Can Capital Gains Tax Cuts Lower House Prices? There are two proposals on the table

The housing market is stuck, and not only because of high mortgage rates and affordability. In many metro areas, old homeowners with large profits are delaying sales to avoid high capital gains taxes, keeping potential listings off the market.

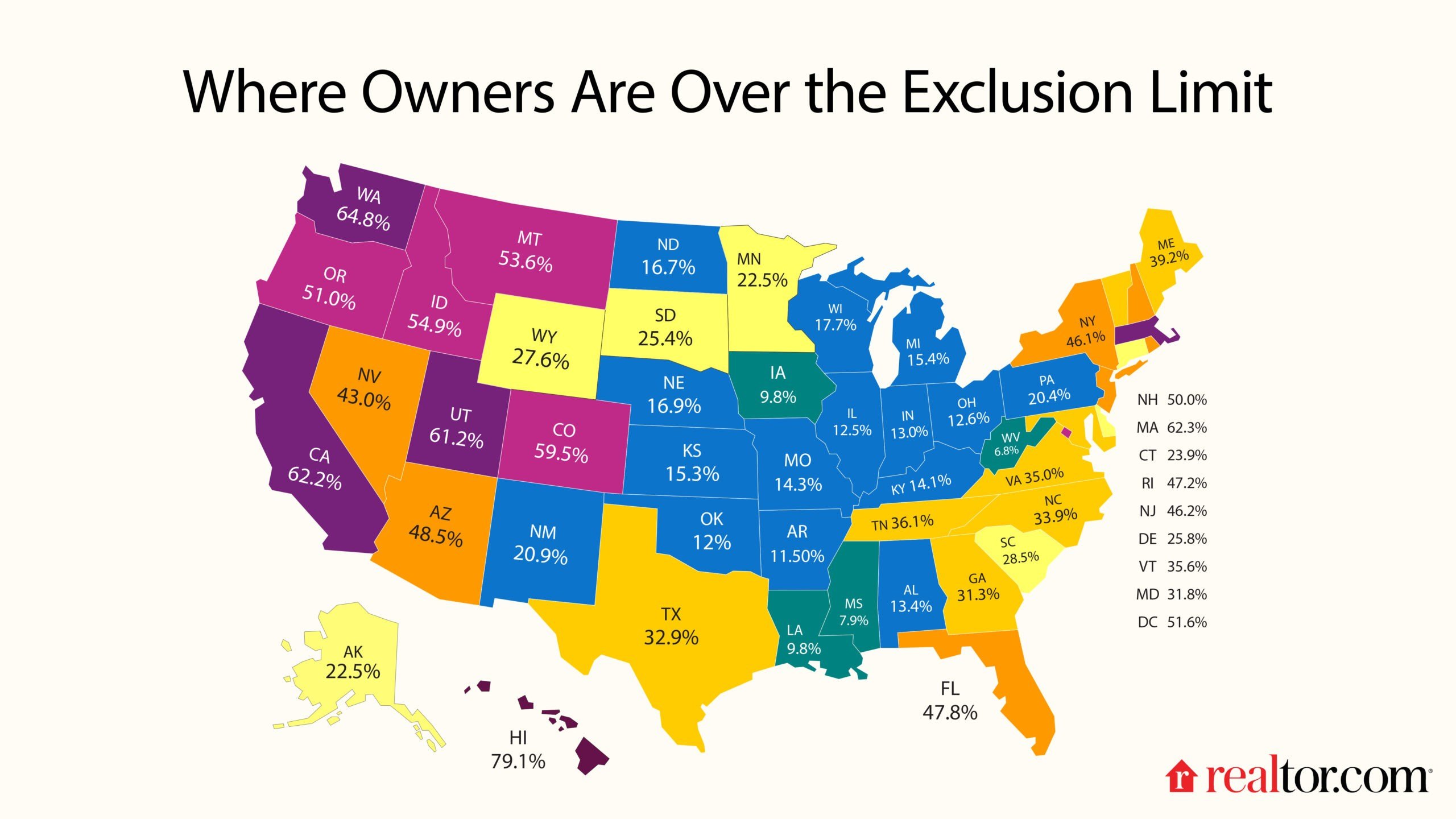

That dynamic has put capital gains back on the table in Washington, D.C., where lawmakers are weighing reforms against the federal exclusion from primary home sales. It currently stands at $250,000 for single filers and $500,000 for married couples filing jointly – a threshold that has not changed since 1997 even as house prices have risen by more than 260%.

The result is a growing group of homeowners who cannot sell without receiving a tax bill. Nearly 29 million households (about 34% of U.S. homeowners) may already exceed the single-file exclusion limit, exposing them to a hidden home equity tax liability if they move. By 2030, that share is expected to reach 56%, turning what was once a niche tax problem into a widespread drag on housing mobility and, by extension, supply.

The National Association of Realtors® states that the effect is already visible on the resale market.

“Based on our best information and insights, there would be a significant increase in the number of homes coming up for sale. [if the capital gains tax was reformed]but it would vary quite a bit between local markets,” says Evan Liddiard, NAR’s director of federal taxes, citing studies the group commissioned.

And the sellers most likely to respond may not look like “luxury” on paper. In many high appreciation markets, a $1 million home is no longer a mansion, but a starter benchmark. That has created an emerging class of “accidental luxury” owners: people who bought ordinary homes decades ago and are now sitting on a windfall they never expected, and a tax bill they never knew they would get in trouble for.

The open question is whether policies that unlock deals can also lower prices. Research shows that it can reduce the lock-in effect and increase sales. Whether that’s enough to shift prices – or ease the broader affordability crisis – is a more difficult question.

