The government’s closure adds uncertainty to the housing market, since the mortgage interest rate assumes

The federal government is closed for the first time in more than seven years this week. The last 35-day episode ensured that the sale of houses to ebb, although they recovered afterwards.

The closure directly influences some transactions because the National Flood Insurance Program no longer issues new policies. The majority of housing sales should not be influenced, but others may be confronted with potential delays as a result of limited staff at various agencies. And although it is difficult to measure, the closure is probably a resistance to the confidence of the consumer.

An important pain point is the lack of new data. The September -work report, planned for Friday, is delayed, so we do not know how recruitment and unemployment officially transported in the past month. Private data showed softer recruitmentand the Job Omzetr report from Augustus showed recruitment and divorces in accordance with recent trends. This makes it more difficult for both markets and policy makers to assess what is going on and positioning for what awaits us.

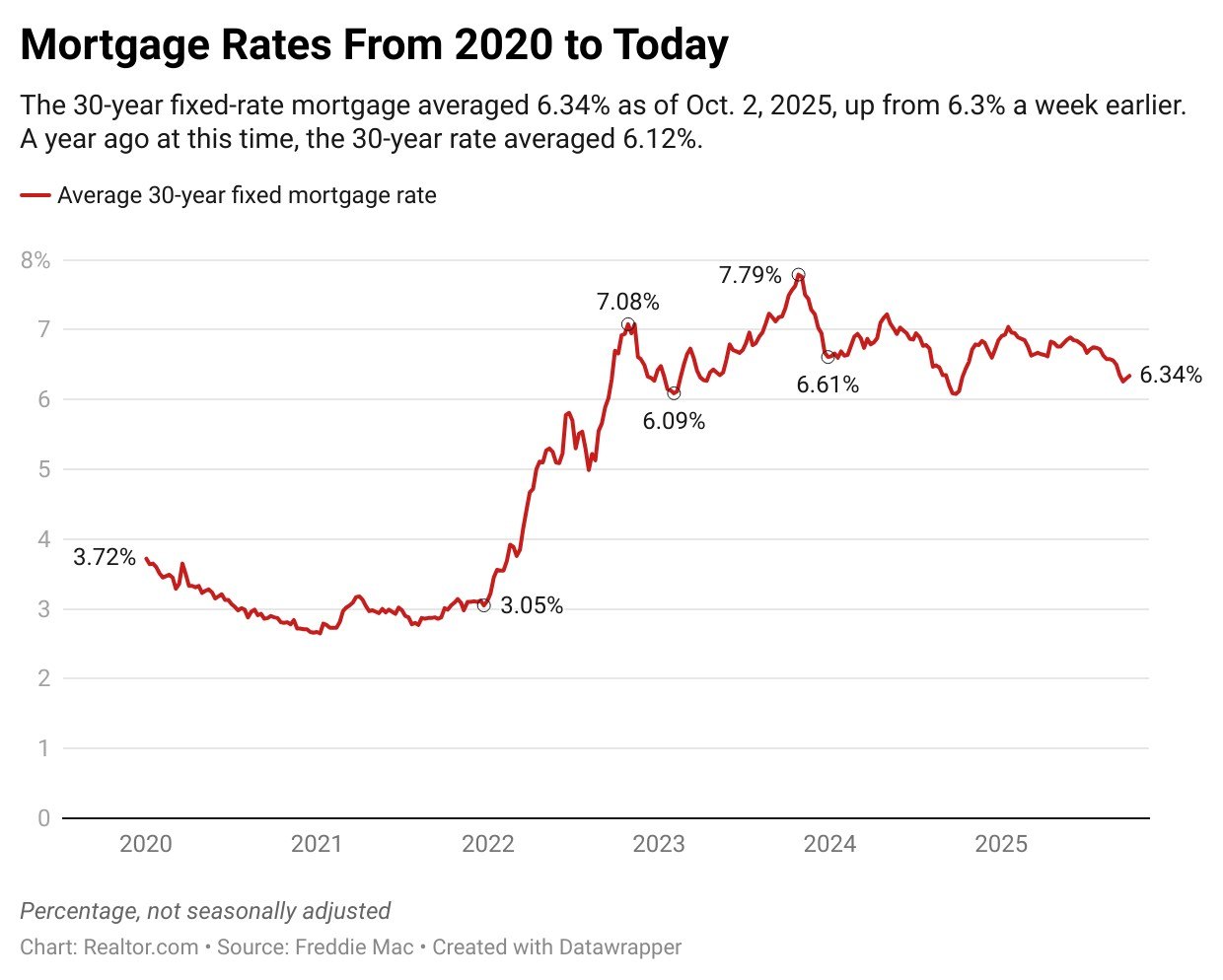

The mortgage interest rate is stuck this week, but remain in the low 6% for a fourth week, because markets digest the closure and try to praise its impact. Since the mortgage interest rate has remained relatively high the majority of 2025, home sales have remained low and the rate for outstanding mortgage debt for homeowners is hardly specified. In fact, 80% of homeowners with a mortgage still have a rate of less than 6%.

In the meantime, pending housing sales were picked up in August when buyers responded to the dip in the mortgage interest rate. A slower pace of the growth of house prices undoubtedly also improved affordability.

REALTOR.COM® September housing details suggest that price purity has largely continued, with the list of fixed prices and the price reduction in comparison with last year. Deeper digging, we see that price reductions occur more often in lower price strokes are rural and rarer between houses of a million dollars. These trends are generally, but not universal, where also at the local level, which suggests that both affordability and regional trends are probably drivers of this pattern.

Weekly housing data underline the price stability and also emphasizes a loss of sales momentum, with new offers falling and active growth from the list conceal.

As we approach the best time to buy nationwide, some markets are already there, with areas such as Atlanta, Austin, TX and Chicago that close their best week while Las Vegas stands out for top conditions next week.

Finally, you will probably know when you see it, but what is a luxury house? And what is the dividing line between purely high-end and ultra-luxe?

We dug in the data to see how the definition of luxury has evolved. The luxury threshold is now more than a million dollars rural, or about three times the current median house price. High-end luxury starts at $ 2 million, while Ultraluxury starts above $ 5 million hurd many multiples of the typical house price.