A Simple Explanation of Section 1231 Property & Its Taxation

Editor’s Note: This article focuses on the big-picture 1231 issues. It excludes details and exceptions that rarely make a difference and only serve to overly complicate things. It is intended for small business owners trying to understand how the tax is calculated on their asset sales, so if you’re a tax pro researching the nuances of 1231 or studying for an exam, this article might not be for you.

Section 1231 property refers to physical assets used in a business for more than one year. These are long-term working assets, such as office buildings, land, office furniture, manufacturing equipment, and long-term rental property, including buildings and rental furnishings. It does not include investment assets or inventory held for sale.

This classification matters because Section 1231 assets receive special tax treatment when sold. All Section 1231 sales for the year are combined and netted together. If the result is a net gain, it is generally taxed at capital gain rates. If the result is a net loss, it is treated as an ordinary loss, which can reduce ordinary income.

Later, a detailed example will show how part of a Section 1231 gain may be taxed at a lower rate than regular income.

Key takeaways:

- Section 1231 property falls into three buckets: 1245 (depreciable assets like equipment), 1250 (buildings), and “other 1231” (land).

- The same item can be classified differently depending on how it’s used (business use vs personal use vs inventory for resale).

- For gains, land usually flows straight into the “1231 bucket,” but equipment and buildings require splitting out the depreciation-related portion first.

- Section 1245 gains can turn into ordinary income through depreciation recapture, while Section 1250 gains can include “unrecaptured 1250 gain” that may be taxed at up to 25%.

- You don’t decide capital vs ordinary transaction-by-transaction. Everything gets netted in the 1231 bucket, and prior five-year nonrecaptured 1231 losses can force later gains to be taxed as ordinary (1231 recapture).

Categories of Section 1231 property

Section 1231 property can be broken into three main subcategories. While they all fall under Section 1231, the tax rules treat them slightly differently once depreciation enters the picture.

- Depreciable assets other than buildings: Furniture, equipment, machinery, vehicles, and similar business assets fall into this group. These are still Section 1231 assets, but they are more specifically classified as Section 1245 property.

- Buildings: Business buildings also qualify as Section 1231 property. However, they are further classified as Section 1250 property for tax purposes.

- Land: Land is the third major type of Section 1231 property. Unlike equipment or buildings, it does not have a separate code section label. For simplicity, it can be referred to as “other Section 1231 property.”

Breaking Section 1231 property into 1245 property, 1250 property, and other 1231 property becomes important when calculating tax on a sale. The reason is simple: not all gains are treated the same.

Think of it like sorting laundry before washing. Even though everything came from the same closet, whites, colors, and delicates go through different cycles. In the same way, business assets may all fall under Section 1231, but the tax rules run them through different “cycles” when sold.

For example, with Section 1245 property, part of the gain may not qualify as Section 1231 gain at all. The portion tied to accumulated depreciation is pulled out and taxed as ordinary income instead. That detail can change the final tax result, which is why the categories matter. The taxation section will walk through this more carefully.

Take a car as an example:

- If a business uses the car to shuttle employees, it is used in normal operations and treated as Section 1231 property.

- If someone buys the car for personal use or to hold as an investment, it is treated as a capital asset.

- If a dealer buys the car to resell it quickly, it is inventory.

The object does not change. The purpose does. And in tax law, purpose drives classification.

