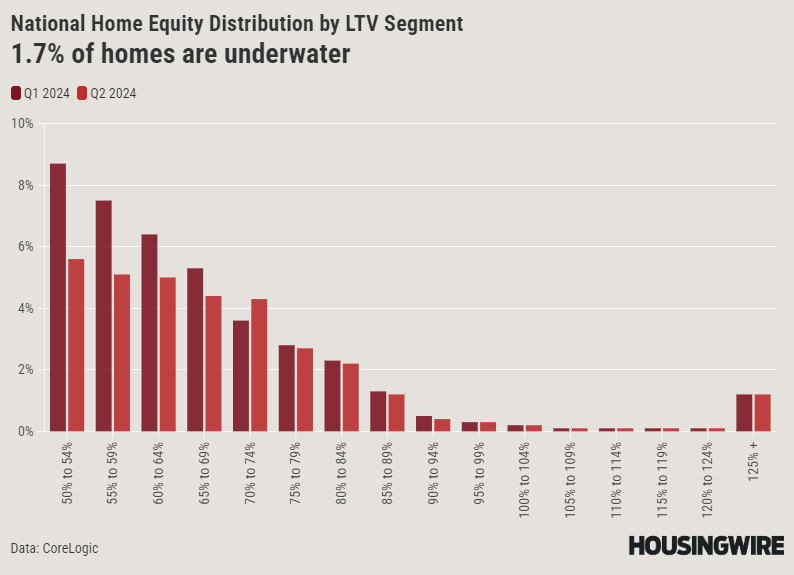

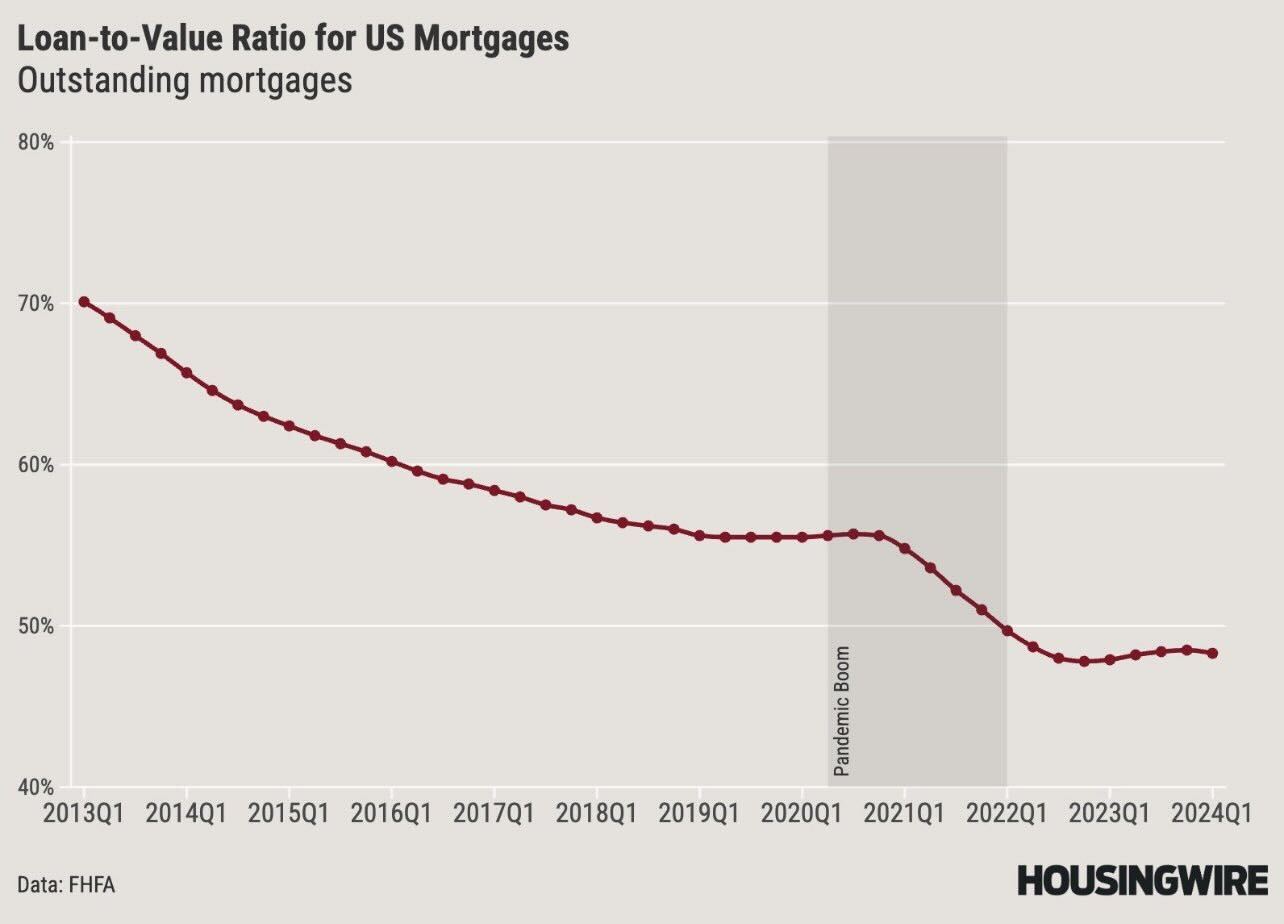

Credit data shows that there is no housing crisis

Credit stress data

When the next recession with job losses occurs we will see a rise in credit stress figures and I am 100% sure that the doomers of America will be on their useless YouTube And X accounts, where they continue their negative story non-stop. However, now that you have all the data, you can see that the credit stress data we saw during the 2008 crisis will never happen again as long as we have a qualified mortgage. Mine crusade The last decade has been about ensuring that lending standards are never relaxed, because today standards are already liberal, but not crazy anymore.

The reason I fought hard for this premise is that when we experience economic stress, as we saw early in the COVID-19 pandemic and with the big burst of inflation, homeowners will be protected with their boring fixed-term mortgages of 30 years.

Using the data below, I expected us to return to pre-COVID-19 levels of credit stress by the end of 2024, but that never happened. Once again, anyone pushing for Housing 2008 needs to get out.

Use these updated credit data charts for your Thanksgiving dinner conversation and remember why this is so important. The new advertising data we track Altos Research has been at its lowest level ever in recent years, while at the time it was running at an accelerated level. Here’s an example using our data from November 9. Look at the difference between this week in 2024 and the same weeks in 2009-2011. We had a lot of stressed salespeople back then!

New ad data this week:

- 2024: 48,863

- 2009: 274,614

- 2010: 359,534

- 2011: 315,915

These credit-challenged sellers didn’t turn around and buy another home, so they created increased distress in the market for years. This hasn’t happened once in the last decade, and it won’t happen until we see a recession with job losses. Moreover, in 2010 more than 23% of houses were flooded; today this is the lowest percentage ever.

Another thing to think about: over 40% of homes don’t even have a mortgage right now, and loan-to-value levels for those that do are averaging below 50%. In 2008, the loan-to-value was almost 85%. Additionally, the average down payment data for this year is 15%, meaning homeowners have more say than they did back then.

Hopefully all these charts will clear up the confusion for your Uncle Dave or other Thanksgiving guests who think we’ll experience another 2008-style housing crash. Homeowner credit data tells a different story.