How to Pay In-Home Senior Care Staff: Ultimate Guide

Paying senior caregivers isn’t the same as paying contractors or a household staff assigned by an agency. If you hire directly and control the schedule and duties, you’re considered a household employer under IRS rules. That means wages and household employment taxes may apply.

This guide explains how to pay in-home senior care staff legally and sustainably, so your payroll process works week after week without creating compliance problems at tax time. I’ll also walk you through how to structure pay, so it follows overtime rules.

If you don’t want to manage payroll yourself, a service like Poppins Payroll can handle pay runs, tax payments, and year-end filings for you. It even has a team of experts you can contact for questions on tax account setup and payroll reporting.

Are in-home caregivers considered household employees?

If you hire a caregiver directly and control what work is done and how it’s done, the IRS treats that worker as your household employee.

In practical terms, that includes situations where you:

- Set the caregiver’s schedule

- Assign daily duties

- Direct how care is provided

- Supervise performance

When those conditions exist, you’re considered a household employer. This means you’re responsible for household employee payroll, including tracking wages and determining whether payroll taxes for caregivers apply once federal thresholds are met. As an employer, you also need a federal employer identification number (EIN) and set up state accounts (if applicable) to remain compliant.

However, if you hire through an agency, that company is the employer of record. So, it handles payroll instead and is considered the caregiver’s employer.

Still in the hiring phase and unsure whether agency vs private hire is best for you? Read our hiring an in-home caregiver guide, which compares both options and walks you through the next steps depending on what you choose.

When paying in-home senior care staff, classification is not optional, as it determines whether you issue a W-2 or a 1099 and whether household employment taxes apply.

Under IRS rules, a caregiver you directly hired is your household employee if you control what and how work is done in your home. Misclassifying workers can result in back taxes, penalties, and interest charges. It can also prevent the caregiver’s wages from being properly reported to the Social Security Administration, which affects how their retirement and Medicare benefits are calculated later.

Some household employment tax rules do not apply when you directly hire and pay certain close family members as in-home caregivers. According to IRS Publication 926, wages paid to your spouse, your child under age 21, and your parent may be exempt from Social Security, Medicare, or federal unemployment taxes depending on the situation.

On the other hand, wages paid to other relatives, such as siblings, adult children over 21, nieces, or nephews, are subject to the same household employment tax rules as any other employee. Because family relationships affect tax treatment, you should review IRS guidance carefully before assuming an exemption applies.

If you’re not sure how classification or exemptions apply to your situation, a household payroll service like Poppins Payroll can help ensure wages are reported correctly and required taxes are handled in line with current IRS rules.

Setting fair compensation rates

Once you’ve confirmed the caregiver is your household employee, the next concern is compensation. Pay must be competitive enough to attract qualified help while also complying with minimum wage and overtime laws.

Based on the most recent national data from the Bureau of Labor Statistics (BLS), the median hourly wage for home health and personal care aides is $16.78 (as of May 2024). That number provides a national midpoint, but it is not necessarily what you should offer. In many metro areas, posted caregiver rates exceed $20 per hour due to labor shortages and higher living costs.

For example, in Colorado, the average posted hourly rate is $24.93, while in Louisiana, it’s $17.09 per hour, according to Care.com’s state posted-rate table. States with higher costs of living, like California, New York, and Massachusetts, typically see rates between $20–$30 per hour for experienced caregivers with certifications.

When determining compensation, I focus on four variables:

- Type of care required: Light housekeeping and companionship commands lower rates than hands-on personal care like bathing, dressing, and mobility assistance. If your loved one has complex medical needs, cognitive impairment, or behavioral challenges, expect to pay at the higher end of the range.

- Experience and credentials: Caregivers with Certified Nursing Assistant (CNA) certification or dementia training typically expect higher wages than entry-level aides. If your loved one needs medication management, wound care, or other medical tasks, you’ll need someone with the appropriate qualifications—and the wages reflect that expertise.

- Live-in vs hourly structure: Live-in caregivers are sometimes paid flat daily or weekly rates rather than hourly wages. Even with flat pay, you must track hours worked and ensure wage laws are satisfied. You also have to consider how overtime and sleep time apply, which depends on federal and state rules.

- Total cost planning: The worker’s hourly rate is not your full payroll cost. As a household employer, your total expense may include employer payroll taxes and other compliance-related costs once wage thresholds are met. That means budgeting slightly above the agreed hourly wage so you’re not surprised later.

