The impact of job reductions on the DC -Woningmarkt

Is the Washington, DC home market confronted with a sudden collapse inflamed by Doge’s job treatment? A whirlwind of messages on social media from dubious figures has speculated that a large influx of inventory is hitting the market. Could this be a turning point that sends the DC -Woningcene in a downward spiral? Is there already a crash going on?

Before you draw conclusions, I want to share a word of wisdom: be careful with those doomsday posts that are floating around X. It seems that everyone has something to say, especially if it is sensational!

Let us elaborate on reliable data sources and find out what happens in the DC market. Altos Research Has the new weekly data to give the answers we need.

Weekly inventory data

First, let us examine the national stock data. This has always been an important indicator for housing while we go to normality. Although the stock levels are not yet average, it is encouraging to note that we are considerably above the low stock level of 240,497, included in March 2022. We experienced a slight increase in the inventory last week and we can anticipate the typical Spring stretch quickly.

- Weekly stock change (7 February 14 Feb. 14): Inventaris was released 632,367 Unpleasant 637,991

- The same week last year (February 9 of February 16): The inventory fell from 494,819 Unpleasant 493,987

- The soil of all time was in 2022 240,497

- The stock peak before 2024 was 739,434

- For some context were active lists for the same week in 2015 954,581

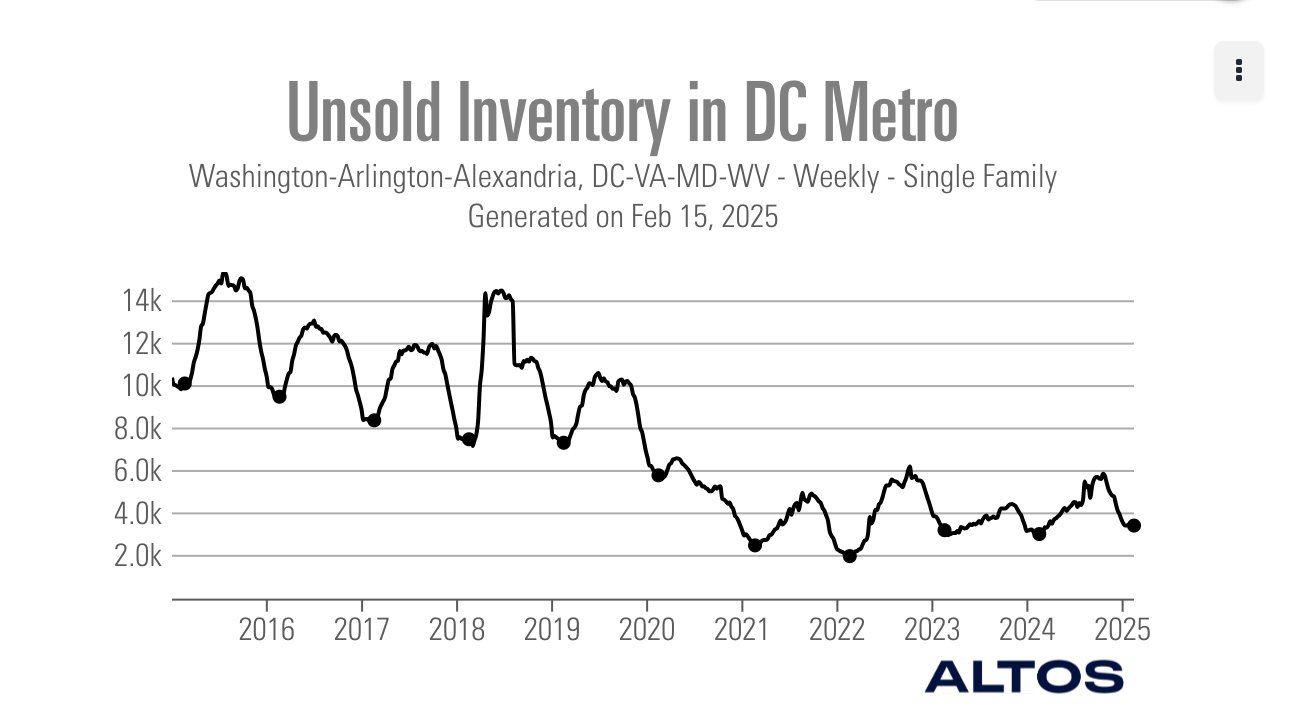

Now let’s look at the DC Metro Housing Market and see if we can see signs of the enormous stock bump that is trending on social media. So far it seems that we don’t see it coming out.

The inventory on the DC Metro Housing Market is not much higher than the Lows Covid-19 inventory. Don’t forget to be careful when listening to people who have never followed the housing economy. When working from such a low basis, inventory that explodes higher will be easy to see, just like what we saw in the data from 2018, so if and when it happens, we will know.