Taxation of Section 1231 property

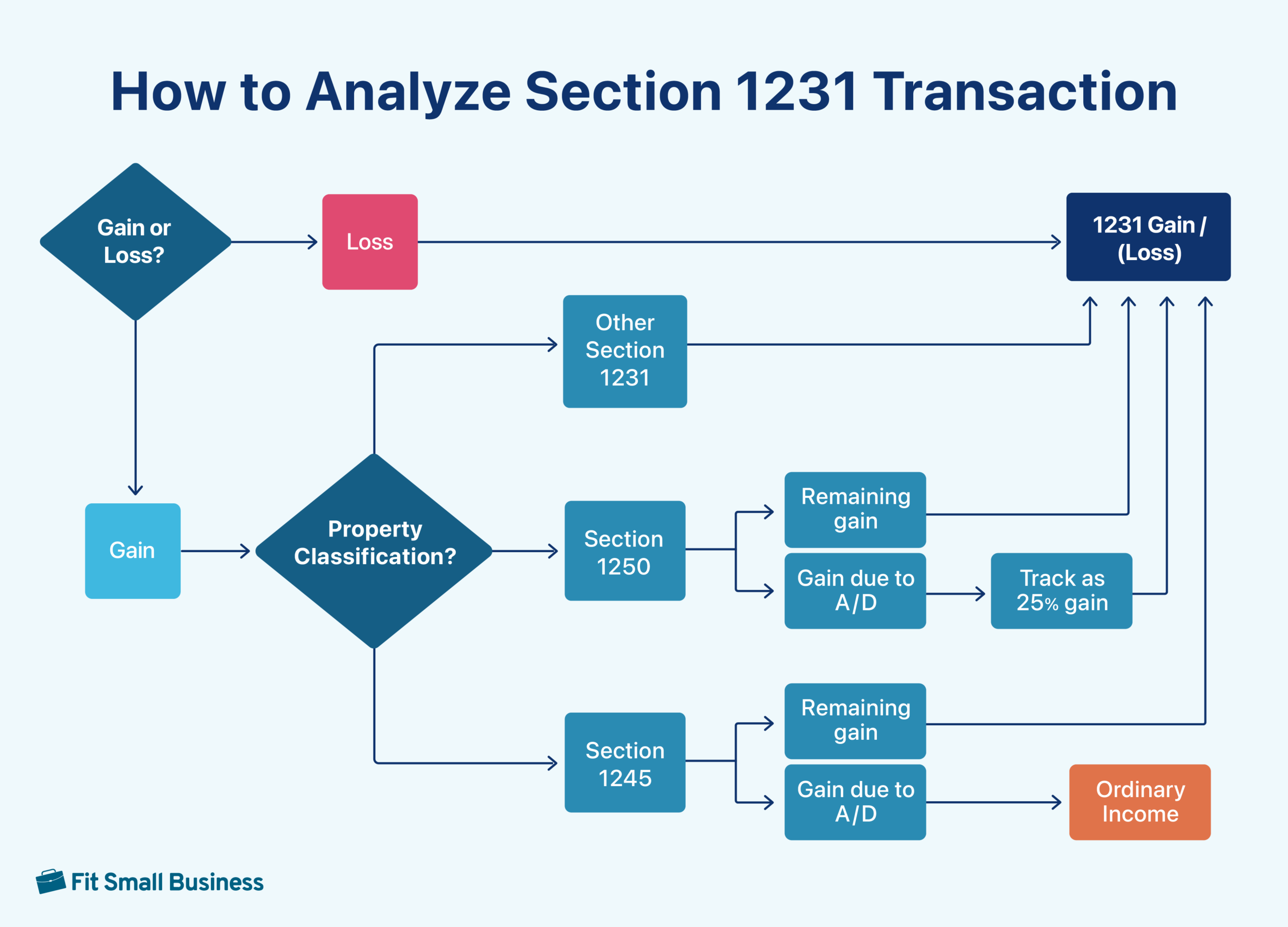

Analyze each 1231 transaction

Start by checking whether the sale created a gain or a loss. If it is a loss, it generally goes straight into the Section 1231 total for the year.

If it is a gain, the next step is to identify what type of property was sold. Land and similar “other” Section 1231 property usually sends the gain straight into the Section 1231 total. Buildings and equipment take an extra step because depreciation changes how the gain is taxed.

The part of the gain tied to prior depreciation is separated out first. For equipment (Section 1245), that depreciation-related portion is taxed as ordinary income. For buildings (Section 1250), that depreciation-related portion is tracked separately and may be taxed at a special 25% rate. After that split, whatever gain is left goes into the Section 1231 total.

To illustrate how Section 1231 disposals are analyzed, assume several business assets were sold during the year. All of the assets were owned for more than one year and used in the business.

Land #2, the equipment, and the maintenance shop were sold at a loss. Losses are automatically treated as Section 1231 losses, so they can be added directly to the Section 1231 “bucket” without further analysis.

After reviewing all transactions, the final step is to look at the overall result of the Section 1231 bucket. If the total is a net gain, it is treated as a capital gain. If the total is a net loss, it is treated as an ordinary loss.

Analyze section 1245 gains

Section 1245 property includes depreciable items like machinery, equipment, and furniture used in a business. These are the working tools of the business that lose value over time through depreciation.

When one of these assets is sold at a gain, that gain does not stay in one piece. It has to be split into two parts.

- The first part is the true increase in value, meaning the amount received above the original cost. That portion is treated as Section 1231 gain and goes into the Section 1231 bucket.

- The second part of the gain exists because depreciation was previously claimed. Over the years, depreciation reduced the asset’s basis. When the asset is sold, the IRS “recaptures” that benefit. This portion is called Section 1245 recapture, and it is taxed as ordinary income. It does not go into the Section 1231 bucket.

Let’s analyze the two 1245 assets that were sold at a gain to separate that gain into the 1231 gain and the ordinary income.

- Machinery: The machinery originally cost $45,000 and was fully depreciated, meaning its accumulated depreciation was also $45,000. It was sold for $15,000, which is less than its original cost but more than its adjusted basis of zero. Because the entire gain comes from prior depreciation, the full $15,000 is treated as ordinary income. This is what tax professionals call Section 1245 recapture. None of the gain is treated as Section 1231 gain.