What is proposed

There are currently two proposals driving the capital gains debate in Washington.

The first is a account from Rep. Marjorie Taylor Greene (R-Georgia) that would completely eliminate the capital gains tax on the sale of first homes.

“I just think this is a great gift to the American people, and it’s the core of what we were founded on,” Greene told Realtor.com® in an exclusive interview in July.

While chairman Donald Trump expressed support for the measure, the future of the proposal has become unclear after the congresswoman announced she will leave Congress at the end of this year. That has the more focused More homes on the marketfrom Rep. Jimmy Panetta (D-California) takes center stage again.

Panetta’s bill would increase the federal capital gains exclusion on primary home sales and then index it to inflation so that the threshold moves with the housing market instead of remaining frozen for decades.

It is an elegant solution for a threshold that has been missing since 1997, when… the median home price was $145,000and Netscape America’s favorite web browser.

While Greene’s approach is blunter, Panetta’s would still have a significant impact, roughly doubling the current exemption to $500,000 for individuals and $1 million for couples, restoring the law’s original intent to protect, not penalize, ordinary homeowners.

The rise of ‘accidental luxury’ homeowners

To understand how changing the capital gains exclusion could affect home prices, it’s worth considering a growing class: casual luxury home owners. These are ordinary people who bought what was then an ordinary house. But because of market dynamics beyond their control, they are now enjoying windfalls.

“When the exclusion came into effect in 1997, it largely created real windfalls on unusually well-performing properties,” he explains. Anthony Smithsenior economist at Realtor.com®. “Today, many homes that are ‘normal’ for their market, especially long-lived primary homes, exceed the foreclosure simply because of price appreciation, and not because of speculative benefits.”

This dynamic is especially visible in the ‘metropolitan luxury’ metros, where seven figures have become a baseline rather than an outlier. That includes coastal California, along with Sun Belt boom markets like Austin, Texas; Nashville, TN; Phoenix; and parts of Florida.

In the Seattle-Tacoma metro area, for example, 596 homes currently for sale were purchased before 2010 for less than $1 million and are now on the market for $1 million or more, Smith says, “illustrating how long-term appreciation has pushed many longtime homeowners toward a million-dollar home.”

It’s a perfect illustration of the policy bottleneck: As more “normal” homes exceed the limit, more owners have a reason to hold back, shrinking the resale supply that would otherwise help drive down prices.

Why home equity taxes create a ‘lock-in’ effect

Just think of my parents. They bought their Phoenix home in 1989 for just under $64,000, long before the metro’s growth and demand surged.

Over the decades, their income has generally been in the lower end of the middle-income category, as defined by Pew research– not the profile most people associate with a large capital gains tax.

But if they had sold at the top of the recent market, when their modest two-bedroom ranch-style home was valued at more than $700,000, a significant portion of that appreciation would have become taxable. Even taking into account the federal exclusion for married couples and the capital improvements they made, they would have been looking at tax liability on about $200,000 worth of hard-earned stock.

For long-tenured owners like those trying to move, that tax calculation could become a reason to opt out, and that friction is already showing up in the data.

Older households have become much less likely to move than in previous decades, with mobility among the over-65s falling from 10% in the 1970s to around 3% in 2023, according to research by the Federal Reserve Bank of Richmond. It’s a steep drop that shows how many seniors are sheltering in place alone.

What the Taxpayer Relief Act of 1997 teaches us about seller behavior

For those skeptical that simple tax reform could lead to more homes on the market and lower home prices, it helps to look at the last time capital gains taxes were reformed.

The Taxpayer Relief Act of 1997 replaced the one-time capital gains exclusion for homeowners over age 55 with the current thresholds.

The shift was not radical, but it did produce results: Researchers found that reducing tax friction encouraged more people to sell, especially those near the new exemption threshold.

Around the same time, the repeal of the age-based exclusion also boosted mobility. Households in their early 50s, mostly empty nesters or downsizing after divorce, were significantly more likely to move. another analysis. Mobility increased between 22% and 31% among target groups.

The people who moved weren’t random either. They often found themselves in high valuation markets, where they faced a higher expected tax bill if they stayed put, and were ready to trade down.

In other words, they were a lot like the current owners of overheated metropolises with long track records, people sitting on big profits and wondering whether now is the right time to sell.

Would this actually lower house prices?

Even a modest shift in supply can quickly change price behavior. Better yet, the price impact would likely not resemble a dramatic national collapse. Instead, it would be reflected in what buyers actually feel: more bargaining power, fewer bidding wars, and more offers that last long enough to trigger price cuts.

In this way, capital gains tax reform could be the key to lowering home prices for buyers.

“The country as a whole has a significant and growing problem with inventories being held back by older, long-term homeowners who are not selling at historic rates due to the fact that they would have to pay significant capital gains taxes on the profits from the sale of their homes,” Liddiard said.

He points to a break in the typical housing cycle, with many vacant residents or owners nearing or reaching retirement downsizing at unusually low rates.

“Many older homeowners know that if they keep their property until they die, they can pass it on to their heirs tax-free, so this is leading to many not wanting to sell,” he says. “Others are not happy about the prospect of handing over their long and hard-earned wealth to Uncle Sam when they need it to pay for their next home.”

When you remove that friction, the market starts to clear. Buyers no longer have to bid as if it were an auction, sellers lose influence, market days rise and price cuts become more common. This creates downward pressure on prices – not from a single shock, but from a shift in bargaining dynamics as choice returns.

None of this means that capital gains reform would fix the housing market on itself. But it could provide an immediate mechanism for relief.