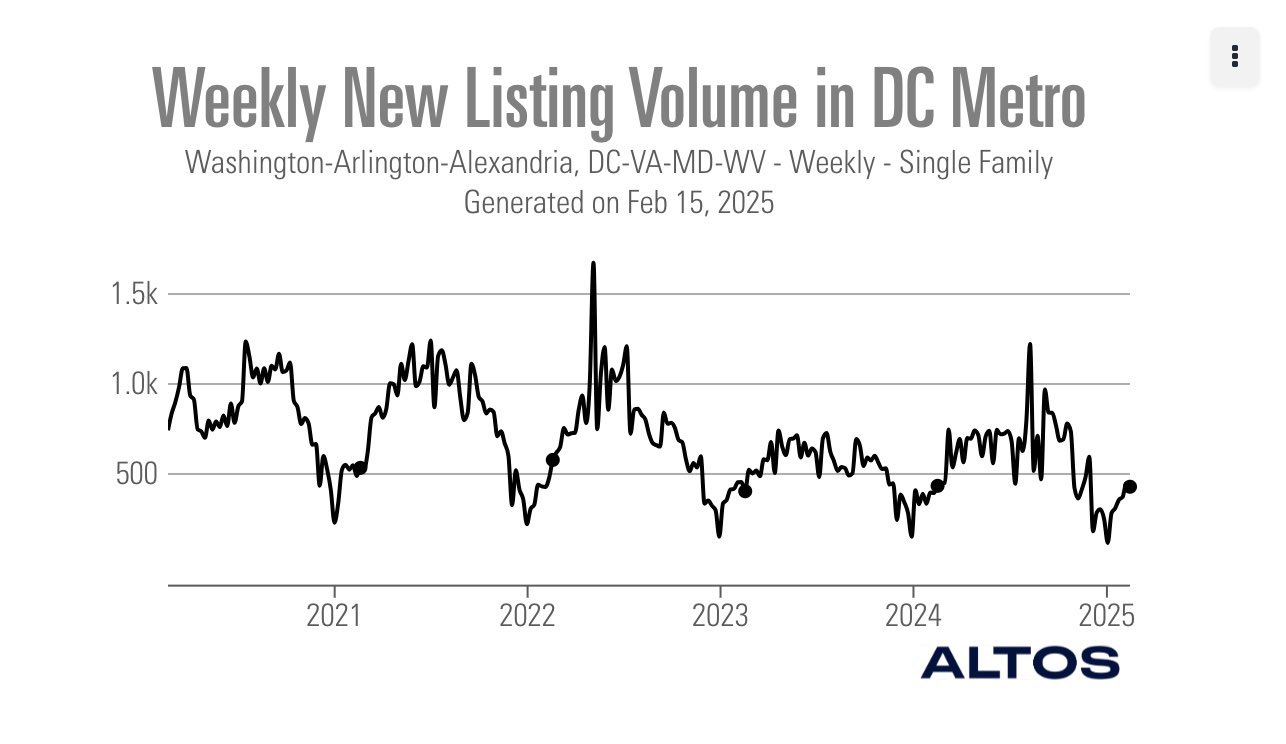

New frame data

The new list data of Altos Research Reflects houses that come on the market without an immediate contract, giving us a real -time picture of every sales pressure in the market. The two lowest new list data in history were the two lowest new list.

Last year I predicted that we would get at least 80,000 a week during the seasonal peak months, but it didn’t happen. This year I think we should hit that goal. Note that this data line ran between 250,000-400,000 a week during the house bubble crash years.

The national new list data for last week in recent years:

- 2025: 56,559

- 2024: 49,556

- 2023: 42.073

Let us investigate the current state of the DC market and recent list data. It seems pretty normal compared to the past years. Unfortunately, it seems that those who promote important stock stirres missed the right data stable to effectively follow these trends.

Jobless claims have risen in this area in recent weeks and we can expect a further increase because of the goal of the Trump administration of Lower federal jobsSome people have estimated at 200,000. I like to like things easy: check unemployed claims, new listing data and active inventory in the coming months and follow the data. However, nothing special has happened yet.

