The housing markets are seeing the sharpest house price declines

House price growth has slowed to 0.9% in December 2025, but many markets are only seeing a decline.

Annual home price growth of less than 1% is one of the softest rates since the recovery from the Great Recession, according to new insights into U.S. home prices. report from data research firm Cotality.

“We are seeing a significant departure from the rapid gains of recent years; while upward pressure on prices remains, momentum has dampened enough to suggest the market is finally becoming more navigable for potential buyers,” says Cotality’s chief economist. Selma Heppthe report said.

The South and the West are hit the hardest. Negative price drops are the norm here. Florida, Texas, Colorado, Washington, DC, Hawaii, Arizona, Utah, Oregon and California have seen the sharpest declines in Cotality’s Home Price Index (HPI), which predicts the risk of recession in metro areas by analyzing multiple market segments and 45 years of home price trends using proprietary statistical models.

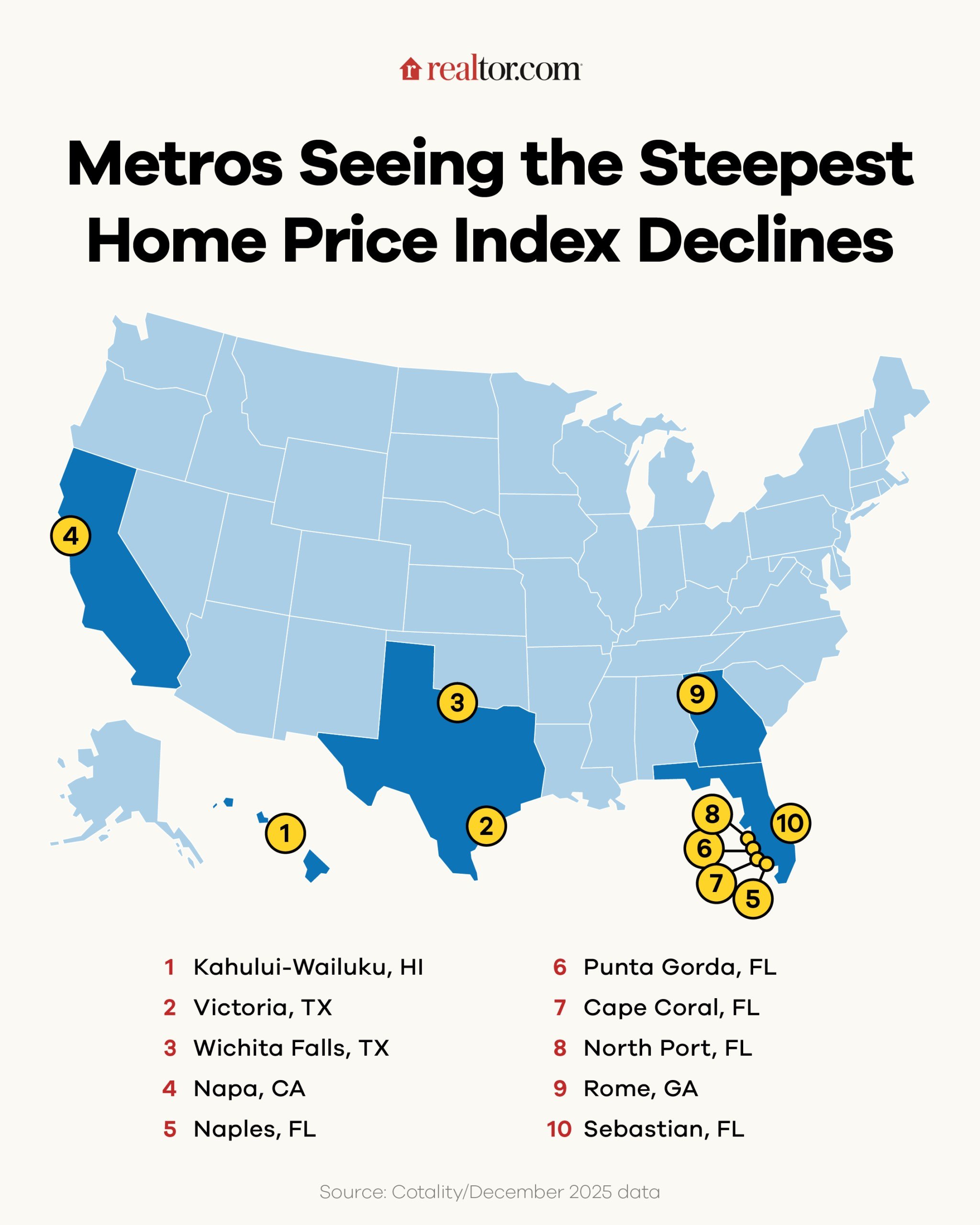

The coolest markets with the sharpest HPI declines are Kahului-Wailuku, HI; Victoria, Texas; Wichita Falls, Texas; Napa, CA; Naples, FL; Punta Gorda, FL; Cape Coral, Florida; North Harbor, FL; Rome, Georgia; and Sebastian, FL.

