Mortgage rates today: Mortgage rates fall to 6.23% as the split Fed signals another cut

Mortgage rates fell on Wednesday as markets awaited the release of more economic data that was delayed by the government shutdown. Federal Reserve seemed to be leaning towards another interest rate cut in December.

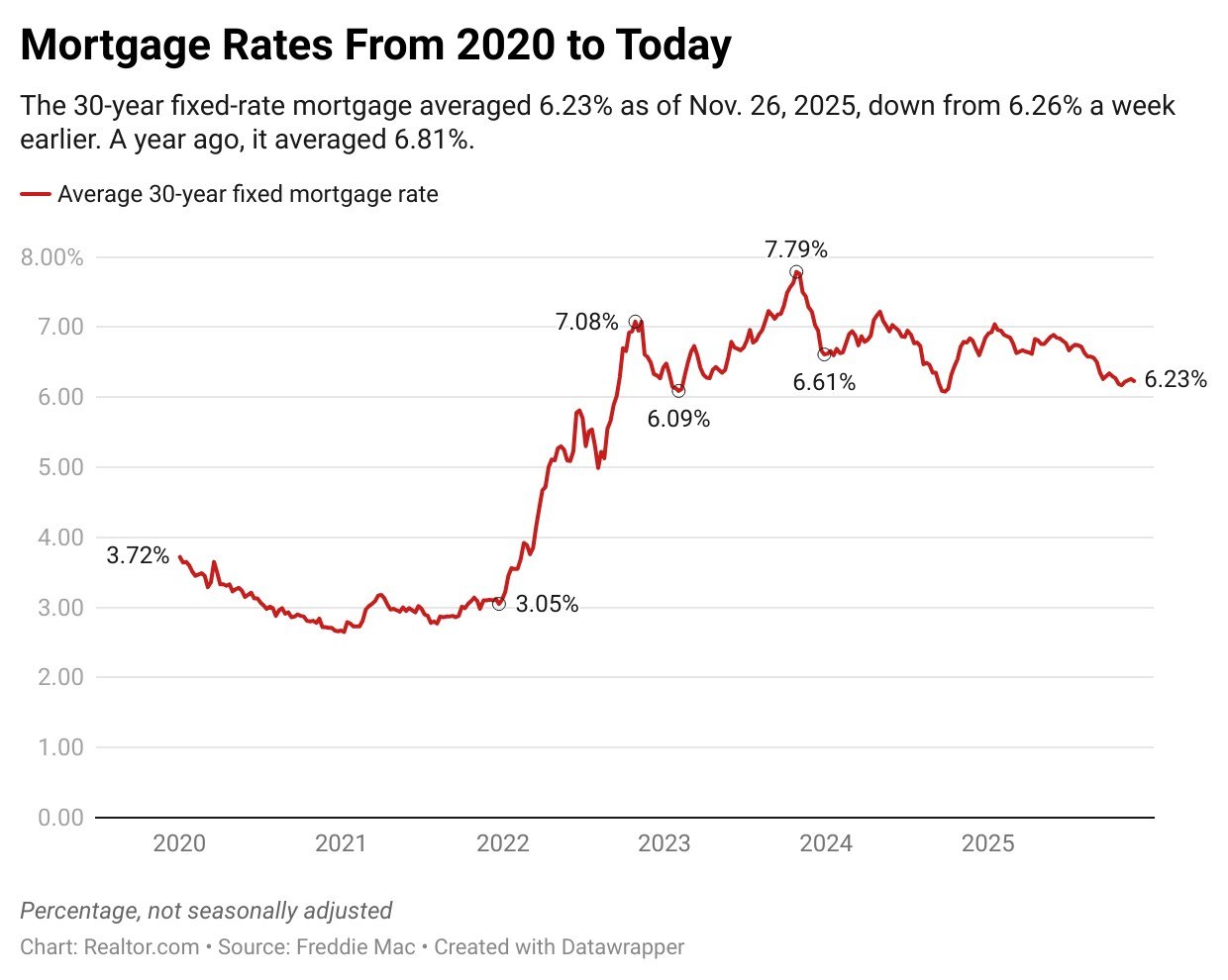

The average interest rate on 30-year home loans fell to 6.23% for the week ending Nov. 26, compared to 6.26% the week before, according Freddie Mac. During the same period in 2024, rates averaged 6.81%.

“Heading into Thanksgiving, mortgage rates fell,” says Sam Khaterthe chief economist of Freddie Mac. “With home sales at their highest level since last November, homebuyer activity continues to show resilience as we approach the end of the year.”

The slight easing comes after 10-year U.S. Treasury yields, which closely track mortgage rates, fell to nearly 4% this week.

After September’s stalled jobs report sent mixed signals, several key Fed officials, including the New York Fed president, stepped up John Williamshinted that they would vote for another rate cut at the next meeting of the Federal Open Market Committee (FOMC), despite some likely dissent from fellow policymakers.

Chairman of the Boston Fed Susan Collins and Fed President of St. Louis Jeff Schmid both telegraphed their intention to oppose this year’s third rate cut, citing inflation concerns.

The FOMC will vote on interest rate policy on December 10, but key employment and inflation reports are not expected to be released on time, leaving policymakers to make decisions based on partial and outdated indicators.

A further quarter-point cut in the Fed’s federal funds rate which traders believe will happen with an 80% probabilitywould likely push mortgage rates to annual lows just as 2025 comes to a close.

“This would give homebuyers something to be thankful for heading into 2026, while potentially boosting a housing market that has seen some light tailwinds of late,” he said. Realtor.com® senior economist Jake Krimmelciting a 1.9% increase in pending home sales in October and four consecutive months of annual growth in existing home sales.

Even more good news for home buyers is that builders have started offering more competitive pricing and financing.

“After Thanksgiving, as the fall home buying season comes to an end, all eyes will be back on the Fed and the slow trickle of backlogged government data,” Krimmel notes. “Much of where the mortgage and housing markets go depends on inflation and the labor market outlook.”

The economist predicts that if inflation cools, the labor market recovers and the Fed cuts again, the housing market could enter the new year with “real momentum.”

How mortgage interest is calculated

Mortgage interest rates are determined by a delicate calculation that takes into account the state of the economy and an individual’s financial health. They are most closely tied to 10-year Treasury yields, which reflect broader market trends such as economic growth and inflation expectations. Lenders refer to this benchmark before adding their own margin to cover operating costs, risks and profits.

When the economy shows warning signs of rising inflation, government bond yields typically rise, causing mortgage rates to rise. Conversely, signs of falling inflation or weakness in the labor market typically cause government bond yields to fall, causing mortgage rates to fall.

However, the mortgage rate offered to you by a lender goes beyond these benchmarks and takes into account some of your personal factors.

Your lender will closely monitor your financial health, including your credit score, loan amount, property type, down payment size, and loan term, to determine your risk. Those with a stronger financial profile are considered lower risk and typically receive lower interest rates, while higher-risk borrowers receive higher rates.

How your credit score affects your mortgage

Your credit score plays a role when applying for a mortgage. A credit score determines whether you qualify for a mortgage and what interest rate you receive. The higher the credit score, the lower the interest rate you qualify for.

The credit score you need depends on the type of loan. A score of 620 is a “fair” grade. However, people applying for a Federal Housing Administration loan may be able to get approved with a credit score of 500, which is considered a low score.

Homebuyers with a credit score of 740 or higher are generally considered to be in very good standing and can usually qualify for better rates.

Different types of mortgage loan programs have their own minimum credit score requirements. Some lenders apply stricter criteria when assessing whether they approve a loan. They want to be sure that you can repay the loan.