Why do house prices rise when mortgage rates rise?

Why are house prices still rising even though mortgage rates have risen? A number of people predicted that house prices would fall sharply if mortgage rates rose, but that is not what happened.

This is not a new idea; I have been dealing with people predicting a housing crisis since 2012. Doom porn is trendy in America and is usually done by people who hate the Federal Reserve. But today I’ll use data to explain why, even in 2024 – the third calendar year with the lowest home sales on record (labor-age-adjusted) – national home prices have not collapsed.

Here are the reasons why home prices have supposedly fallen over the past thirteen years:

Ladies and gentlemen, these are not housing experts or analysts. I have a rule: Don’t listen to anyone on the internet unless they show their name, face, a written 2024 price forecast, a five-year home price forecast, and a working model.

Why haven’t house prices fallen this year due to high mortgage rates?

If history is our guide, it is rare that home prices have fallen overall since 1942. If you ignore the period 2007-2011, we only had one negative year; that was 1990, and that was only a 1% decline.

When you ask housing crisis addicts why their house price predictions don’t work, they usually say we need to adjust house prices for inflation, the price of gold, or some other silly historical reference that doesn’t apply to the modern economy. This group is just a cult, and their X accounts have been inaccurate for thirteen years.

Let’s take a look at today’s existing home sales report to see if it can explain why home prices haven’t fallen year over year. To get a real price crash, we would have to see a rise in housing inventory and distressed sellers. As you’ll see below, inventory is growing, but 2024 saw a quiet, healthy increase and no flood of homes coming onto the market.

The National Association of Real Estate Agents‘ existing home sales report shows that home sales fell just 1.0% from August to a seasonally adjusted annual rate of 3.84 million in September. On an annual basis, turnover fell by 3.5%.

“Home sales have essentially been stuck at a pace of about four million units over the past 12 months, but factors typically associated with higher home sales are developing,” said NAR chief economist Lawrence Yun. “There are more inventory choices for consumers, lower mortgage rates than a year ago, and continued addition of jobs to the economy. Perhaps some consumers are hesitant to make big expenditures, such as buying a house before the upcoming elections.”

Where I disagree with Yun is this: we have more inventory because demand has been weaker, and we have more new listings this year than last year. If mortgage rates had stayed below 5.75% – 6.25% this year, we would have seen home sales growth regardless of inventory data. Inventories are growing and home price growth is cooling after the brutally unhealthy housing market of 2021 and early 2022, but it’s not enough to send home prices crashing nationwide.

Below are the graphs from today’s report. Note: Average sales price data is seasonal. Many people will try to fool you by saying that house prices fall in the second half of the year, but these are just normal seasonal price drops.

Based on the NAR data, the normal amount of active inventory since 1982 has been between 2 and 2.5 million. In 2007, the active stock rose to 4 million. Today it is only 1.39 million. With over four months of monthly housing supply and getting closer to my target of 1.52-1.93 million for active inventory, the housing market is in balance. We have some offers to buy houses; we have no demand because the mortgage interest rate is too high.

Okay, but you might wonder: If prices follow volume, why haven’t national home prices fallen sharply? Well, you would have to add distressed sellers into the mix, as we saw from 2007 to 2011, and we simply don’t have that in the data right now.