I also recommend checking local job postings and using online cost calculators to establish a competitive baseline. Remember, offering fair compensation isn’t just about following labor rules and payroll compliance. It’s attracting reliable, quality caregivers who’ll provide excellent care for your loved one.

Caregiver overtime rules & overnight pay

Overtime rules are one of the most misunderstood parts of paying in-home senior care staff. Getting this wrong can expose you to back pay claims, penalties, and strained working relationships.

Under the Fair Labor Standards Act (FLSA), most household employees must be paid at least the applicable minimum wage and overtime pay at one and one-half times their regular rate for hours worked over 40 in a defined workweek.

Before you calculate anything, define your workweek. A workweek is a fixed, recurring seven-day period (for example, Monday through Sunday). Overtime is calculated within that period.

Overtime: Live-out vs live-in caregivers

Caregiver overtime rules depend on whether or not the worker resides in your home.

Live-out caregivers: If your caregiver doesn’t live in your home, federal overtime rules apply once they exceed 40 hours in a workweek. Let’s say you pay your senior care staff $22 per hour and they work 50 hours a week. So that’s 40 regular work hours and 10 hours of overtime for the workweek.

The pay computation will be:

(Regular rate × regular work hours) + ((regular rate × 1.5) × overtime hours) = Total gross pay

Or

($22 × 40 regular work hours) + (($22 × 1.5) × 10 overtime hours) = $1,210

Note that some states have stricter requirements. Always confirm your state’s labor standards in addition to federal law.

Live-in caregivers: If the caregiver permanently resides in your home or stays for extended periods (typically five or more days per week), the FLSA provides an overtime exemption for live-in domestic service employees at the federal level. However, many states don’t follow the federal exemption.

States with their own overtime requirements for live-in caregivers include California, Hawaii, Massachusetts, Maryland, Maine, Minnesota, New Jersey, Nevada, New York, and Oregon. In these states, live-in caregivers may be entitled to overtime after working more than 40 hours per week, or in some cases, after working a certain number of hours per day or week based on state-specific thresholds.

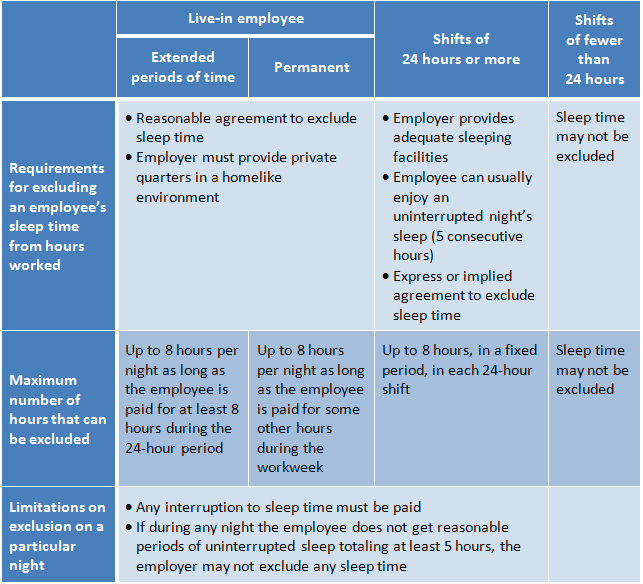

Overnight shifts and sleep time

If your caregiver lives in and works a 24-hour shift, you can exclude up to eight hours of sleep time from compensable hours. However, this only applies if the caregiver gets at least five hours of uninterrupted sleep and has adequate sleeping facilities. If the worker is regularly interrupted to provide care services during those hours, the sleep time is compensable.

Paying senior caregivers for sleep time depends on employment status and shift length. Factors include living on site and whether the shift is 24 hours or longer, or shorter than 24 hours. For a quick guide on which sleep rules apply, check out the table below:

When tracking caregiver hours, precision matters. I recommend using a time-tracking system. It can be a simple app, a paper timesheet, or a feature within your payroll service.

Poppins Payroll, for example, tracks hours and calculates overtime automatically based on your state’s rules, which removes the guesswork and reduces errors. To learn more about its services, visit the Poppins Payroll website.

