Africa’s hotel development pipeline reaches record highs as East Africa leads construction momentum | News

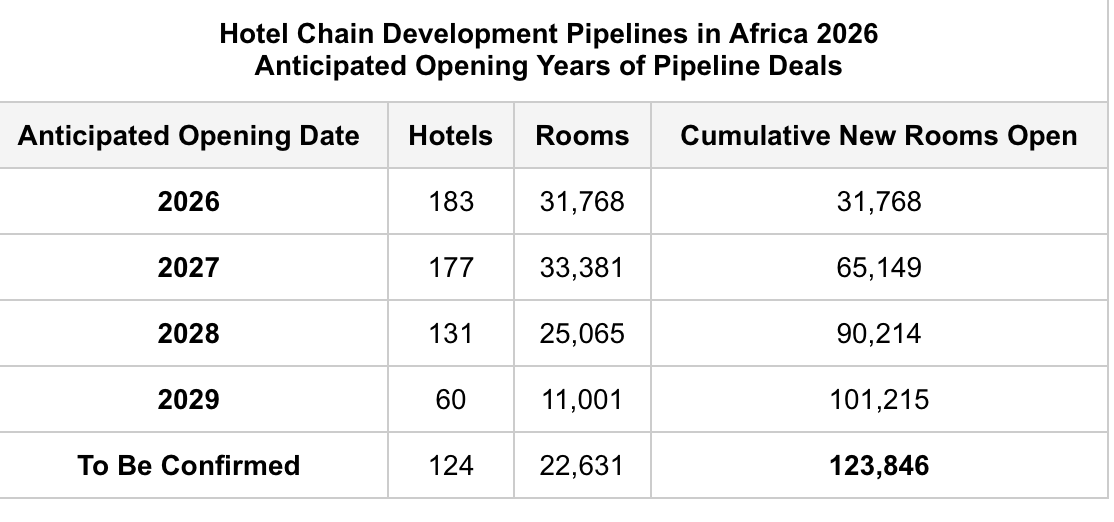

W Hospitality Group’s 2026 Hotel Chain Development Pipelines in Africa report reveals a record 123,846 rooms across 675 hotels and resorts. This represents year-over-year growth of 18.6%, or 12.2% on a same-store basis.

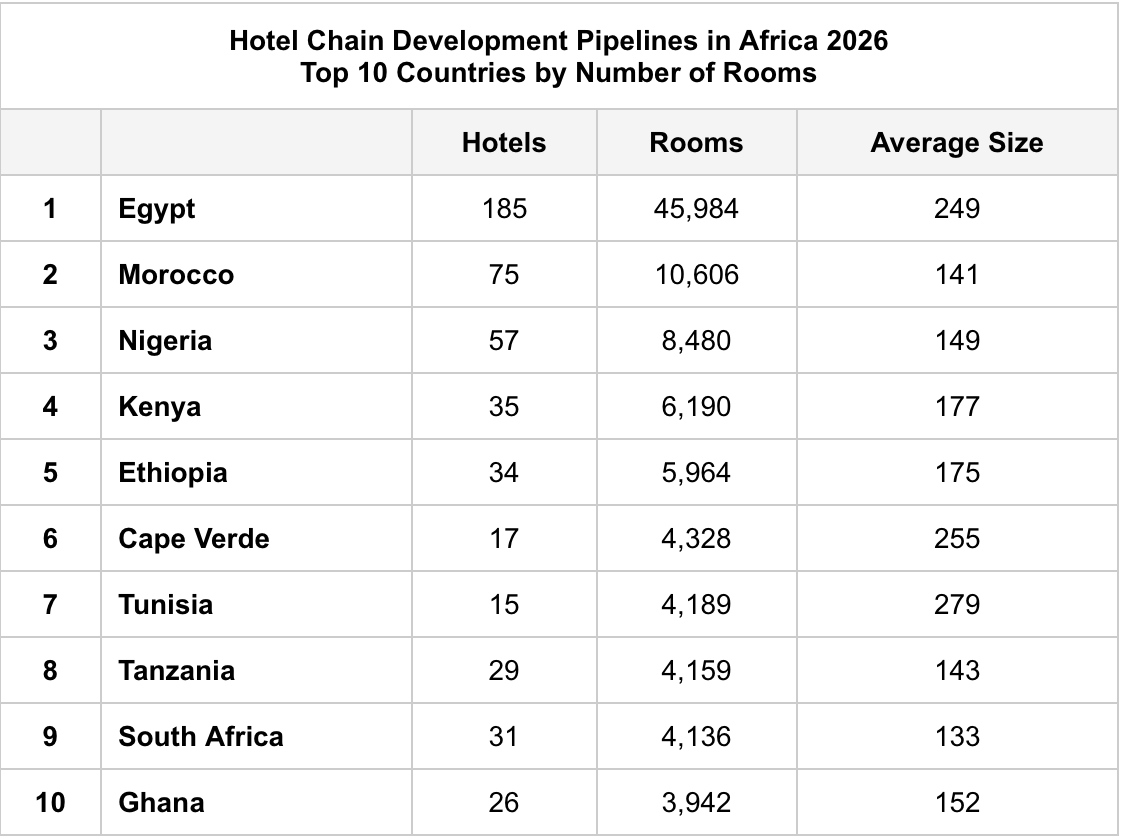

While the overall pipeline reflects strong continental expansion, the data shows that development activity is increasingly concentrated in a small number of dominant markets. The top ten countries now account for 79% of the total pipeline rooms and more than 75% of new business, reinforcing their growing influence on Africa’s hotel development trajectory.

Egypt leads with 45,984 rooms across 185 properties – more than a third of the entire African pipeline and more than four times as many as second-place Morocco, which has 10,606 rooms. Together, Egypt and Morocco account for over 45% of the total pipeline spaces, and their share continues to grow due to the large number of new contracts. Egypt alone recorded 39 new deals last year and expects 33 openings in 2026, boosting sustainable development momentum.

As Trevor Ward, Managing Director of W Hospitality Group, notes: “The data clearly shows that the African hotel development story is driven by a handful of high-performing markets, with Egypt firmly leading the way in both signings and expected openings.”

In addition to the overall scale, the pipeline status data shows that execution momentum is currently strongest in East Africa. Ethiopia and Kenya both have almost 80% of their rooms under construction, closely followed by Tanzania with 77.5%.

This compared to significantly lower percentages of projects under construction in markets such as Nigeria and Cape Verde. While North Africa dominates in terms of overall size, East Africa leads the way in terms of projects actively progressing towards completion and delivery in the near term.

As Trevor Ward notes: “What stands out this year is the strength of East Africa in terms of progressive projects. Kenya, Ethiopia and Tanzania are showing some of the highest construction rates on the continent, suggesting this is where we are likely to see new supply in the short to medium term.”

At operator level, development activity remains highly concentrated among a small number of global brands. Marriott International leads with 31,782 rooms, followed by Hilton and Accor, with the Big Five global chains – including IHG and Radisson Hotel Group – accounting for around 80% of all hotels and rooms across Africa.

While more than 65,000 rooms are expected to open in 2026 and 2027, historical update figures indicate that delivery may fall short of expectations, underscoring the persistent gap between ambition and execution.

A deeper analysis of these trends – including signings, construction progress and expected openings – will be presented at the Future Hospitality Summit Africa, taking place from March 31 to April 1 in Nairobi.