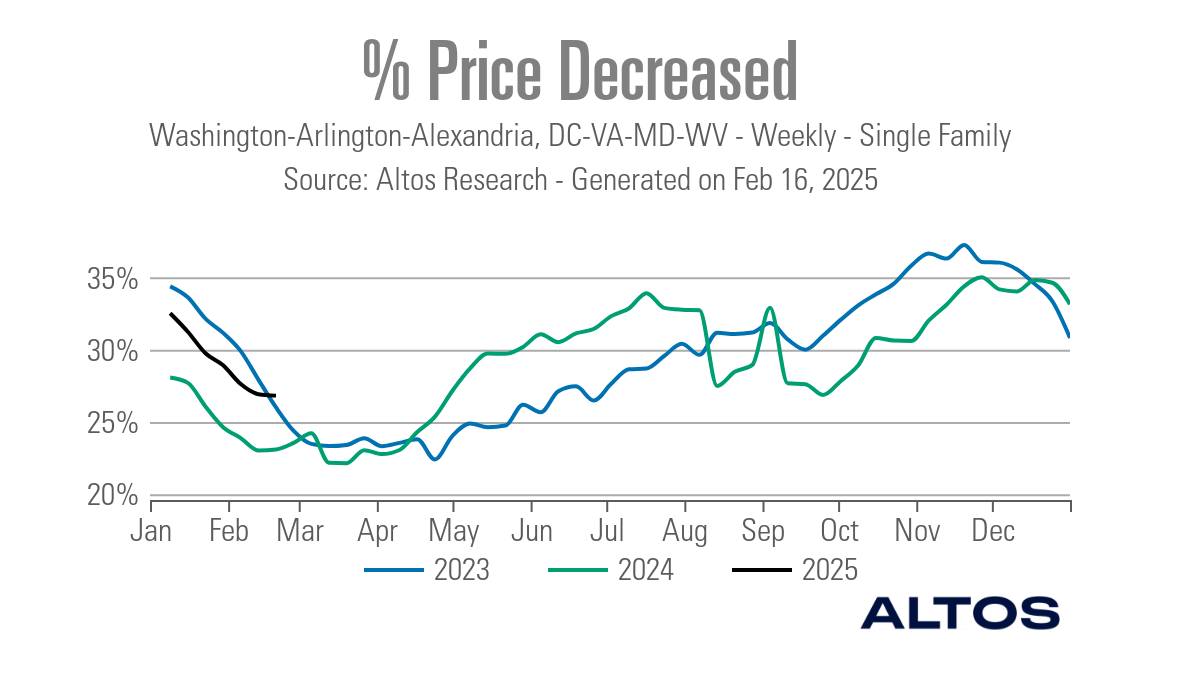

Price percentage

In an average year, about a third of all houses usually experience a price reduction, which reflects the usual dynamics of the housing market. Last year I had a low prediction, with only 2.33% nominal growth in the home prize, which eventually became too low.

Before 2025 I predict the growth of 1.77%, which indicates another year of negative growth in house prices. As the inventory increases and the mortgage interest rate remains above 7%, the price growth is expected to cool. I was mistaken last year, partly because the mortgage interest quickly dropped to 6%. However, the delay in price growth is a positive development for the housing market, which desperately needs this.

Price percentages for last week in recent years:

- 2025: 33%

- 2024: 30%

- 2023: 31%

Finally, let’s investigate the price reduction percentages on the DC market. We can see that the percentage of price reductions is lower than the national average. This does not mean that we will not see stressed sellers, because federal employees lose their jobs in the coming weeks, but the recent data do not indicate any significant stress in the market.

10-year revenue and mortgage interest

In my forecast of 2025 I expect the following series:

- The mortgage interest is between 5.75% and 7.25%.

- The return of 10 years will fluctuate between 3.80% and 4.70%.

The 10-year proceeds was wild last week. The CPI report sent bond returns and the next day the PPI inflation report sent the decrease of the 10-year return. Friday’s weak retail sales report ensured that the 10-year return fell again, so that the mortgage interest rate was pushed under 7%.

Mortgage spreads

The positive story with regard to mortgage interest rate is the improvement of the mortgage spreads that will be observed in 2024 and 2025. Without this improvement, the mortgage interest in 2025 would be almost 8%.

Historically, these spreads usually vary between 1.60% and 1.80%. If we experienced the worst mortgage spreads of 2023, the mortgage interest rate would be 0.77% higher today. Conversely, the current mortgage interest would be around 0.73% to 0.83% lower with regular mortgage spreads.

Application -Buy data

Application application data has been approximately flat this year:

- 2 positive lectures

- 1 flat lecture

- 2 Negative reading

Last week the weekly data fell 2% per week, but by 2% year after year. Historically, the mortgage interest request data is reflected when the mortgage rates are high, negative trends. Last year, when the mortgage interest rate ranged between 6.75% and 7.50%, the data request data showed 14 negative, two positive and two flat measurements.

We will Check the data closely in February and discuss these and other economic topics in the home with our large Housing Economic Top on 26 February in Dallas.

Weekly pending sale

The last weekly current contract details of Altos Research offer valuable insights into the current trends in the demand for homes. This dataset has shown a remarkable improvement since the summer of 2024 and by the end of the year it showed growth on an annual basis.

However, because the mortgage interest rate started to rise late in 2024 and was increased by 2025, it has facilitated a slight decrease in the turnover year after year from where we had grown. We still show higher growth compared to 2023 levels, but not much. Our housing data improves when the mortgage interest rate is almost 6%.

Weekly current contracts for the past week in recent years:

- 2025: 303,957

- 2024: 314,053

- 2023: 298,432

The coming week: Housing data and fed speeches

This week we have various important releases for housing data, including trust in the housing builder, start of housing and existing home sales. On Monday a few Federal reserve presidents will speak, and we must pay attention to how the markets respond to their comments. On Tuesday I will be on CNBC To discuss builders and rates. Moreover, we can expect every Thursday that unemployed claim data will be released, and this information can soon become particularly interesting due to the recent fired.

Hopefully this article offers a better understanding of the home inventory in the DC market.