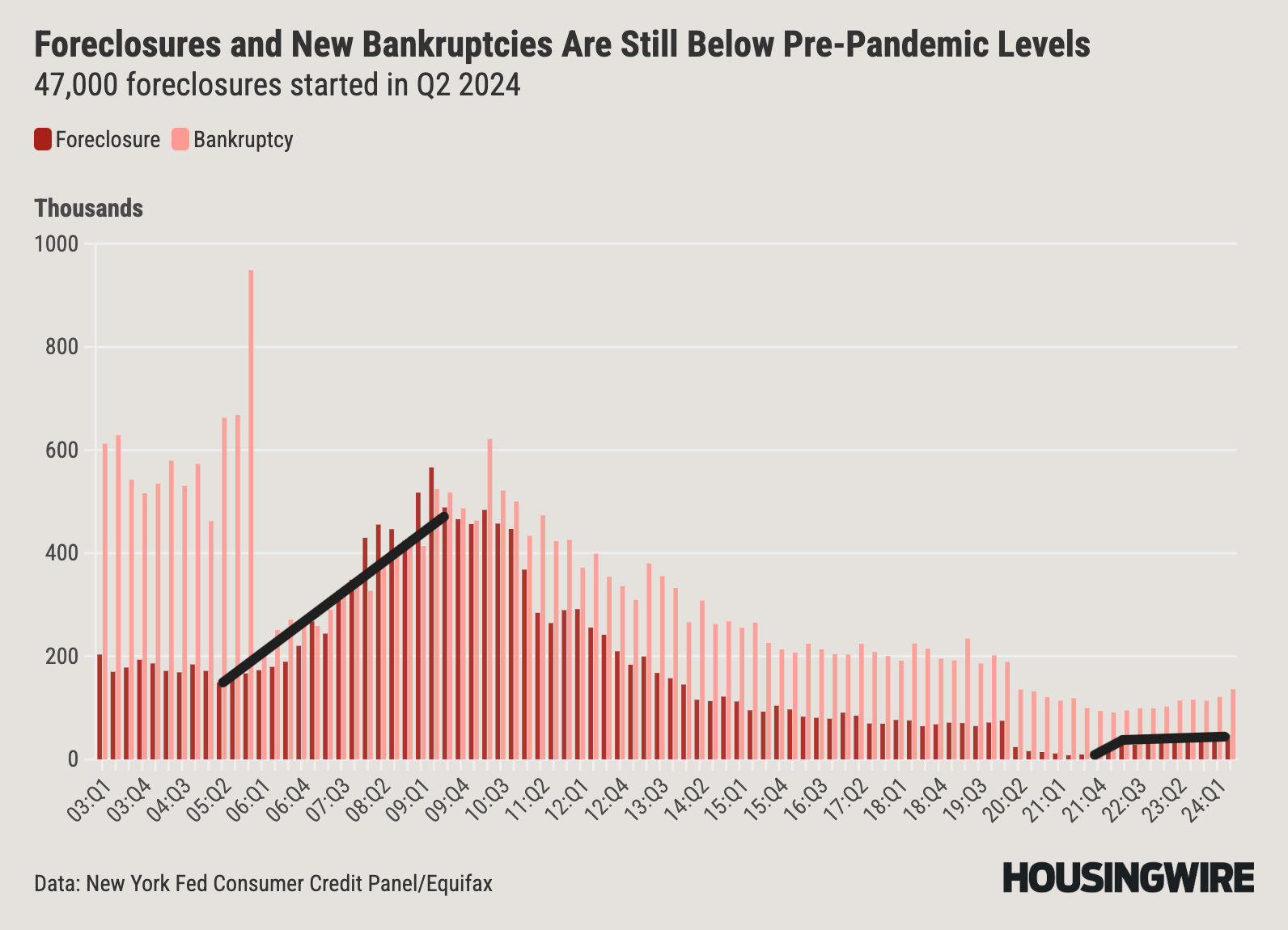

The number of bankruptcies is historically low

As you can see below, foreclosures and foreclosures data rose between 2005 and 2008, all before the recession started with job losses. Today, bankruptcies have not even returned to pre-COVID-19 levels.

There are no major forced sales taking place

Below is our new listing data, which shows that 2023 and 2024 will be the lowest new listing periods ever. This data varies weekly between 30,000 and 90,000 for the last five years. Compare that to 2009 to 2011, when this data line increased 250,000 to 400,000 per week. That’s a big difference, folks. The only time in over 80 years that national house prices have risen had crashed when new listings data was three times higher than we’ve seen in recent years.

