaching a low of 11 months of 6.35%.

It comes as welcome news for potential home buyers, who benefit from the lower loan costs. For those who maintain that the mortgage interest will automatically fall further after the FOMC meeting, the disappointment can wait.

That is because financial markets have already priced in three 25-Bash-Point FED cuts before the end of the year, and three further cutbacks of that size by the end of 2026.

“This means that the markets have high expectations for the coming tariff reductions of the FED, and the market can be very well disappointed by a slower pace,” says Realtor.com® Chief Economist Danielle Hale.

If the FOMC decision is controversial and split, with different voices against the reduction, or if policy makers provide forward guidelines that do not correspond to the expectations of the market for future rate reductions, the mortgage interest rate can go higher in response.

A similar scenario took place in September 2024, when the mortgage interest rate dropped to a lowest point in two years prior to the expected decreases of the FED rate, but then the rates began to rise, because it became clear that the FED cuts would not be as extensive as the expected markets.

Although the mortgage interest rate has fallen in recent weeks, they have not yet reached the lows almost 6% at the beginning of September 2024 – when the federal fund percentage was a full percentage point higher than it is today.

“I expect this drop [in mortgage rates] To continue at least until the upcoming FED meeting, “says Hale.” After the FED meeting, however, I expect that the mortgage interest rate is steadily or even higher, because markets are able to expect relatively more relaxation and can be disappointed by the forward guidance of the FED. “

The FED does not set a mortgage interest that tend to follow the proceeds of long -term bonds. These bond markets are influenced by the expectations of investors about the future policy of FED and financial circumstances, including inflation and government deficits.

In a phone call with reporters last month, National Association of Realtors® Chief Economist Lawrence Yun Warned that higher inflation and worries about setting up government debt can exert on an upward pressure on the mortgage interest rate, despite the relaxation of the FED.

“The mortgage interest rate should not fall, not even with the reduction of the Fed, if there is high inflation, and also if the issue of debts somehow becomes great,” he said. “That will prevent mortgage interest from falling meaningfully.”

Political drama surrounds the decision of the FED’s interest rate

The Fed has long made it difficult to maintain its independence of political pressure or influence, but that tradition has been challenged by the president in recent months Donald TrumpThe public printing campaign for lower rates.

Shortly after the start of his second term, Trump began to demand lower rates publicly, at various points that are in danger of dismissing or sue Powell. Trump has said that lower rates would help the government to refinance its enormous debt on favorable conditions and also stimulate the housing market.

Powell, however, opposed Trump during a meeting of the White House in May that the future decisions of the Central Bank about interest rates “would be based solely on careful, objective and non-political analysis,” said a FED statement about the meeting.

The impasse has been intensified in recent weeks with Trump’s attempt to dismiss Lisa Cook of the Federal Reserve Board of Governors for accusations of mortgage fraud.

Cook, a Biden -appointed, had supported Powell to keep the rates stable the last time the FOMC voted on policy at the end of July. She is currently fighting Trump in court and is expected to vote on Wednesday after a judge temporarily blocked the president’s attempt to remove her.

The FOMC normally has 12 voting members, but has currently fallen to 11 after Board of Governors member Adriana Kugler Dismissal last month and without explanation.

The resignation of Kugler, also a Biden -appointed, gives Trump an opening to add a new voter to the FOMC who is sympathetic to his vision of easy money.

The replacement he has nominated, economic adviser to the White House Stephen MiranCan be confirmed in a senate voice on Monday evening, so that he can participate in the FOMC meeting this week.

If confirmed, Miran would be the first sitting White House officer on the board of the FED in modern history, crushing the precedent and adding a new political dimension to the administration of the central bank.

Why the Fed now lowers the rates

The FED uses higher rates to curb inflation and the lower rates to stimulate the labor market, the two halves of its double mandate to maintain steady prices and maximum employment.

With reference to the fear of persistent inflation, FED policy makers have kept the policy percentage of the Central Bank stable since December with a reach of 4.25% to 4.5%.

Now a series of alarming reports that reveal weakness on the labor market is finally encouraged to act – as well as giving Trump and other critics support for their claim that the Fed has waited too long to act.

The first blow came in early August, days after the last FOMC meeting, when the Labor Department released a sharp downward revision to earlier job growth figures for May and June.

Subsequent revisions show that the economy has added only 27,000 new jobs every month from May, far below the 100,000 pace that is seen if necessary to prevent rising unemployment.

There are also more unemployed jobseekers than vacancies in the country for the first time since 2021. And last week new unemployment claims, a sign of dismissals, jumped to their highest level in four years.

All this offers the FED sufficient reason to lower the rates. At the same time, however, inflation started to raise its head again, with the total inflation that rises 2.9% annually in August and the FED presents with a thorny dilemma.

“Although inflation has occurred and remains above the target of 2%, the Federal Reserve gives more weight to the labor numbers and it will lower the rates to prevent further deterioration,” says Bright MLS Chief Economist Lisa Sturtevant. “Since inflation is still above the goal, I expect that we will see a 25-based point-snit, and not something bigger this month, while future tariff reductions can be more dependent on the inflation process.”