Big changes are in store for the Federal Reserve in 2026: Here’s what it means for interest rates

The new year will bring major changes at the Federal Reserve, with major implications for borrowing costs, the housing market and the economy as a whole.

In addition to major upcoming staff changes, Fed policymakers have indicated that further rate cuts are unlikely until the spring. That creates a new confrontation with the president Donald Trumpwho has made clear his desire for dramatically lower interest rates.

Fed Chairman Jerome PowellTrump’s term ends in May, and Trump is expected to announce his nominee for the position in early January after narrowing the list to a handful of finalists.

Before his term ends, Powell will chair three more meetings of the Federal Open Market Committee (FOMC), the 12-member panel that sets interest rate policy. Starting in January, however, there will be personnel changes, with four new regional Fed presidents rotating on the panel.

Also Fed Governor. Stephen Mirana temporary Trump appointee who has pushed for quick and deep interest rate cuts will see his term expire at the end of January. Trump can reappoint Miran, or use that vacancy to install his nominee for the next Fed chairman.

The fate of the Biden-appointed Fed governor. Lisa Cook is also at stake, with the Supreme Court set to hear arguments in January on Trump’s attempt to fire her.

It is also unclear whether Powell will decide to remain on the FOMC as regular governor after his term as chairman ends, or will resign and vacate his board seat, which he can hold until January 2028.

The shake-up will add a new layer of uncertainty to the Fed after a year of extraordinary central bank politicization. In 2025, Trump and his allies openly attacked Powell and demanded lower interest rates, which would lower the government’s borrowing costs and undermine the economy.

Despite Trump’s threats to fire or indict Powell, the FOMC held its policy rate steady through the first five meetings of 2025, waiting until September to make the first cut.

