US Home Equity has reached $ 35 trillion. It’s a blessing and a curse

This comes from one Recent report Through the Wall Street Journal. Under the less expected consequences, high amounts of equity can limit the amount of financial aid for which some potential students are eligible. Spikes in housing values can increase the ability of a homeowner, but remarkable increases from the real estate tax have also ensured that some have reduced their discretionary expenses.

“And cashing in the wealth is difficult: high interest rates and prices have stopped the sale of home and the prospect of tax accounts of a large capital gain is to hold the houses,” the report said.

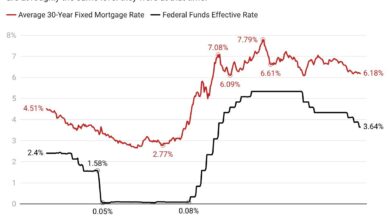

Recent market volatility that results from the White houseThe rate policy can cause some homeowners to find more new financial options, including ticking equity. But tight credit standards and the persistent ghost of interest rates can destroy these goals before they can be fully achieved, the magazine reported.

And house prices, which reached historical highlights in the run-up to and immediate aftermath of the COVID-19 Pandemie, have been trending in the other direction.

“House prices have cooled, especially in some parts of the country where they have risen the most in recent years,” the report explained. “Although that can ultimately reduce real estate tax, it makes Americans prospect with the prospect of seeing the wealth in their homes eroding without ever tapping it.”

While those who feel excluded from the housing market, see home ownership as a goal to strive for, current homeowners feel more financially pressed because of these realities, said Rick Sharga, founder and CEO of Real Estate consultancy CJ Patrick Co.

“Many homeowners still feel surprisingly financially insecure,” he said.

In general, homeowners also seem reluctant to tap their own capacity despite his meteoric growth in the past five years. Older homeowners can be better suited to tap their equity because they have paid their mortgages longer, and a larger part of this cohort will have their houses sooner.

But the senior equity has also taken a hit in recent months. It placed a modest decline in the third quarter of 2024 before it went through a more serious decrease in the fourth quarter, according to data from the National Reverse MortGage Lenders Association (NRMLA) and Risk -span.

Older Americans can also have more diverse needs that can be tackled by tapping their equity, said NRMLA president Steve Irwin.

“A new study from the Center for Retirement Research at Boston College estimates that 30% of Americans would consider using their equity to pay for future needs for long -term care,” Irwin said. “This is encouraging news. The costs for getting care in the house can be considerable, even for those who are planned as well as possible.”

But the impact of real estate tax and other pressure is realistic, and they can let people tap on the sidelines of equity for some time.