Punta Gorda also saw the largest share decline: -7.97%, with an average drop in value of $26,624.

Why are home valuations falling?

Much of this is attributed to higher inventory levels and slowing immigration in markets that previously saw rapid expansion, the report said.

During the COVID-19 pandemic, when mortgage rates were at historic lows, people in urban areas rushed into many of these markets that were now approaching or in recession — especially Florida and Texas — as they looked for more space and fewer restrictions, driving prices to unsustainable levels.

These markets are now undergoing a hard correction, especially in Florida. The Sunshine State takes up half of the spots on the list.

Cotality calls the declines a “return to a long-awaited normalization, driven by economic and housing fundamentals. The frenetic bidding wars and double-digit price increases of recent years have given way to a market where buyers and sellers are having to gradually adjust their expectations.”

This is already happening in Florida.

“As sellers lose leverage in this environment, they become more realistic in their pricing,” said agent Douglas Elliman Michael Merrillwho works in Vero Beach, says Realtor.com®.

Even as billionaires flock to the state for friendlier tax policies, the average resident faces a loss of equity on top of higher (but stabilizing) housing costs.

“The reason [Florida] homes have lost their value due to higher inventory, less migration to the area and sellers overpricing homes,” he adds Brenden Rendoa strategic real estate advisor with Real Estate Bees serving Central Florida.

The Sunshine State takes the top five markets most at risk of continued future declines: Cape Coral, Lakeland, North Port, Palm Bay and even West Palm Beach, which has seen an influx of luxury developers.

Two Texas metros are in the top three markets and are experiencing a hard correction: Victoria and Wichita Falls.

Real estate investor from Los Angeles Jameson Tyler Drewwho witnessed the exodus of California residents to Texas during the pandemic, says many people — both current and potential residents — are disenchanted with the Lone Star State because it is no longer as affordable as it used to be.

“Texas’ shine seems to be fading pretty quickly as prices have risen in recent years,” he tells Realtor.com. “People I’ve talked to have noticed that property taxes are higher than California’s, and their commutes are getting longer. Now people leaving California are just going straight to Midwestern cities.”

He mentions Milwaukee, Indianapolis and even Chicago as places where California transplants are looking for more affordable pastures. Others are looking for cheaper areas in the Golden State, including Fresno and Bakersfield-Delano.

Hawaii and Napa in recession?

A pair of unexpected metros – both pricey and known for their beauty – had two of the steepest HPI drops: Kahului-Wailuku, HI (No. 1) and Napa, CA (No. 4). They have average list prices of $1,049,500 (down from $1.42 million in August 2023) and $1,304,500 (down from $1.79 million in June 2023), respectively.

In January, 10% (188 listings) and 11.6% (56 listings) of listings in Kahului-Wuiluku and Napa, respectively, saw price reductions, according to data from Realtor.com.

Cotality‘s foremost economist, Thom Maloneattributes the HPI declines in these two coveted markets to the cost of home insurance.

“Hawaii’s insurance costs have skyrocketed in the wake of the 2023 fires, and Napa is the same story, with most of the county classified as at very high wildfire risk,” he tells Realtor.com.

‘The price drop is necessary to compensate the buyer for the damage [rising] insurance costs, as the attractiveness of the areas has otherwise not changed.”

Kahului-Wailuku, Hello

HPI percentage drop: 8%

Median list price: $1,049,500

Victoria, Texas

HPI percentage drop: 7.4%

Median list price: $276,100

Wichita Falls-TX

HPI percentage drop: 7.2%

Median list price: $199,575

Napa, CA

HPI percentage drop: 7.1%

Median list price: $1,304,500

Naples, FL

HPI percentage drop: 6.8%

Median list price: $729,725

Punta Gorda, FL

HPI percentage drop: 6.2%

Median list price: $384,750

Cape Coral, FL

HPI percentage drop: 6.2%

Median list price: $399,949

Northhaven, FL

HPI percentage drop: 5.9%

Median list price: $479,900

Rome, GEGA

HPI percentage drop: 5.2%

Median list price: $296,950

Sebastian, FL

HPI percentage drop: 5.2%

Median list price: $442,725