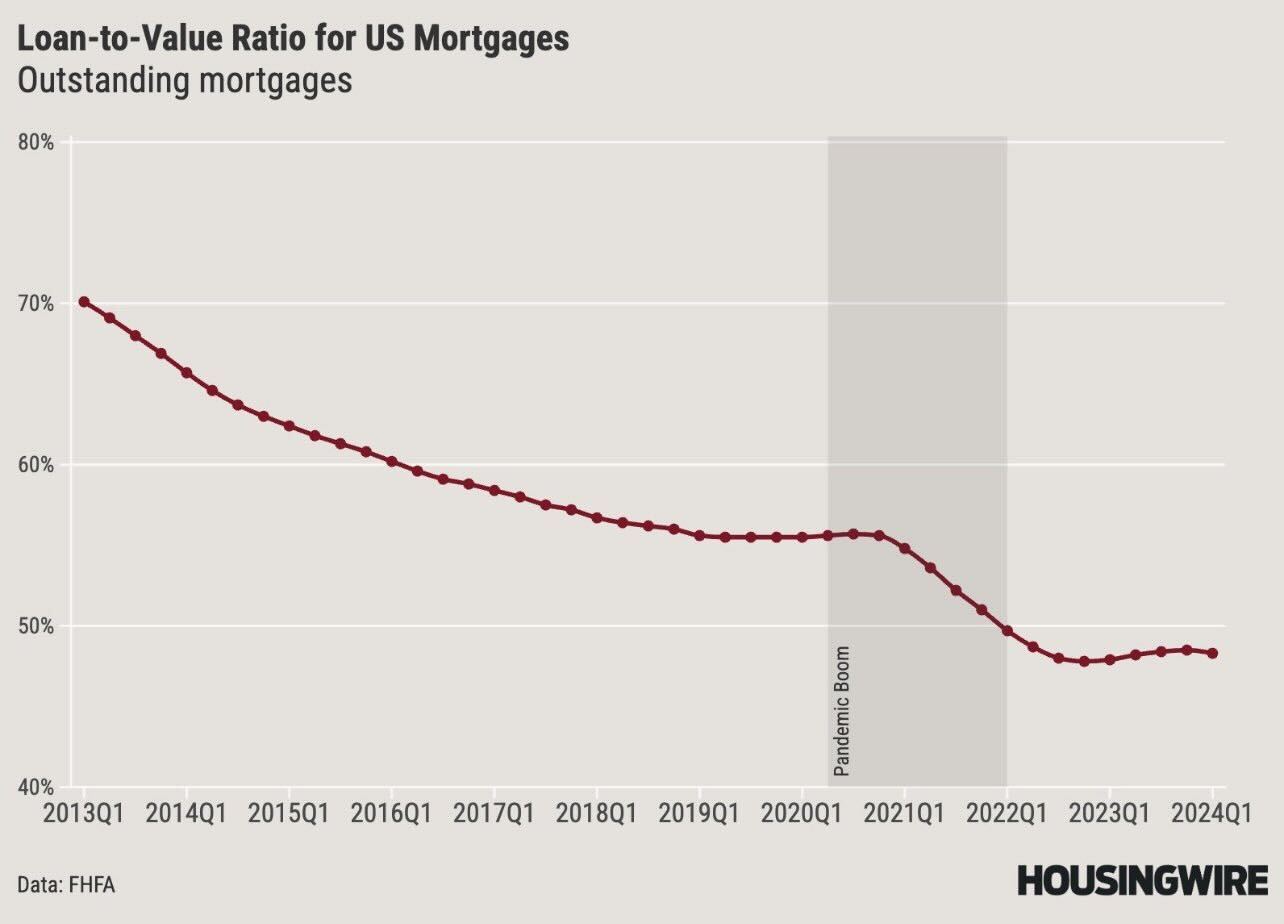

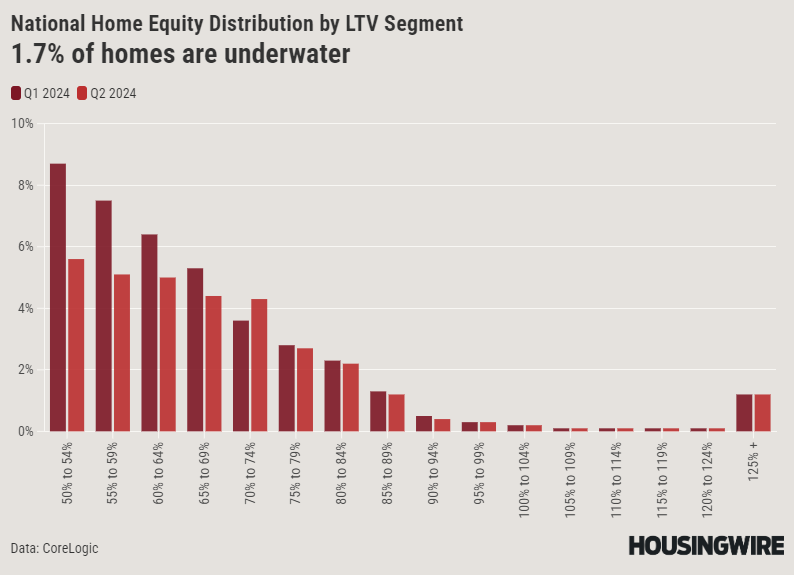

Lots of equity this time

These days, few people sell their homes underwater; the percentage of underwater homes is 1.7%. Moreover, the Loan-to-Value of homes with a mortgage is below 50%, and more than 40% of homes in America do not even have a mortgage. In 2010, as new listing data exploded, more than 23% of homes in America were underwater.

I want to keep it very simple: we had a period where national home prices collapsed, and to replicate that model you need a number of comparable variables, mainly distressed sellers or people forced to sell in a declining market. Some people believed that rising mortgage rates over the past two years would automatically mean that house prices would collapse. History does not agree with this claim. The data has been showing us for decades that we have periods in history where we have had both rising mortgage rates and inventories without home prices collapsing.

As we can see in today’s existing home sales report, home sales are down don’t crash. I discussed this on the HousingWire Daily Podcast last year, in which I explained my housing economic model. For a national housing price crash to happen you need a terrible economy, big distressed sellers, and no government assistance in helping American citizens, which means you need a repeat of the Great Recession of 2008. The data above shows that this is not the case today.