Tip: In addition to checking state and federal overtime rules for live-in caregivers, prepare a clear written agreement that includes on-duty and off-duty hours, minimum wage, and applicable overtime rates. It should also clarify how interruptions to sleep will be recorded and the accommodations provided (e.g., meals, private bedroom).

Workers’ compensation for caregivers

Caregiving is physical work. Transfers, mobility assistance, fall prevention, and repetitive tasks all carry injury risk. If a caregiver is injured while working in your home, you may be responsible for medical costs and lost wages.

Workers’ compensation insurance covers work-related injuries and illnesses. In many states, household employers are required to carry workers’ comp coverage for domestic employees once certain wage or hour thresholds are met. Even where coverage is not mandatory, it’s a good idea to get one as it significantly reduces personal liability exposure.

Without workers’ comp coverage, if your caregiver slips on your stairs, injures their back while helping your parent transfer from a wheelchair, or develops carpal tunnel from repetitive tasks, you could be personally liable for their medical bills and lost wages. A single workplace injury claim could easily reach tens of thousands of dollars.

It’s also important not to assume that your homeowners’ insurance covers workplace injuries involving household employees. It often doesn’t, except in California and New Jersey, where you can add an endorsement. Even then, that coverage is limited and doesn’t provide the same protections as a standalone workers’ comp policy.

Tip: To ensure compliance with varying state rules, I advise utilizing a payroll service that offers access to workers’ compensation plans. Poppins Payroll, for instance, collaborates with Bhalu Insurance, which specializes in workers’ compensation coverage for household employers and manages the processes for quoting, enrollment, and renewals.

Payroll taxes for caregivers

This is where paying senior caregivers legally can get confusing. Once wages reach certain thresholds, federal household employment taxes apply.

Here’s how that breaks down:

FUTA applies if you pay $1,000 or more in cash wages in any calendar quarter to household employees. This is 6% on the first $7,000 of wages per employee, per year. FUTA is not withheld from the caregiver’s wages. It is paid entirely by you.

Most employers qualify for a 5.4% credit for paying state unemployment taxes, bringing the effective FUTA rate down to 0.6%. However, if you’re in a “credit reduction state” (one that hasn’t repaid federal unemployment loans), your FUTA credit may be reduced, increasing your effective rate.

Depending on where you live, you might also owe state unemployment insurance, state disability insurance, or local payroll taxes. California, New York, New Jersey, and several other states have their own unique requirements that can catch families off guard, so ensure you check state and local rules before processing in-home senior care payroll.

Income tax withholding is optional for household employers, meaning you’re not required to withhold it. However, many caregivers prefer having taxes withheld throughout the year rather than facing a big tax bill in April. If your caregiver requests withholding, they’ll need to complete Form W-4, and you’ll have to calculate the withholding amount based on their elections.

How payroll services simplify tax compliance

For many families, handling pay calculations and tax reporting feels overwhelming. Some may manage in-home senior care payroll themselves using spreadsheets, only to discover they’ve underpaid taxes or missed a filing deadline. If you’re not comfortable with payroll tax calculations and deadlines, professional help is a smart investment.

This is where household payroll services like Poppins Payroll become valuable. For $49 per month, Poppins Payroll will handle EIN registration, tax calculations, quarterly filings, W-2 preparation, and Schedule H at year-end. It also monitors changing thresholds, ensures you’re compliant with state-specific requirements, and gives you direct deposit capabilities so you’re not cutting paper checks every week.

Required tax forms for household employers

Once payroll taxes apply, paying in-home senior care staff legally requires specific federal reporting forms. Household employers use a different reporting structure than traditional businesses, so it’s important to understand which forms apply to you.

Step-by-Step: How to pay in-home senior care staff

Once your federal EIN, tax accounts, and payroll process are set up, paying in-home senior care staff becomes a repeatable cycle. The key is consistency and accurate recordkeeping.

Here’s what the process looks like:

Step 1: Collect and review hours worked

At the end of each pay period, review the caregiver’s recorded hours. Confirm the total hours for regular work, overtime tasks, and overnight interruptions (if any).

If you’re not using a payroll service with a time tracker, consider using a time tracking system for your in-home senior care staff. Check out our guide to the best free time tracking software for options.

Step 2: Calculate gross pay

Multiply regular hours by the agreed hourly rate and apply overtime where required.