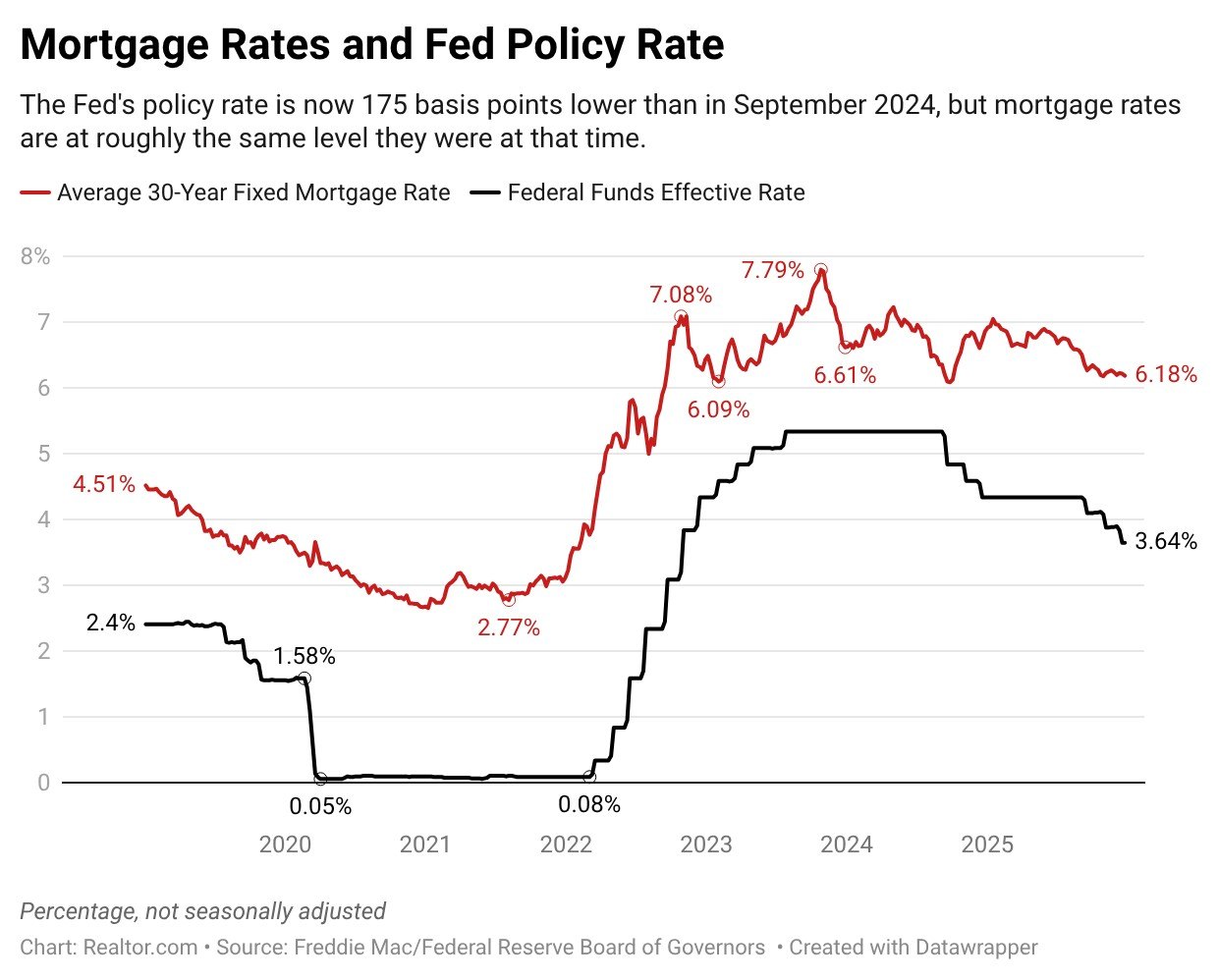

Two consecutive cuts have brought the Fed’s benchmark interest rate to a current range of 3.5% to 3.75%, which is 75 basis points lower than a year ago.

The Fed uses lower interest rates to stimulate the labor market and higher interest rates to fight inflation, in accordance with the central bank’s dual mandate: price stability and maximum employment.

The interest rate set by the FOMC is the short-term rate used for overnight lending between commercial banks, and the Fed has no direct control over long-term mortgage rates. However, the markets that determine mortgage rates move in response to investors’ expectations about inflation and future Fed policy.

How many rate cuts will the Fed make in 2026?

Since the end of December CME Fed Watch shows that financial markets expect the Fed to make only two quarter-point rate cuts in 2026, which would put the policy rate in a range of 3% to 3.25%.

Gamblers in the prediction market Polymarkt are slightly more optimistic and give an approximately equal chance of two and three cuts in 2026.

The members of the FOMC themselves are more conservative, with the latest dot plot’s median projection calling for only a single rate cut. However, the scatter plot also shows a wide range of predictions for 2026, ranging from rate increases to drastic cuts, underscoring the deep divisions within the panel.

Also, newly released minutes from the December meeting show growing hesitation within the panel about further rate cuts, with some participants saying that “it would probably be appropriate to leave the target range unchanged for some time” after last month’s rate cut.

The next FOMC vote on January 29 could provide important insights by showing where the new rotation of regional Fed presidents stand on interest rate policy.

In 2026, the presidents of the Federal Reserve Banks in Cleveland, Philadelphia, Dallas and Minneapolis will receive votes on the FOMC, replacing the presidents of Boston, Chicago, Kansas City and St. Louis.

With the annual rotation, the FOMC will lose two notable ‘hawks’ who voted against a rate cut last month: Chicago Fed President Austan Goolsbee and chairman of the Kansas City Fed Jeffrey Schmid.

However, the panel will have new hawks in their place, including the president of the Cleveland Fed Bet Hammakwho recently said this Wall Street Journal that she would prefer to keep interest rates stable until spring.

Realtor.com® senior economist Jake Krimmel expects the Fed to hold its key rate steady at its January meeting, despite recent consumer price index (CPI) data showing inflation unexpectedly cooled in November.

“Questions about how the government shutdown has affected the recent unexpectedly low CPI make me think the committee will need a lot more evidence that the inflation problem is fading,” he says.

Trump’s announcement of a new Fed chairman is expected soon

Trump said last month he planned to announce his nominee for the next Fed chairman in early January, creating the potential for a “shadow chairman” who could shape market expectations throughout the spring.

Director of the National Economic Council Kevin HassettTrump’s closest economic adviser, is seen as a frontrunner in the prediction markets, with Polymarket estimating a 43% probability of Hassett’s appointment in late December.

Hassett has argued that the Fed should aggressively cut rates, saying the artificial intelligence boom will boost growth and put natural downward pressure on inflation.

“If you look at central banks around the world, the U.S. is way behind the curve in terms of cutting rates,” Hassett said. CNBC on December 23.

That argument is in line with Trump’s view. But because of his close relationship with Trump, if Hassett were appointed he would be faced with the task of convincing markets that he is a credible and independent central banker, and not a political pawn charged with carrying out the president’s will.

By law and tradition, the Fed has long been structured to remain free from political influence and is charged with carrying out its dual mandate of stable prices and maximum employment.

Central bank independence is important because historically, maintaining artificially low interest rates for political reasons often leads to runaway inflation and capital flight. Ultimately, this could increase government borrowing costs as investors lose confidence in the Fed’s commitment to keeping inflation in check.

“If the Fed wants to influence markets in general, and the long end of the yield curve in particular, it needs credibility,” Krimmel says. “Especially for investors in long-term Treasury bonds and mortgage-backed securities, the markets that effectively set mortgage rates, they need to know that the Fed will credibly prevent runaway inflation.”

Krimmel notes that, paradoxically, the more Trump is seen as exerting outsized influence over the Fed, the less ability the central bank will have to deliver the lower long-term interest rates the president is seeking.

“If the Fed is no longer seen as independent of partisan or presidential politics, it will lose its credibility in the markets — and with it the influence the president is so eager to exert,” he says.