- Furniture: The furniture was purchased for $10,000 and fully depreciated. It was later sold for $12,000, which is $2,000 more than its original cost. The total gain is $12,000. Of that amount, $10,000 is due to prior depreciation and is treated as ordinary income under Section 1245 recapture. The remaining $2,000 represents the amount received above the original cost, and that portion is treated as a Section 1231 gain.

Analyze Section 1250 gains

Section 1250 property refers to depreciable buildings used in a business. When a building is sold at a gain, the gain does not stay as one lump amount. It must be separated based on what caused the gain.

- Any amount received above the original purchase price is treated as a regular Section 1231 gain and added to the Section 1231 bucket.

- The portion of the gain tied to accumulated depreciation is also treated as a Section 1231 gain, but it is tracked separately. This amount is called unrecaptured Section 1250 gain. It still flows into the Section 1231 buck

Let’s analyze the Warehouse in our example, which is the only 1250 asset sold at a gain.

The warehouse was purchased for $500,000 and later sold for $575,000. The selling price is $75,000 higher than the original cost, so that $75,000 is treated as a regular Section 1231 gain.

An additional $150,000 of the total gain comes from accumulated depreciation that reduced the building’s basis over time. This portion is also treated as Section 1231 gain, but it is classified as unrecaptured Section 1250 gain and may be taxed at a maximum rate of 25%.

Compile your gains and losses

Now that each transaction has been analyzed, you can compile your gains and losses. Any amounts from Section 1245 property treated as ordinary income should be reported as ordinary income on Form 4797. All other gains and losses get included in our 1231 bucket.

Let’s separate our total gains and losses from the asset disposals into what gets 1) reported as ordinary income on Form 4797; and 2) included in our 1231 bucket.

The total gain is still $247,000, just like in the original example. That number did not change. What changed is how the gain is classified. After reviewing each sale, it becomes clear that $25,000 of the total gain is not Section 1231 gain. That amount must be reported as ordinary income on Form 4797. It also becomes clear that $150,000 of the Section 1231 gain falls into a special category. That portion may be taxed at a maximum capital gains rate of 25% instead of the typical 20%.

Calculate the tax on 1231 gains

All Section 1231 gains and losses are combined into one total, often called the “1231 bucket.” The tax treatment depends on whether that final number is positive or negative.

- If the bucket is negative, the entire amount is treated as an ordinary loss and reported on Form 4797.

- If the bucket is positive, the entire amount is treated as a capital gain.

A common mistake is to treat each gain as capital and each loss as ordinary. That is not how the rule works. The capital-versus-ordinary decision is made only after all Section 1231 transactions are combined. The final net result controls the treatment for everything.

To wrap up our example, let’s assume the taxpayer has an ordinary marginal tax rate of 35%, which will make their maximum capital gains rate 20%.

The total Section 1231 gain is $222,000, and it is treated as capital gain. However, not all of it is taxed at the same rate. Out of the $222,000, $150,000 is classified as unrecaptured Section 1250 gain and may be taxed at a maximum rate of 25%. The remaining $72,000 is taxed at the regular capital gains rate of 20%.

What are nonrecaptured Section 1231 losses & Section 1231 recapture?

A nonrecaptured Section 1231 loss is created when a net Section 1231 loss is treated as an ordinary loss. That ordinary loss gives a tax benefit in the year it is claimed.

If a Section 1231 gain occurs within the next five years, the rules look back. Any prior nonrecaptured Section 1231 losses must be recovered first. That means part or all of the new gain is taxed as ordinary income instead of capital gain. This rule is called Section 1231 recapture.

In the earlier example, it was assumed that there were no nonrecaptured Section 1231 losses from the previous five years.

Assume a taxpayer had the following 1231 gains and losses for 2019 through 2024:

In 2020 and 2021, the 1231 losses are deducted as ordinary and generate nonrecaptured section 1231 losses:

In 2022 and 2023, the section 1231 gains of $110,000 must be treated as ordinary income because of the nonrecaptured 1231 losses.

In 2024, $40,000 of the 1231 gain will have to be treated as ordinary 1231 recapture. The remaining $20,000 of gain can be treated as capital because all the nonrecaptured 1231 losses from 2020 and 2021 have been recaptured.

Frequently Asked Questions (FAQs)

Section 1245 property is a type of Section 1231 property. Both involve assets used in a business. The difference is that Section 1245 property refers specifically to depreciable personal property, such as equipment or furniture, rather than real estate.

Examples include machinery, equipment, and furniture used in a business. These are depreciable personal assets, not buildings or land.

Before treating a current-year Section 1231 gain as a capital gain, the prior five years must be reviewed for any Section 1231 losses that were deducted as ordinary losses. If such losses exist, the current gain must be treated as ordinary income to the extent of those prior losses.

Source link