If you and your caregiver agree on a flat daily or weekly rate, you must still track hours worked. Divide total pay by total hours to confirm the caregiver’s average hourly rate meets at least minimum wage. If the caregiver works more than 40 hours in a workweek and overtime applies, you must calculate overtime pay separately, even if you started with a flat rate.

For example:

If you pay $1,200 for a week and the caregiver works 60 hours, the effective hourly rate is $20 (or $1,200 ÷ 60 hours). If overtime rules apply after 40 hours, you would owe 40 hours at $20 and 20 hours at $30 (or 1.5 × $20), for a total of $1,400. A flat $1,200 payment would fall short.

Step 3: Apply required withholdings

If wage thresholds have been met, withhold Social Security and Medicare taxes, including federal and state income taxes (if agreed upon). Separately account for your household employer tax obligations. Remember: do not deduct employer taxes from caregiver wages.

Step 4: Issue net pay

Depending on what you agreed with the caregiver, issue employee payments via check, cash, or direct deposit. You should also provide a pay slip showing gross wages, taxes withheld, net pay, and any deductions.

Step 5: Set aside employer taxes

Each pay period, set aside your employer portion of taxes so you’re prepared for quarterly or annual payments. Many household employers underestimate this step. Planning ahead prevents cash flow strain at tax payment time.

Step 6: Maintain payroll records

Keep copies of timesheets, pay summaries, tax calculations, payroll tax payment reports, and year-end filing reports. The IRS recommends maintaining employment tax records for at least four years. Keeping consistent records protects you in the event of a dispute or payroll audit.

Tax payments & year-end reporting

Paying in-home senior care staff is not just about calculating wages. It also involves paying and reporting taxes throughout the year.

Quarterly estimated tax payments

Rather than waiting until year-end to pay all your household employment taxes at once, you can make quarterly estimated payments using Form 1040-ES. This means calculating your expected annual tax liability (FICA taxes plus FUTA), dividing it by four, and making payments by April 15, June 15, September 15, and January 15.

Alternatively, if you’re employed and have income tax withheld from your own paycheck, you can increase your withholding to cover your household employment taxes throughout the year. This approach avoids the hassle of making separate quarterly payments. Just submit a new Form W-4 to your employer requesting additional withholding, and your household employment taxes get paid automatically through your regular paycheck.

Year-end reporting

At the end of the year, you must report total wages paid and reconcile household employment taxes. The key federal forms and deadlines are summarized below.

In addition to federal filings, many states require year-end reconciliation for unemployment or income tax withholding. Requirements and deadlines vary by state. Before filing, confirm that total wages, taxes withheld, and any estimated payments align with your payroll records.

Frequently asked questions (FAQs)

No. According to the IRS, if you control what work is done, when it’s done, and how it’s done—which is virtually always the case with in-home caregivers—they’re your household employee. You must also issue a W-2, not a 1099. Misclassification leads to back taxes, penalties, and denied Social Security credits for your caregiver.

Caregivers with part-time schedules can still trigger taxes. Whether you owe FICA taxes really depends on whether the annual wages reach a certain minimum amount.

Yes. You can choose your payment method, but wage and tax obligations still apply.

Yes, it is. Managing in-home senior care payroll requires tracking hours, calculating taxes, and meeting reporting deadlines. Services like Poppins Payroll can simplify and streamline tax computations, filings, and W-2 preparation, reducing administrative risk.

Yes. Household employee payroll providers like Poppins Payroll can help you catch up on back taxes and get current. However, you’ll likely need to pay additional fees for amended filings and back-period reporting. The sooner you get compliant, the less you’ll owe in penalties and interest. It’s always better to correct the situation voluntarily rather than waiting for the IRS to discover unreported employment.

Source link

According to IRS Publication 926, if you pay a household employee $3,000 or more in cash wages

This threshold can change from year to year. Check the IRS website for updates.

in 2026, you must withhold and pay Federal Insurance Contributions Act (FICA) taxes—that’s Social Security and Medicare combined.

FICA taxes total 15.3% of wages. You’re responsible for half (7.65%), and your caregiver pays the other half (7.65%) through withholding. The 7.65% split consists of:

This limit can change from year to year. Check the SSA website for updates.

If a caregiver earns over $200,000 in a year, an Additional Medicare tax of 0.9% applies. Although this is uncommon in household employment situations, you must withhold this from the employee’s salary. Unlike the regular Medicare tax, there’s no employer match for this.